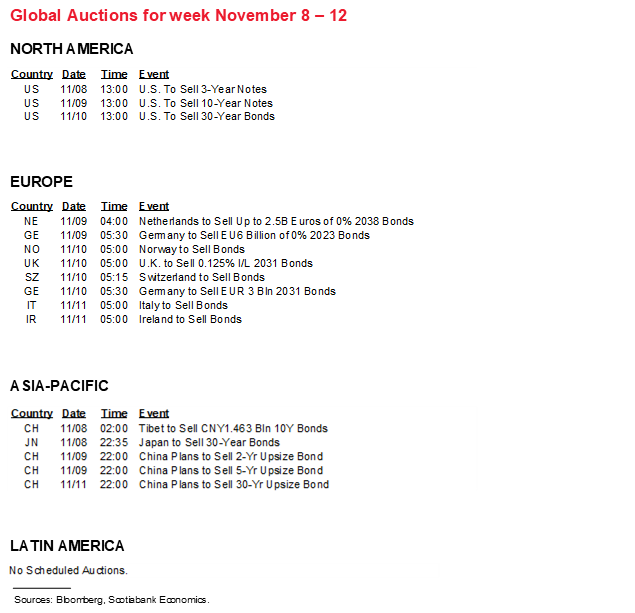

Next Week's Risk Dashboard

• US inflation: a three-decade high & future drivers

• Pending Fed appointments?

• China CPI: Chinese policy too tight?

• Canadian housing doomsters and higher rates

• CBs: Banxico, Peru, BoT

• Other CPI: Mexico, Chile, Brazil, India, Norway

• Aussie jobs rebound?

• Other macro releases

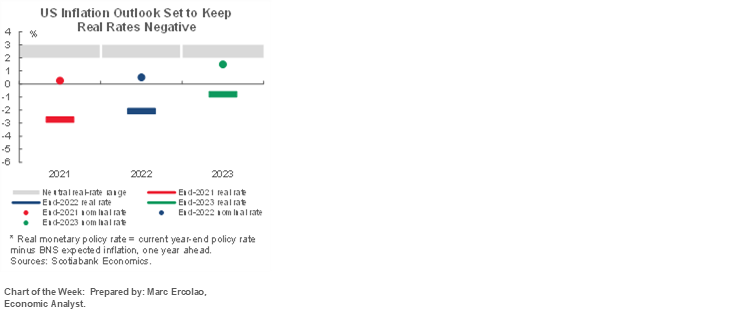

Chart of the Week

US INFLATION—HOW TO OVERCOMPLICATE SOMETHING

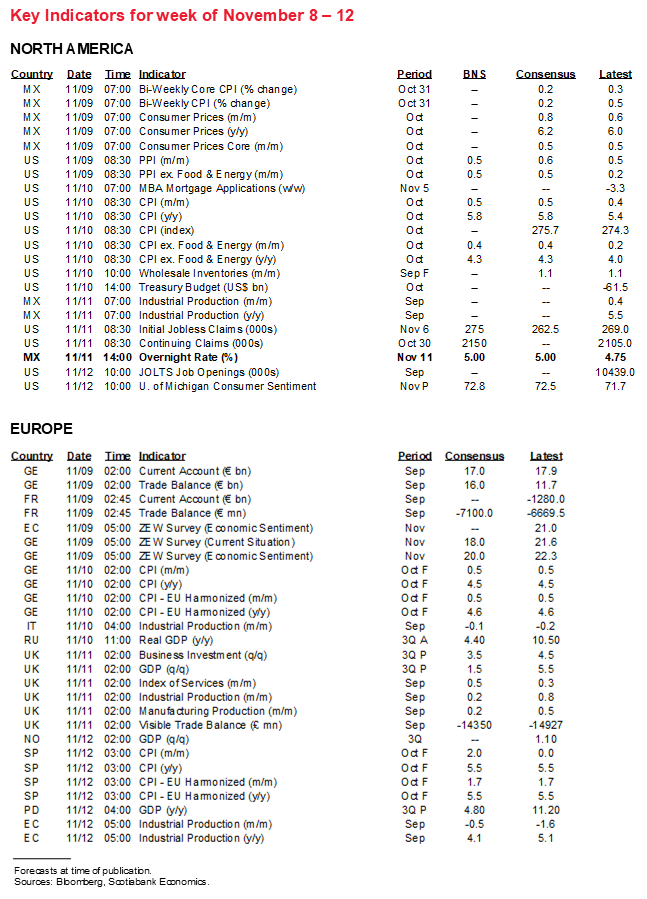

US CPI inflation arrives on Wednesday. A rise to 5.8% y/y (from 5.4% previously) seems likely and with prices up by 0.5% m/m on a seasonally adjusted basis. Core CPI is expected to rise to 4.3% y/y from 4% with prices ex-food-and-energy higher by 0.4% m/m. There is likely more upside risk than downside risk to these estimates. If the estimates are close to reality, then headline year-over-year inflation will surpass the prior peak in 2008 before lagging effects of the pandemic dragged it downward and will hit the highest rate since late 1990. Core inflation would hit the highest rate since the end of 1991.

