Next Week's Risk Dashboard

• CBs: PBOC, Banxico, BanRep…

• …RBNZ, BoT, Norges, Riksbank, SNB, Turkey

• CB guidance: Fed, Brazil

• PMIs: EZ, UK, US

• Canada’s Throne Speech

• US macro

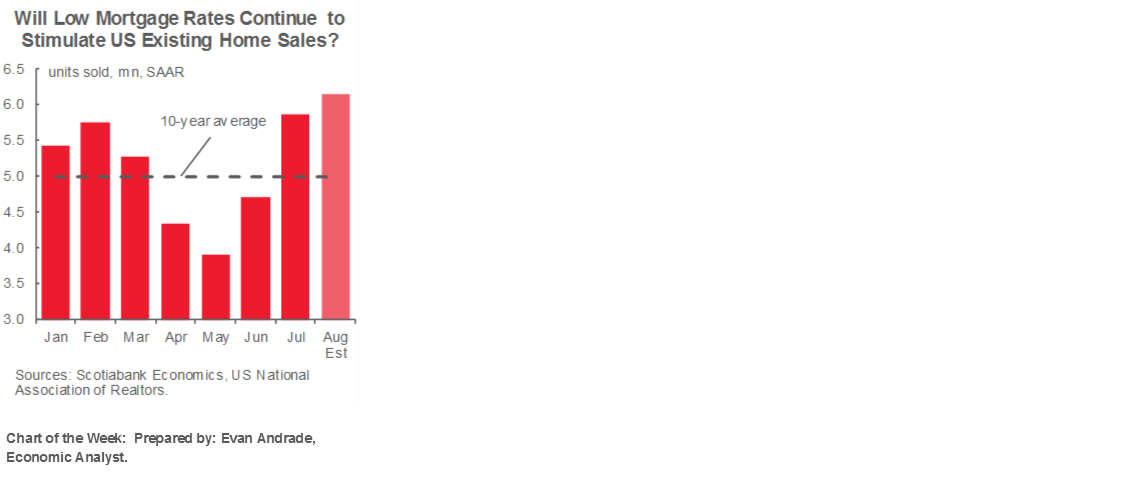

Chart of the Week

To some, September is a wonderful time of year that leads to crisper air and Fall colours in the northern hemisphere while transitioning to Spring and then Summer in the southern hemisphere. To investors, it often results in narrative shifts and amplified market risks. So far, this September is true to form as witnessed by the S&P500 that peaked in early September and has struggled so far this month.

