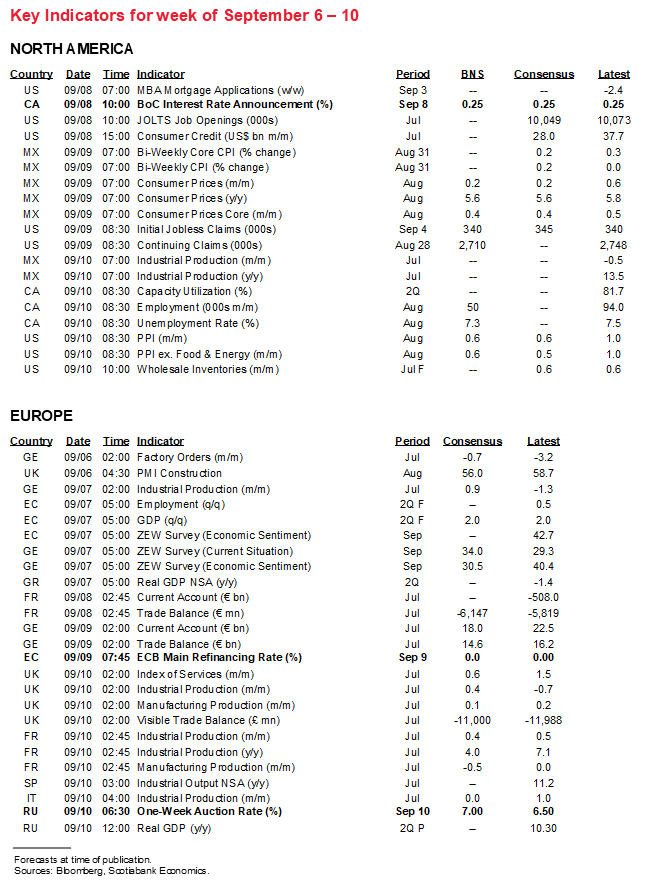

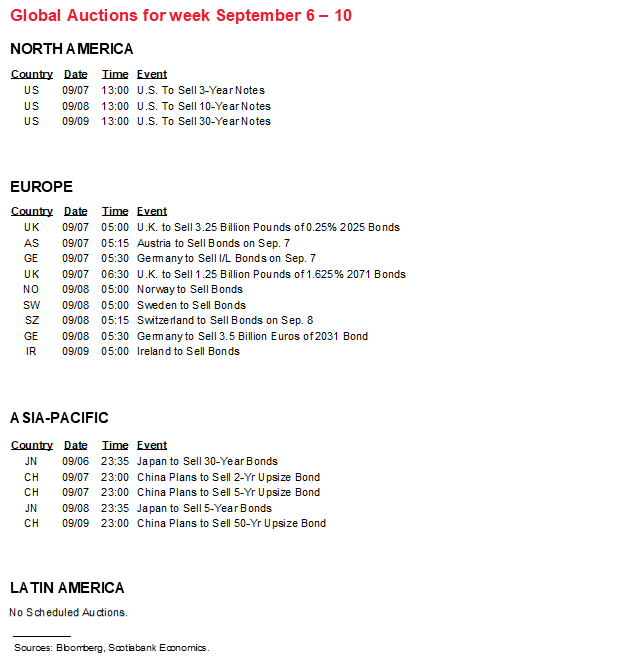

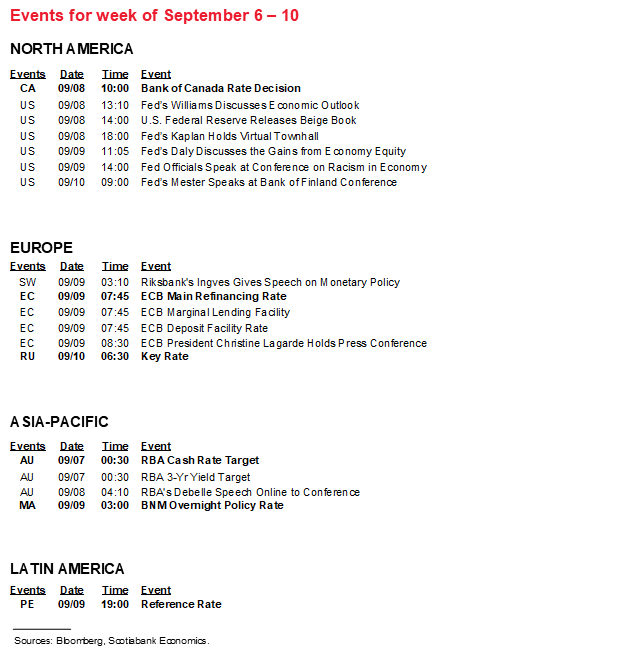

Next Week's Risk Dashboard

• ECB: Time to walk the talk on purchases?