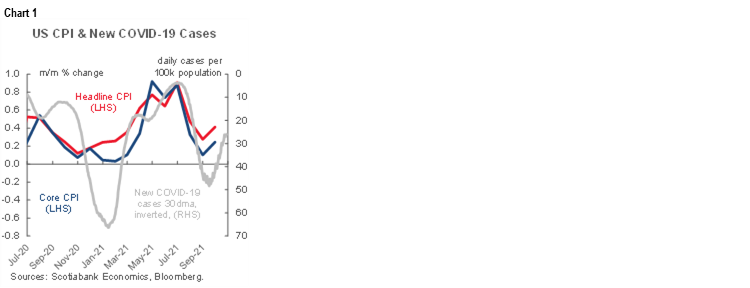

It almost seems that we’ve all been overcomplicating the inflation forecasting business during the pandemic. Endless debate over Philips curves, reopening effects, closing effects, supply chain pressures, idiosyncratic influences, energy drivers, etc. can all be replaced by one simple chart. Chart 1 that is. Ebbs and flows in recent month-over-month rates of inflation—both headline and core—are highly correlated with ebbs and flows in COVID-19 cases. The chart plots inflation the normal way but inverts the axis for COVID-19 cases in order to show the connection in the clearest possible way.

Since we’re back on the downswing for new cases, inflation is back on an upswing from the weakest point in August when Delta variant cases were raging. The continued decline in cases should mean that October’s price gains continue to accelerate after the up-tick in September.

Across other CPI drivers, base effects alone would lead to no change in headline year-over-year CPI, but core CPI would tick down to 3.9% from 4%. Seasonality would add a small amount to headline and core prices in October. Gasoline should add another small amount in weighted terms given the 3.8% weight on a 3½% m/m increase in all-grades gasoline prices. Price signals from readings such as the ISM-services measure also reinforce expectations for the resumption of inflationary pressures.

Apart from pandemic swings, there are two other main drivers of uncertainty around inflation forecasts. One is when spare capacity shuts. Having recovered all GDP lost due to the pandemic by about now, the US economy is expected to move into material excess demand over the coming quarters which should be the next leg of inflationary pressures (chart 2).

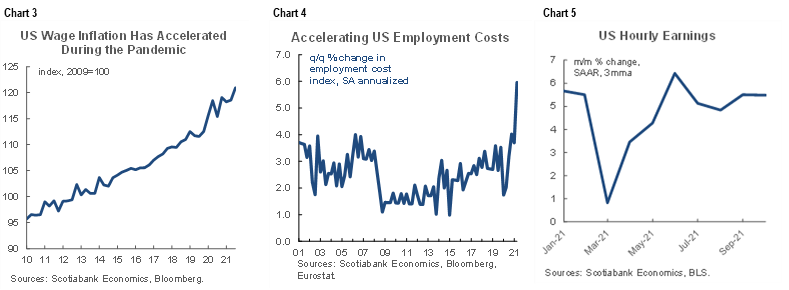

Second, wage pressures are highly evident. Unit labour costs—productivity adjusted compensation including wages and benefits—have undergone a definite slope shift toward faster rates of increase during the pandemic than before the pandemic (chart 3). They are up by a cumulative 7 ½% since the end of 2019 which means labour costs have been rising much faster than output and productivity on a trend basis. If this persists then it would be a source of inflationary pressure in ways that counter Chair Powell’s assertion that wage gains have been supported by productivity. The surge in the Employment Cost Index (chart 4) and average hourly wages from the household survey (chart 5) generally reinforce the fact that wage pressures are rising in the US economy. If so, then that makes the wage-price spiral argument an increasingly credible argument against transitory inflationary pressures.

That, in turn, is likely to raise the risks to applying further fiscal stimulus if only to set the Fed up to neutralize it. Senator Manchin’s concerns about inflation are unlikely to be diminished after Wednesday’s CPI figures.

CHINESE INFLATION—TOO TIGHT-FISTED?