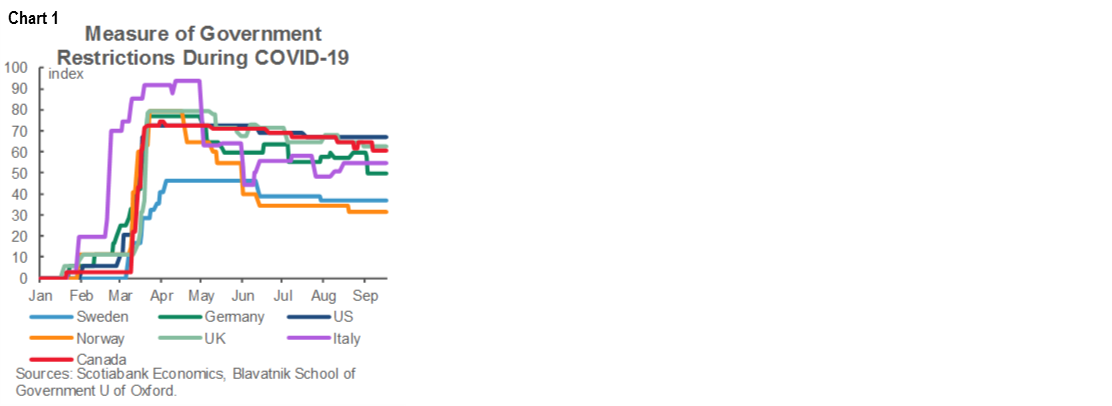

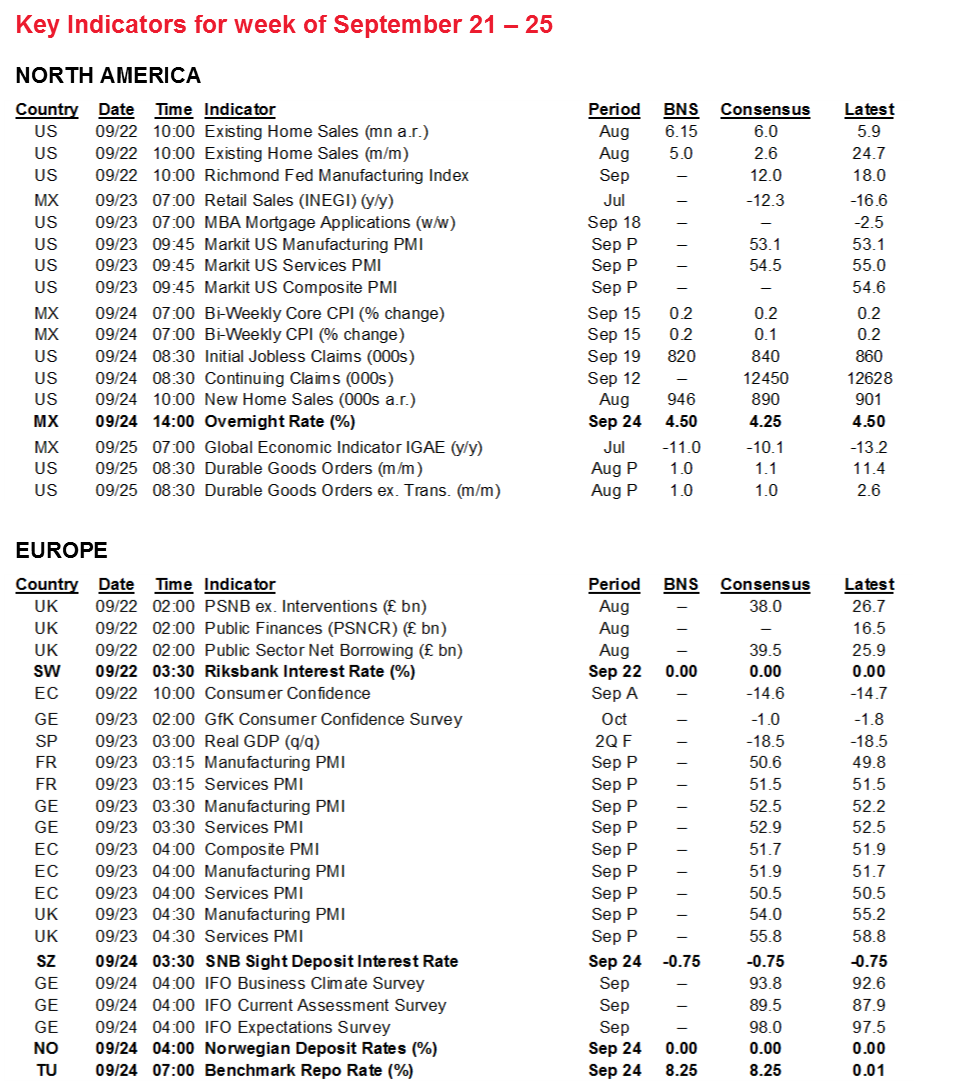

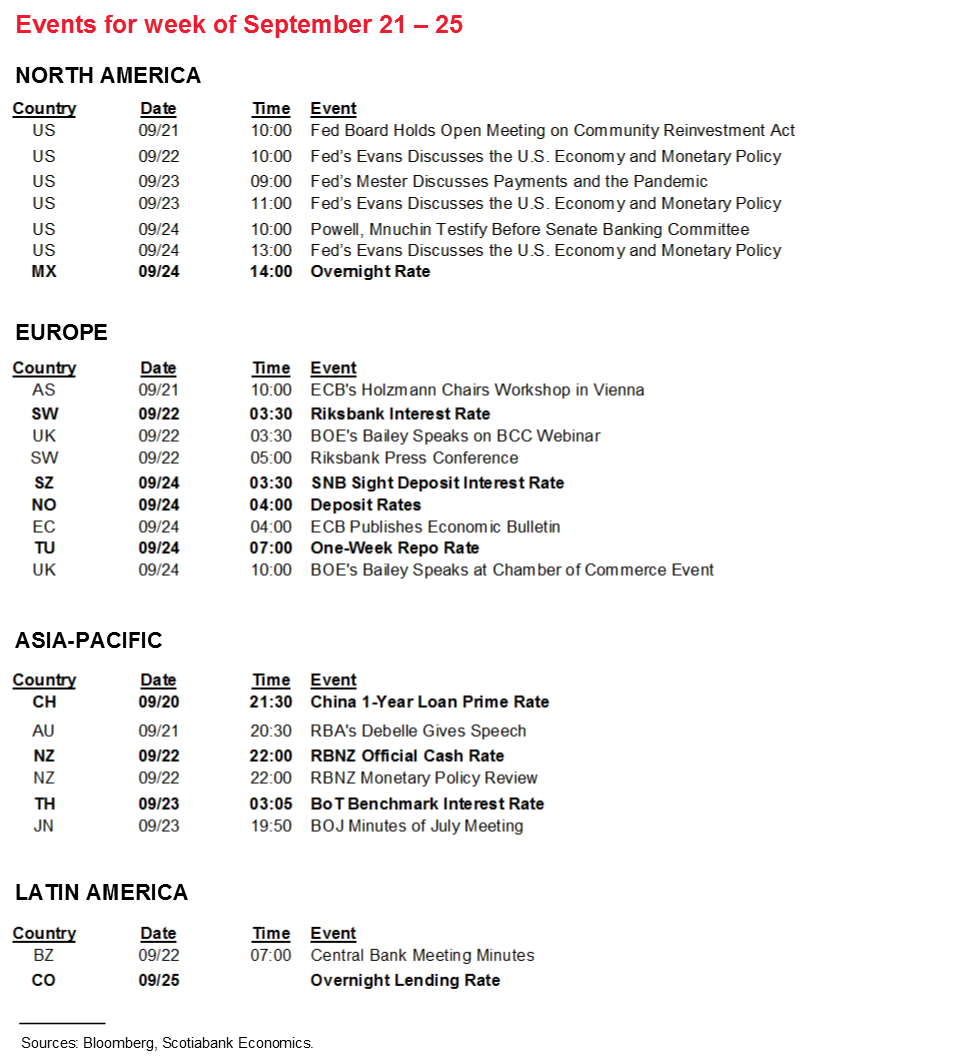

The reasons and drivers for this are likely to extend into the coming week. Nine central bank decisions and guidance from two others are likely to continue to indicate an awkward waiting game across the central bank community. They are getting tripped up by uncertainty regarding COVID-19 second waves that are emerging globally while evaluating lagged effects of what they’ve already done and whether incremental steps would be effective anyway. Governments are pondering whether they reopened too quickly and need to go in reverse. Chart 1 might suggest they’ve generally acted in moderation while cognizant of the devastation that another round of widespread closures could cause to the economy, financial distress, and hence health and social problems. Political risk is mounting from the US to UK, Canada to New Zealand. As such incremental risks evolve, there is rising uncertainty over the durability of the global economic recovery that is one part misplaced (of course indicators cool after initial reopening) but one part legitimate (if second waves, waning income supports and diminishing pent-up demand are taking root).

On the eve of the government’s throne speech, the narrative that is unfolding in Canada in this regard may be instructive to many other countries by way of the paths that various governments may choose going forward. While debt loads from pre-pandemic spending and pandemic spending mount, so does pressure on governments to address those being left behind. The social versus the fiscal deficits are so often falsely dichotomized, but Canada’s situation is constrained by large and rising twin deficits and external debt that is similar to some countries but vastly different compared to others.