• Why the BoC could still be interesting

• The last pre-election Canadian jobs report

• Canadian election: shifting scenarios and leaders’ debates

• RBA: Sufficient reason not to taper?

• Russia likely to hike again

• Peru’s central bank expected to hike

• Bank Negara to hold

• CPI: China, Norway, Mexico, Chile, Colombia, Brazil, Russia, Philippines, Thailand

• Other releases: China, Germany, UK

Chart of the Week

Times have changed it seems and funny enough there is no better gauge of this from a Canadian standpoint than to remember what The Economist magazine has said about the country not so long ago. In 2015 they generated headlines by calling the beautiful city of Vancouver, Canada ‘mind-numbingly boring.’ In 2016, the magazine shifted gears and got caught up in the politicized effects of Trump’s victory stateside and ‘Trudeaumania’ with a front cover titled “Liberty Moves North: Canada’s Example to the World.” In 2021, the magazine is relatively quiet on Canada when the country might be spicing it up a touch.

Thrill seekers, be careful what you ask for. The coming week could further inform market participants’ expectations for the upcoming Canadian election, how the central bank might guide markets on the future of its balance sheet and whether job growth is holding up in the face of the more muted rise of the Delta variant than in the US. In fact, other than the ECB and several regional central banks, most of the global calendar-based action is going to be focused on Canada this week.

CANADIAN ELECTION WATCH

Canada’s election campaign is heading into a critical stretch ahead of the vote on September 20th. Nationally televised leaders’ debates will be held this week starting with the French-language debate on September 8th from 8pm–10pm—and hence right after the Bank of Canada’s statement—and followed by the English-language debate the next night from 9pm–11pm—after Governor Macklem speaks earlier in the day. Topics will be announced three days in advance, but you can probably guess at what they’ll be and the scope for differentiation on macroeconomic policies as they may materially affect government debt issuance, growth and inflation is probably pretty low. If the recent debate before a Quebec-based tv audience was any sign, then don’t look for major policy guidance.

At present, the two main competing attempts at translating polling data into seat projections are mildly conflicting (here and here). One shows the Liberals winning a minority and the other shows the Conservatives winning a minority. Neither party comes close to the 170 seats required for a majority, but that could still change.

This means one of two most likely outcomes at this point, barring a still possible majority outcome for either party. One is the status quo of a center-left Liberal minority propped up by the NDP. Alternatively, if the centrist Conservatives garner the most seats then they could be asked to form a government which could turn the focus to seeking a coalition partner or being vulnerable to confidence votes in Parliament such as at the first attempt to land a budget.