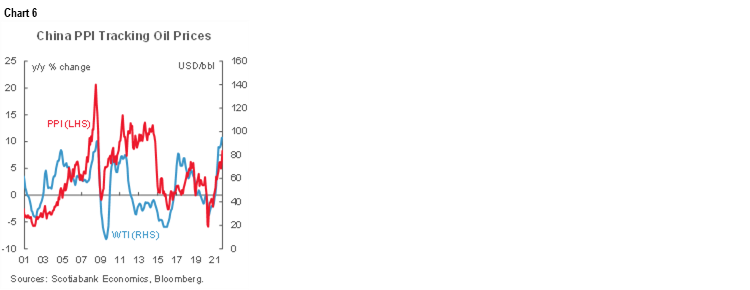

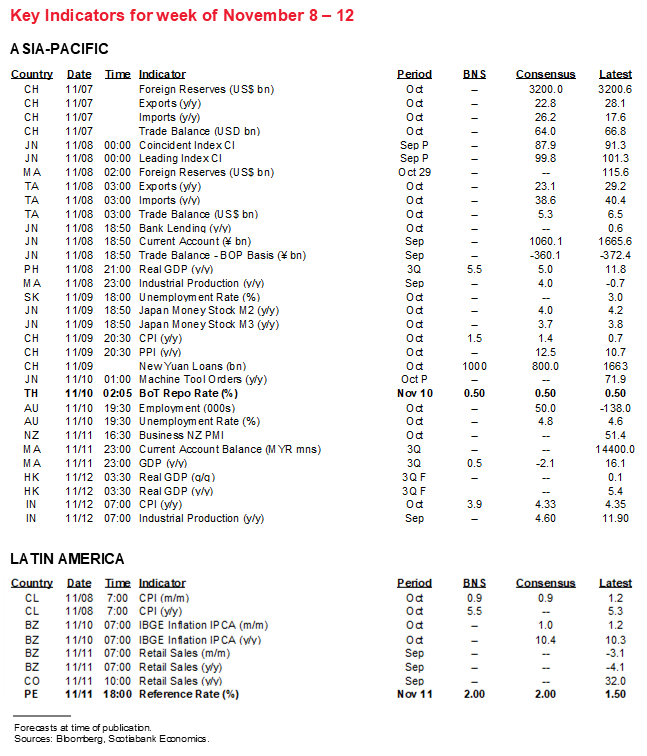

China updates CPI and producer price inflation readings for October on Tuesday night (ET). Producer price inflation is likely to continue to trend higher in keeping with oil prices (chart 6).

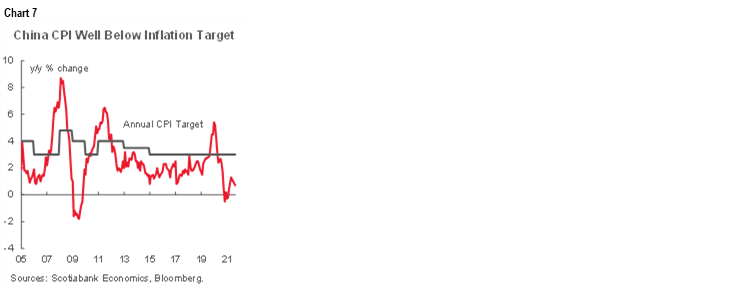

What is passing through to consumers is more important. Headline CPI has been running at just 0.7% y/y with core inflation at 1.2% y/y. Inflation is far below the state’s 3% inflation target and has been for years (chart 7). At issue is the credibility of the PBOC’s inflation target and why it is not embracing easier monetary policy. A common narrative is that China does not wish to repeat the imbalances that resulted from previously excessive stimulus coming out of the Global Financial Crisis and that Chinese authorities view policy stimulus abroad as having gone haywire. Both are fair points.

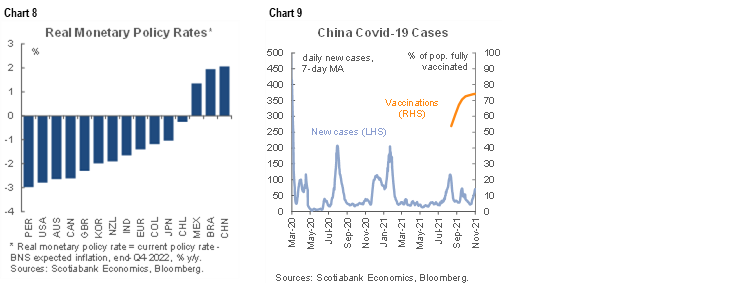

Except that perhaps the pendulum has swung too far. China’s economy is faced with a growing list of downside risks while monetary policy is setting among the world’s highest inflation-adjusted policy rates (chart 8). China’s Covid Zero approach to shutting down schools and venues at the mere whiff of a case—and despite a high vaccination rate and very low per capita cases (chart 9)—is causing a reassessment of momentum in earnings and broad near-term growth. China, it seems, remains so scarred by its initial outbreak that it has not transitioned away from a lockdown mentality toward approaches being taken in other high-vaccination countries that are relying upon alternative policies. Given China’s early experiences in the pandemic, however, it’s pretty hard to fault the country for being cautious.