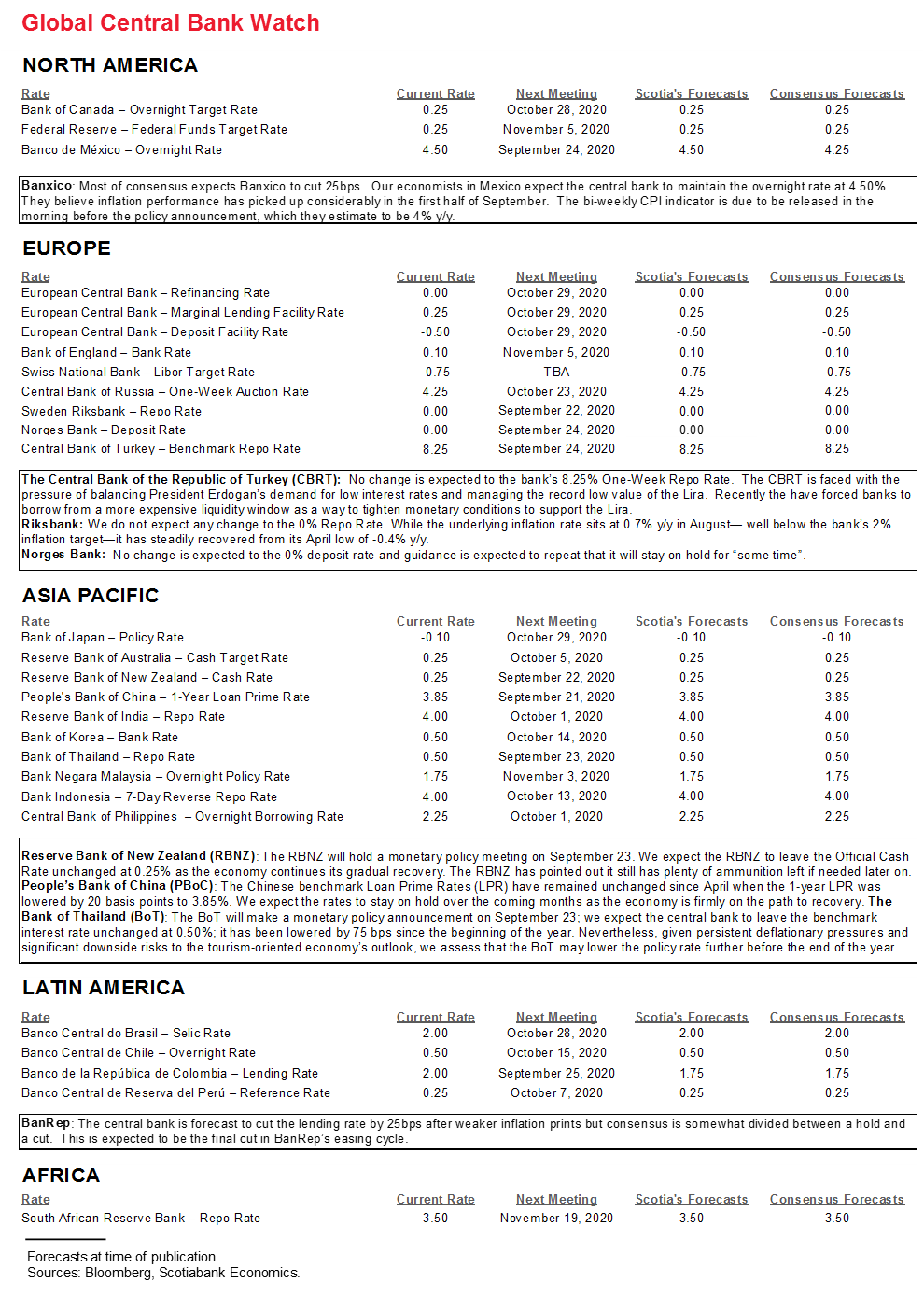

Central Banks Galore

Nine central banks will deliver policy decisions next week but they are unlikely to affect global as opposed to regional markets and even that might be a stretch. The Federal Reserve and Brazil’s central bank have recently delivered decisions but their further guidance they provide may be instructive.