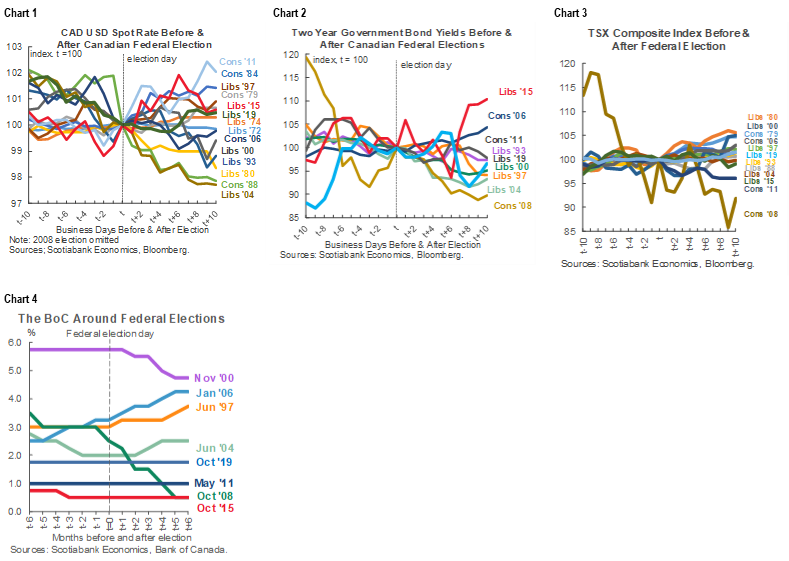

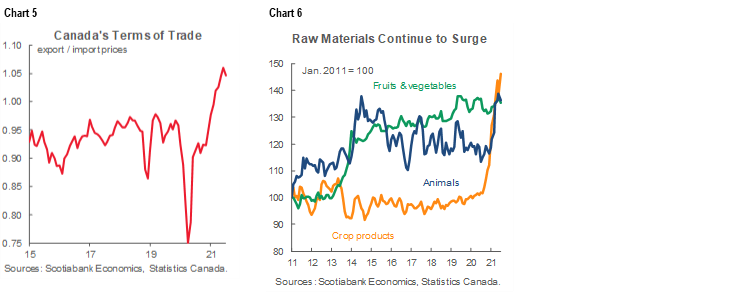

We’re therefore in a state of flux evaluating implications for markets and playing market volatility potentially over a more extended period of time. The impact of past elections on financial markets is shown in charts 1–3 and chart 4 shows how the BoC’s policy has tended to behave around elections.

CENTRAL BANKS—ECB & BOC

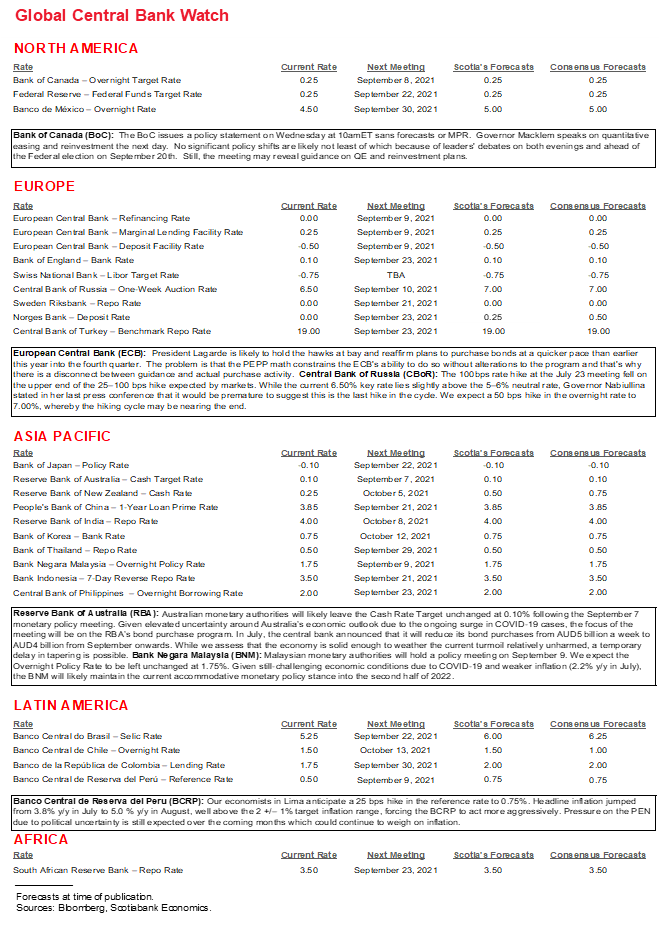

Six central banks are slated to make decisions over the coming week while markets will remain on guard toward the prospect of a required reserve ratio cut by the People’s Bank of China at some point.

BANK OF CANADA—HOW TO INFORM MARKETS, BUT NOT THE POLITICIANS

The Bank of Canada issues an updated policy statement on Wednesday at 10amET sans forecasts or MPR. Governor Macklem will speak on the economy in a session titled “QE and the reinvestment phase” the next day during an online event held by Quebec’s Chamber of Commerce (12pmET). There will be (usually tame) audience Q&A, but no press conference. The BoC might pull off a way of informing markets on topics that would make political eyes glaze over.

The BoC—like many other central banks—tends to lie rather low before elections and the BoC has a track record of working very closely with the Federal government on approaches to policy. I wouldn’t look for any big policy shifts in either direction. They don’t have to issue another round of forecasts until October 27th and so pre-committing to any altered views would probably be premature at this stage. They also tend to prefer tapering at MPR meetings to have full cover with a complete narrative. Also, the first nationally televised leaders’ debate will commence just 10 hours after Wednesday’s statement and the second debate starts 9 hours after Macklem begins speaking the next day and so he probably doesn’t want monetary policy to be a last-minute lightning rod. Then again, none of the leaders appear to be the least bit fussed by inflation risk anyway and they’re all pledging to spend a lot of other peoples’ money going forward!