Nevertheless, add Covid Zero to the country’s energy shock, ongoing risks in property finance (and not just Evergrande) and supply chain woes. Reserves continue to be stockpiled and have modestly risen during the pandemic to US$3.2 trillion. Avoiding past policy mistakes risks triggering another in the opposite direction. In all, there is an underlying market narrative that posits that heading to the exits may be premature for DM central banks such as the Fed that I don’t subscribe to, but nobody is talking about whether China’s central planners are committing policy error through an overly tight policy stance that jeopardizes ‘common prosperity’ goals. It also begs the question about what China has done for world growth lately.

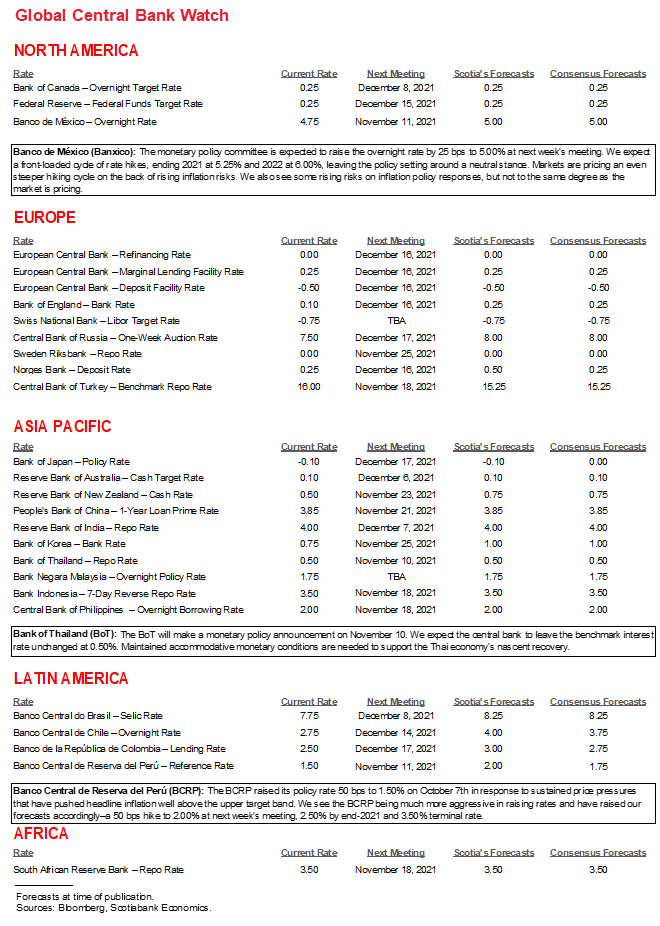

CENTRAL BANKS—LATAMS STILL TIGHTENING

A pair of hikes and a hold wouldn’t serve you well in a game of poker but is a fair characterization of expectations for a trio of regional central bank meetings next week. Major global central banks are unlikely to have much further to offer after recent policy decisions over the past couple of weeks.

- Bank of Thailand (Wednesday): Another hold at 0.5% is expected on Wednesday. The Thai baht’s 10% depreciation to the dollar since mid-February is so far doing little to generate core inflation pressures (0.2% y/y) as the tourism industry continues to struggle, but financial stability considerations are more dominant.

- Banxico (Thursday): Another 25bps hike is expected on Thursday which would take Mexico’s central bank up to a 5% overnight rate. Wednesday’s inflation reading is expected to rise again toward 6.2% y/y and any upside surprise could drive a more hawkish outcome in addition to forward guidance in favour of further rate hikes. Inflation is already far above the target (chart 10). Our Mexico City-based economists expect the overnight rate to peak at 6% by about mid-2022.