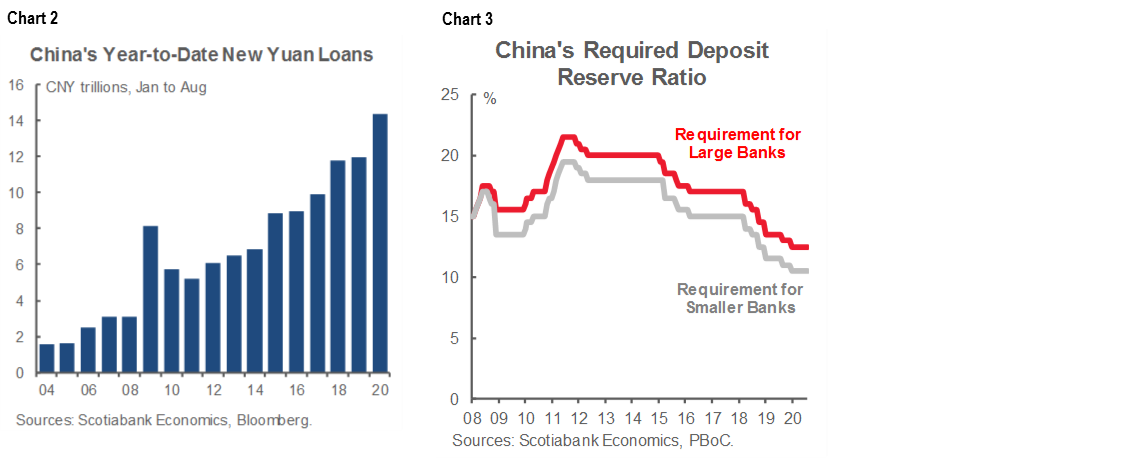

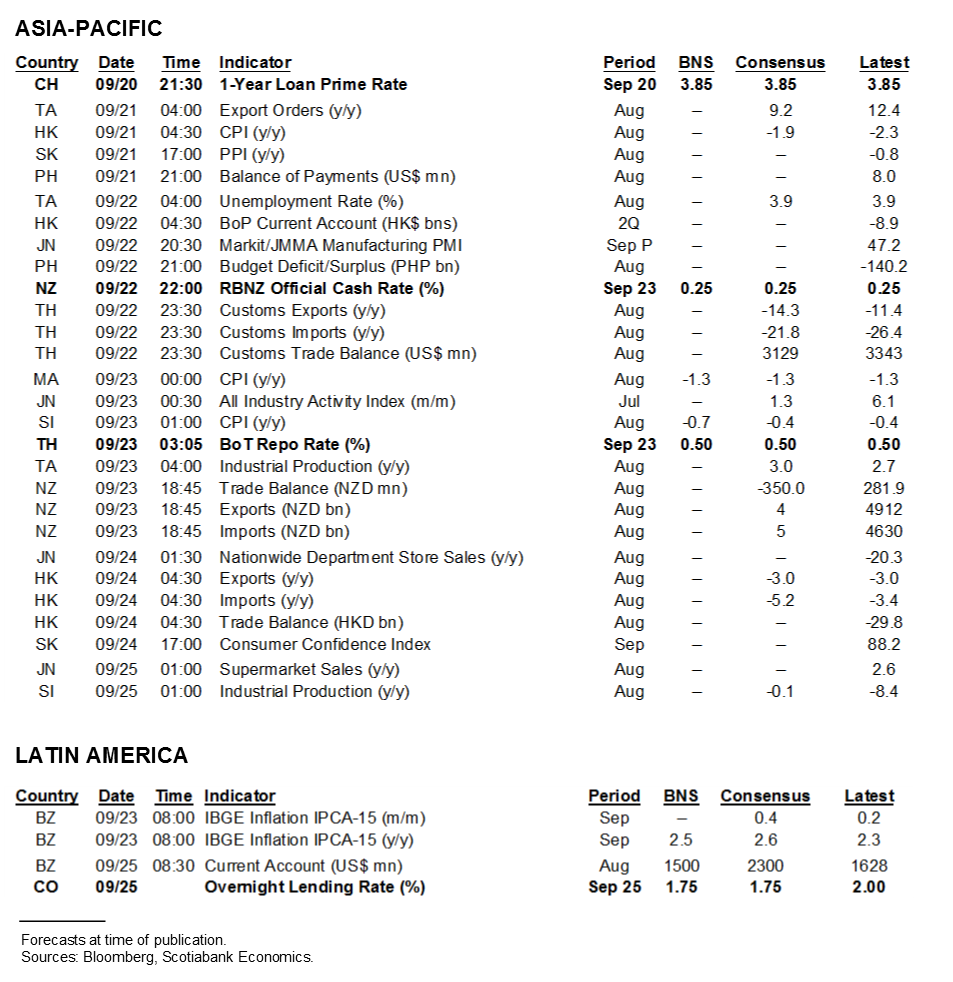

PBOC: The People’s Bank of China is expected to keep its one year and five year Loan Prime Rates on hold at 3.85% and 4.65%, respectively, on Sunday night eastern time. The central bank has been on hold since May. It has tended to rely more upon facilitating quicker credit expansion (chart 2). This has partly stemmed from a secular downward trend in reserve requirements that has been going on for most of the past decade but in accelerated fashion since April 2018 through to today in response to the bilateral trade war with the US and then the pandemic (chart 3).

Banxico: Mexico’s central bank is widely expected to cut its policy overnight rate by 25bps to 4.25% on Thursday with a minority expecting a hold. Appetite for continuing with the five 50bps cuts that have dominated easing decisions since March has likely diminished. In fact, one dissenter favoured a smaller cut at the August meeting.

BanRep: Colombia’s central bank is expected to cut its overnight lending rate by 25bps on Friday but it’s not a slam dunk with a somewhat divided consensus. At 1.9% y/y and 1.4% y/y, headline and core inflation are running well under the 2–4% target range and expected to soften further. Watch guidance on the appetite for further easing.

RBNZ: The decision on Tuesday may be a pretty straight forward and uneventful one. The RBNZ is already at the lower bound with a cash rate of 0.25%. It already expanded QE in August. It is also just four weeks until the general election on October 17th.