So how do you say something that achieves the goal of lying low while nevertheless saying something useful to BoC watchers and thus making the event worthwhile? Bwah, good luck! Or maybe, just maybe you do so by talking about quantitative easing and watch economists, bond traders and PMs perk up while the political wonks fall asleep. The title of Macklem’s address suggests that we will learn more about the next leg of the Bank of Canada’s bond purchase program now that they have steadily tapered purchases in a three step tango from “at least” $5B/week at the beginning to $2B/week at present.

Here are the possible topics Macklem may broach in this regard beyond the statement that may continue to err on the side of cautious optimism while nevertheless noting the disappointment in GDP revisions and rising COVID-19 case counts.

a. Plans for further tapering

It would be a bold—and hence a low, but non-zero probability—stance ahead of the election if he were to announce the end of purchases especially on the back of a big miss for the Bank of Canada’s (and everyone else’s) GDP forecasts and uncertainty surrounding the fourth wave of COVID-19 cases. It would be a little less bold if he guided that the end was nearing over something like ‘coming meetings.’

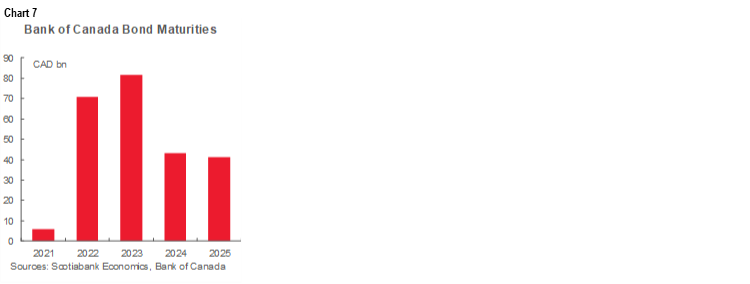

A sharply improving terms of trade (the ratio of export to import prices) offers one reason for doing so given the implications for national income (chart 5), but the bigger case for doing so would be inflation. Nevertheless, when given the opportunity to adjust his narrative on this issue Governor Macklem has only tended to dig in deeper. I don’t personally see how he can still argue that all inflation is just base-effect driven and it’s likely to be persistent in my view, but policy guidance needs Macklem’s view to pivot on this matter. That’s not impossible. He could follow in the footsteps of Fed Chair Powell who started off the same way earlier in the year but pivoted in his Jackson Hole speech toward the FOMC consensus by declaring that the price stability half of the Fed’s dual mandate has now been achieved. Going into the Fall, it’s likely that supply chain pressures will continue to put the heat on inflation readings. Two examples might be in sectors like autos and the likelihood that your grocery bill will probably keep rising as prices get passed on (chart 6).

Macklem’s stance has also attracted criticism. Former Governor Dodge said back on July 27th that “By insisting it’s all temporary they tend to undermine their own credibility, which is unfortunate. It’s better to be humble and say that’s what we think, but of course there is a chance things could be different.” Dodge went on to guide that he thought the BoC would begin to de-emphasize temporary drivers and offer “greater recognition there may be more longer-term pressures in the system.” If so, that might afford an opportunity to further adjust purchases soon or to further coax markets in that direction.

b. Reinvestment horizon

Even if no such guidance arrives just yet, just by virtue of the reductions to date it’s logical to assume that the end of the net purchases is drawing nearer which makes it important to hold hands in advance of the ensuing steps. There are important issues around the mechanics of the reinvestment phase that the BoC may further inform even if implementing them somewhat further down the road. Way back in March (here) we last heard from the BoC that “we would arrive at the reinvestment phase of QE some amount of time before we start to increase the policy interest rate.” Tapering steps were guided to proceed on a “gradual and measured” basis and the BoC said—much like the Fed is now—that altering QE steps “won’t necessarily mean that we have changed our views about when we will need to start raising the policy rate.”

But we don’t know how long the BoC might reinvest. They might not know either. I would expect Macklem to guide that this reinvestment phase will be conditioned around the durable achievement of the Bank of Canada’s 2% inflation goal and inclusive recovery language without committing to a time period.