Bank of Thailand: Wednesday’s policy decision is expected to leave the policy rate at 0.5% where it has been since May. Policy is focused upon the trade-offs to allowing foreign tourists to return versus the risk this may incite a second wave of COVID-19 cases. Expanded fiscal supports may also take some pressure off the central bank.

Norges Bank: The often-paraphrased expression ‘been down so long everything looks up from here’ was clearly devised before anyone thought of negative rates. Norges Bank’s deposit rate sits at 0% and so Thursday’s decision is likely to be a non-event in terms of immediate action. Watch the bias which is likely to repeat that “the policy rate will most likely remain at today’s level for some time ahead” that the central bank has translated into a projected hold until into 2022 (here).

Riksbank: Ditto for Sweden’s central bank that also sits at 0% and is expected to stand pat on Tuesday. The central bank uses confidence intervals around rate scenarios to convey uncertainty over the future path of rates as shown on page10 here.

Switzerland: No change is expected to the -75bps policy rate on Thursday. The Swiss National Bank tends to shadow the ECB’s policy deposit rate.

Turkey: Thursday’s policy decision is expected to keep the one week repo rate unchanged at 8.25%. The lira’s sharp depreciation of almost 30% since the start of the year has tilted inflation risk to the upside following a heavily politically influenced series of rate cuts that dropped the policy rate from 24% in mid-2019 to about one-third of that now.