c. Reinvestment style

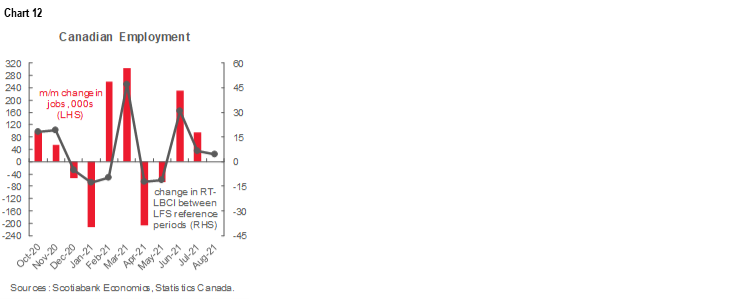

We have not heard public guidance on how the BoC may reinvest these maturing flows and that could also be further informed. About C$71 billion in Canada bonds presently sitting on the BoC’s balance sheet will mature next year (chart 7). They will do so in lumpy and erratic fashion as the weeks and months go by. They could reinvest on a matching flows basis as the maturities arise. They could instead reinvest on a regular averaging basis such as, say, just under C$1.5B/week to match maturing bonds. If they do the latter, however, then whatever flow they pick might imply expected horizons for reinvestment plans. They could say they will reinvest tactically with the end smoothed goal being a flat balance sheet for some time but without disclosing a steady or predictable amount. They could adopt a hybrid tactical approach that is some combination of these approaches while implicitly taking debt issuance plans into account including maturity compositions.

d. Reinvestment composition

Will the BoC reinvest in neutral fashion across the curve, favour some maturity benchmarks over others or match the maturity of the issues at hand as they arrive? They haven’t said, but they have so far resisted an announcement effect around intentions to alter the weighted average maturity of their present net purchase flows.

All of which brings us closer to the point at which the Bank of Canada is expected to announce the conclusions of its strategic review. That is likely at a separate event later. It’s not looking to me as if the staffers are convinced there is a material net benefit to straying from the current flexible inflation-targeting approach (here).

EUROPEAN CENTRAL BANK—TIME TO WALK THE TALK

The ECB weighs in on Thursday with a policy statement at 7:45amET followed by President Lagarde’s press conference forty-five minutes later. It’s unlikely that the balance of the Governing Council will adopt the stance of some of the pre-meeting language from some of its more hawkish members. The hawks have pointed to inflation, but if there is one market where base effects have indeed played a large role it is the Eurozone given influences such as Germany’s sales tax cut last year that could keep year-over-year rates relatively high over the duration of this year.

Still, at hand is whether the ECB will continue to just jawbone purchase intentions or more concretely enact those intentions in the wake of announcing the results of its strategic review. The statement is likely to strike out “current quarter” with a reference to the next quarter in guiding that GC “continues to expect purchases under the pandemic emergency purchase programme (PEPP) over the current quarter to be conducted at a significantly higher pace than during the first months of the year.”

Contrast this guidance to the actual purchase flows of late as shown in chart 8. With the exception of a downward blip at the very start of the year, net purchase flows have generally ebbed of late.

But how much room does the ECB have in practice in order to deliver on the promise of higher purchases? Not much. Maybe none at all. The Pandemic Emergency Purchase Programme has an envelope of €1.85 trillion and has utilized €1.325 trillion of this room as at the end of August. The program is to continue “until at least the end of March 2022.” If we take the end of March as the cut-off then that’s about 30 weeks from now. By corollary, ending purchases at that point would imply only being able to buy an average weekly amount of €17½ billion before the envelope is exhausted. If the program is allowed to run longer without an increase then the purchase flows must be smaller. Either way, it’s unlikely that purchases will be higher than earlier in the year over Q4 when they haven’t been of late and without exhausting the size of the PEPP program before March. Lagarde either has to gradually twist some arms on the size of the PEPP or eventually listen to the hawks, or simply keep purchases running around the pace similar to that which we’ve seen over recent weeks and face questioning about why the verbiage says otherwise.

Four other central banks will issue policy decisions over the coming week and could also spice things up themselves.

RESERVE BANK OF AUSTRALIA—LOWE’S TAPER ‘OUT’ DOESN’T SEEM COMPELLING

The Reserve Bank of Australia will deliver an updated statement and policy decisions on Tuesday. The key issue at hand is whether they delay plans to implement a reduction of bond purchases from A$5 billion per week to $4B this month. Opinions are varied, but on August 3rd (here) and more pointedly a couple of days later (here) Governor Lowe dug in and indicated ongoing commitment to reducing purchases. It’s best to just repeat what he said here and set a high bar against expectations he will deviate from this logic next week:

“At the Board's meeting earlier this week we considered the case for delaying this tapering to $4 billion a week. The critical issue here is the outlook for the economy. As I discussed earlier, we are expecting a return to strong growth next year. Any additional bond purchases would have their maximum effect at that time and only a very small effect right now when the extra support is needed most. The Board also recognised that fiscal policy is the more appropriate instrument for providing support in response to a temporary and localised hit to income, and the Board welcomes the substantial fiscal response by governments in Australia. We will, however, keep the situation under review and are prepared to act in response to further bad news on the health front that affects the outlook for the economy over the year ahead.”

His comments left an out depending upon how health risks evolved, but only insofar as they impact the economy ‘over the year ahead’ and not in the context of recently increasing COVID-19 cases.

OTHER CENTRAL BANKS

Peru: Another 0.25% rate hike to the reference rate of 0.5% is expected on Thursday. Rising inflation in part driven by the impact of political uncertainty on the Sol is a driving motivation (chart 9).

Russia: The central bank is expected to raise the key rate by another 25–50bps on Friday to 6.25–6.5%. Governor Nabiullina indicated in her press conference on July 23rd following a 100bps hike that because of uncertainties it would be “premature” to assume that rate hikes are over, though they are nearing completion.

Bank Negara Malaysia: Consensus unanimously expects a hold not least because of the country’s experience with soaring COVID-19 cases.

CANADIAN JOBS—LESS DELTA TO THE DELTA?

Canada updates jobs for the month of August on Friday. I went with +50k and a small decline in the unemployment rate to 7.3% on the assumption that fewer people entered the labour force than got jobs. Canada might not suffer the same downside risk to the pace of job growth owing in part to the Delta variant as the US did through nonfarm payrolls. The underlying rationale includes the following points.

Canada’s COVID-19 fourth wave is much less acute than seen in the US at least so far and including the period between Labour Force Survey reference weeks in July and August. Chart 10 shows the striking difference in per capita case rates. That might suggest somewhat less scope for disappointment than occurred with nonfarm payrolls for August.

Secondly, high-frequency tracking of job postings continued to increase through to the end of August as shown here and in chart 11.

Third, kudos to Statistics Canada’s forays into tracking high frequency activity in their Real-Time Local Business Conditions Index (here). It’s available for seven Canadian cities right through the Labour Force Survey’s reference week for August which is always the calendar week including the 15th day of each month. Chart 12 is an attempt at weighting the cities into a national composite and showing the connection to monthly job growth. It’s fallible, but as far as job indicators go it looks to be a pretty useful gauge on average during the pandemic. The measure suggests that job growth will moderate compared to prior months but stay positive.

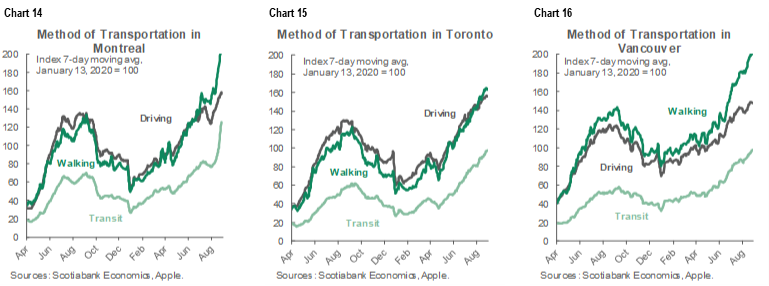

Furthermore, chart 13 shows that COVID-19 restrictions continued to ease between July and August while charts 14–16 show that mobility powered forward across the country’s largest cities.

Also see Marc Ercolao’s front cover nifty ‘radar’ chart that shows a sector breakdown of peak job losses and where they stand at present. It helps to graphically demonstrate areas of ongoing softness.

OTHER MACRO

The rest of the global macro line-up will be fairly light over the coming week. The main points of emphasis will be upon the economies of China, Germany and the UK. Also recall that the US and Canada will be on holiday on Monday for Labour Day.

China updates trade figures for August early in the week and possibly aggregate financing figures for August either this week or next.

Several countries will provide inflation updates including Chinese CPI and producer prices on Wednesday, US producer prices on Friday, Russia on Wednesday ahead of the central bank decision two days later, several Latin America countries including Colombia this weekend, Chile on Wednesday and then Mexico and Brazil on Thursday. Norway updates on Friday. The Philippines and Thailand update early in the week as well.

US releases will be very light with just the Fed’s Beige Book of regional economic conditions on Wednesday, weekly jobless claims on Thursday and limited Fed-speak.

UK releases will be skewed to Friday when July readings for services, trade and industrial output arrive.

Germany updates factory orders during July (Monday), ZEW investor confidence (Tuesday) and exports on Thursday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.