Brazil: The central bank recently held its Selic rate at 2% but next Thursday’s quarterly Inflation Report will further inform its perspectives toward inflation and macroeconomic forecasts and risks.

Federal Reserve: Fresh on the heels of its latest policy decisions and communications (recap here), the Fed is rolling out a wave of officials to provide further colour that may reveal more information on the range of opinions in support of the most recent statement. Chair Powell and Treasury Secretary Mnuchin will deliver their required quarterly testimony on the CARES Act before the House Financial Services panel on Tuesday at 10:30amET and the Senate Banking Committee on Thursday at 10amET. Chair Powell will also speak before the House select committee on the COVID-19 virus. Governor Brainard will weigh in on Monday with Governor Quarles appearing on Wednesday. Several regional Presidents will speak including Williams (twice), Evans (3 times), Barkin (3 times), Mester (1), Rosengren (1), Daly (1) and Bullard (1).

I still struggle with some of the divisions within the FOMC. For instance, when Minneapolis Fed President Neel Kashkari issued this explanation for his dissenting vote it seemed to almost backfire. Kashkari wants to make sure the Fed doesn’t raise until it’s sure that dual mandate objectives have been reached. He rightly cites the past periods when the Fed raised before being clear on this, although overstates his clairvoyance by implying he was right that hikes would ultimately backfire when he could not have known that the US would continue to escalate trade wars before the pandemic struck. Yet he defines achieving the dual mandate to be just 2% for a year with no overshoot. Nobody on the FOMC is talking about pre-emptive hikes before achieving the dual mandate, but Kashkari is setting a lower threshold than the committee consensus and trying to package that to make him sound like a dove. Further explanation would appear to be required.

Canada’s Throne Speech

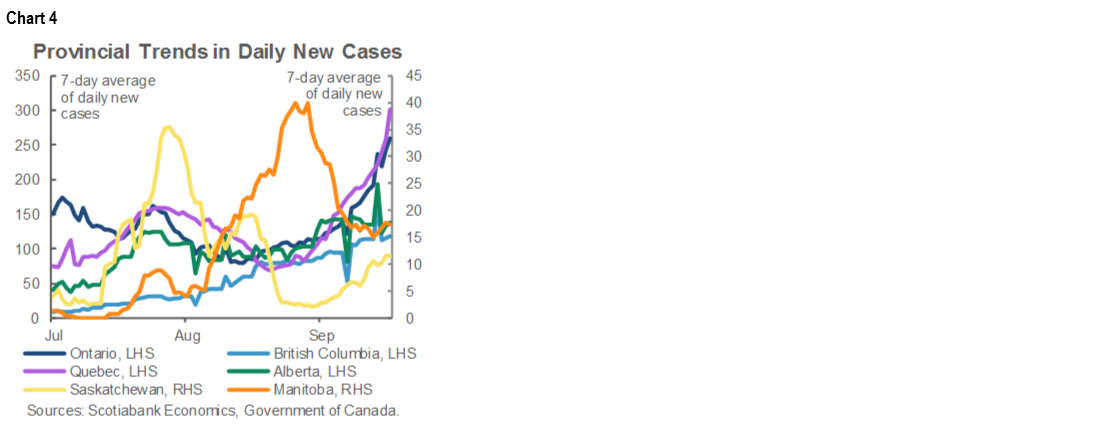

They are so much fun, why not do one every year. A great deal has changed in the world and in Canada since December 5th, 2019 when the last Speech from the Throne was delivered (recall here). Wednesday’s crack at another one will be delivered by Governor General Julie Payette as per custom. It will be set against the COVID-19 pandemic that has swept across the world and is making a resurgence in Canada (chart 4). Formally a chance to welcome back Parliament—whether after an election or, in this case, after having been prorogued amidst the Federal Liberals’ WE Charity scandal and the departure of former Finance Minister Morneau—the intent is to lay out the government’s legislative agenda. Like State of the Union speeches in the US, the British parliamentary concept of a throne speech is typically long on platitudes, generalities and wishes that may or may not translate effectively into policy. They are partisan and wordy; last year’s was over 3,300 words. They are designed to stir emotions and some discussion.

This year’s throne speech may set in motion a series of events that could result in a confidence vote and election call, although these are likely low probability risks. This view treats as a given the NDP support for the Liberals who are courting the NDP with somewhat of a turn to the left at a time when the NDP may not be in a financial position to fight another election while the Liberals step further onto their policy turf. Game theory is at work as the Liberals seek to dominate the entire centre-left spectrum.

The government is fielding a wide range of policy prescriptions like this one that advocates higher spending on child care and investment incentives and this one from former BoC Governor David Dodge (with op-ed here) that prefers to address mounting twin deficits (trade and fiscal). The challenge to the Trudeau administration will be fending off the many special interest groups seeking funding after leading them down that path with reference to once-in-a-lifetime opportunities to address social and environmental challenges. With the pandemic resurging, the prudent path may be to consider proposals but avoid over-committing should second-wave risks drive deficits much higher yet.

Growth Momentum

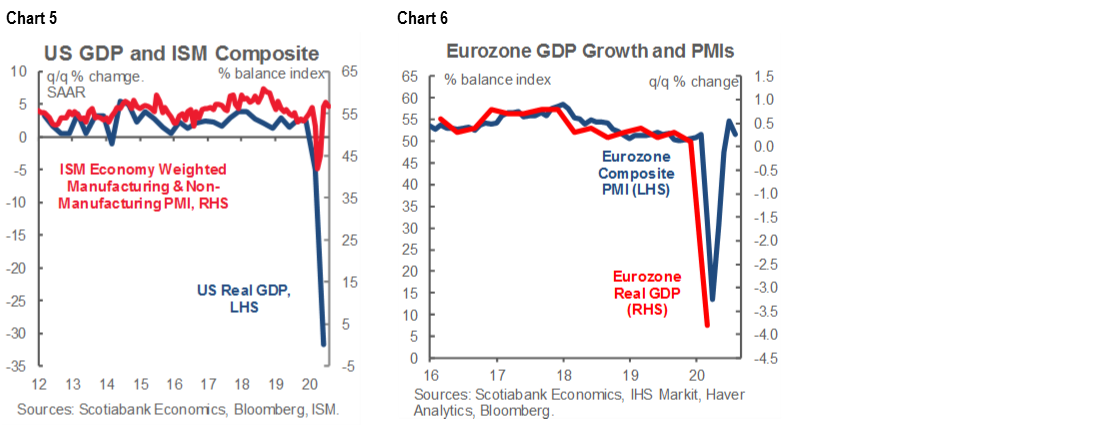

Purchasing managers’ indices are relied upon to signal what kind of momentum the economy has in light of their connections with GDP growth over time. That’s why markets will pay keen attention to three sets of September PMIs that all land on Wednesday.

The US will update the Markit versions of PMIs that day after the Eurozone, Germany, France and UK have released. Charts 5–6 showcase the correlations with GDP for the US and Eurozone. Germany will also update two other sentiment gauges that will complete the suite of such readings when it updates consumer confidence (Wednesday) and IFO business confidence (Thursday).

Extra Credit

Not to be lost in the shuffle will be several other macroeconomic readings skewed toward the US.

Housing market momentum will be informed by US existing home sales (Tuesday) and new home sales (Thursday) that are both coming off strong prior gains. Tuesday’s Richmond Fed manufacturing reading may offer insight into the next day’s Markit PMI and the ISM-manufacturing reading on October 1st that could face upside based upon the combined Empire and Philly readings. Friday’s durable goods orders are expected to show a slower pace of progress with the key being whether the trend of three months of increases in capital goods orders ex-defence and air will continue. This is part of why Chair Powell recently referred to some tentatively encouraging signals about business investment.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.