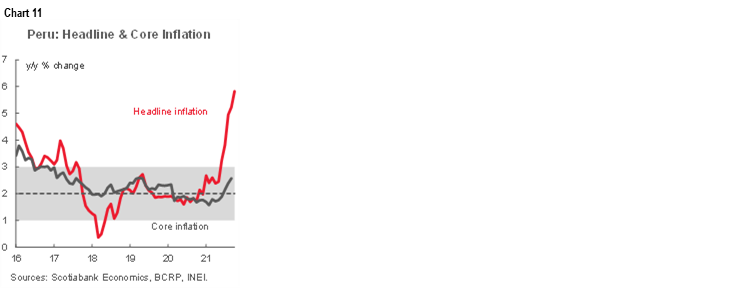

- Peru (Thursday): A 50bps hike to a new reference rate equal to 2% is expected. Lagging effects of the Sol’s 10% depreciation to the dollar this year are contributing toward inflation’s rise to 5.8% which far surpasses the central bank’s 2% +/-1% inflation target range (chart 11).

CANADIAN HOUSING AND HIGHER RATES

As individual cities continue to release home sales figures leading up to the nationwide totals for October on November 15th, they’ll continue to inform a debate over how housing markets will hold up to a rise in rate pressures in addition to how our forecasts for higher market rates will impact mortgage funding costs at financial institutions. Some say the housing market cannot withstand the effects of our rate hike forecasts and what financial markets have priced in without suffering a correction.

Let me first start by saying in response to the doomsters that you’re going to have to do better. For nearly three decades, I’ve been hearing about the imminent collapse of Canada’s housing markets and I’m still waiting.

Every threat needs to be evaluated, however, so it’s worth reviewing some of the evidence. Overall, there is ample padding in measures of household finances to take rate hikes. Our growth forecasts anticipate a mild drag effect from housing, as the whole point to tightened monetary policy is to cool interest sensitives. Our forecasts nevertheless assume a rotation of the sources of growth more toward exports and investment plus the 70% of the economy that’s in services. Monetary policy has to target broad conditions in the economy and not just one sector.

The following points work against a more alarmist housing perspective.

- Our forecast is for rising short-term borrowing rates to go up 200bps over 2022–23 starting next summer. The underlying Government of Canada bond yield is forecast to rise by a total of about 150bps from this past September’s levels to the end of 2023 and so fixed rate mortgages will likely rise more slowly than variable rates.

- It will therefore take ~2 years to get back to interest rates that are more neutral and only about 50bps above pre-pandemic levels. Housing moderated but survived back then.

- It will then take years for the effects of higher rates to reprice existing mortgages given lagging effects on refinancings and renewals. During this period, we expect job and income gains to be offsetting from an affordability standpoint. The connection to how higher mortgage rates will feed into CPI involves much shorter lags of about 1–2 years.

- Households had to qualify at the stress test levels for rate shocks within OSFI’s B20 provisions. That means qualifying at 5.25% or the contractual rate plus 200bps, whichever is higher. B20 therefore invokes an automatic rate shock in the qualifying process. Existing mortgages should be well positioned to meet this shock.

- For new mortgages, it’s unlikely that the best offers on mortgage rates now plus 200bps will come to sharply surpass the existing 5.25% B20 qualifying rate as higher fixed borrowing costs are factored in. We’ll be monitoring whether OSFI and the Minister of Finance will see fit to adjust how the B20 stress test operates conditional upon housing’s evolution.

- Of course, if existing mortgage borrowers after qualifying then turned around and spent the difference in interest payments at the stress test threshold and the actual contractual rate at the casino then that’s clearly not so good. The evidence suggests households generally behaved more rationally. The saving rate of 14% in Q2 has moved sharply higher during the pandemic due to risk aversion and goods shortages (chart 12).

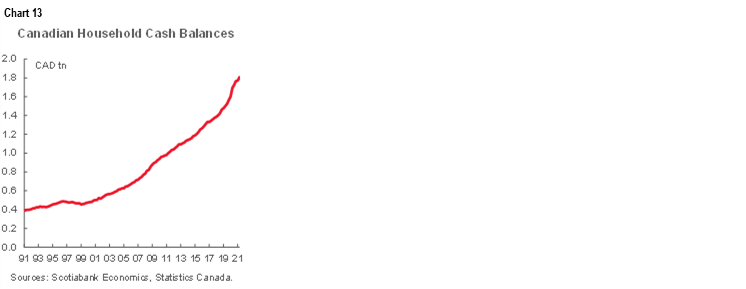

- Further, large cash and liquidity balances on household balance sheets are now 16% higher than they were before the pandemic struck (chart 13).

- Home equity on the Canadian household balance sheet is very high at over 76% of the value of the real estate assets which is a record high (chart 14) and offers substantial padding around price risk.

- The household debt service burden has fallen during the pandemic partly due to lower rates and income supports and Canada has fully recovered lost jobs (chart 15). It will likely take years to get back to pre-pandemic debt service burdens alongside phased-in rate hikes.

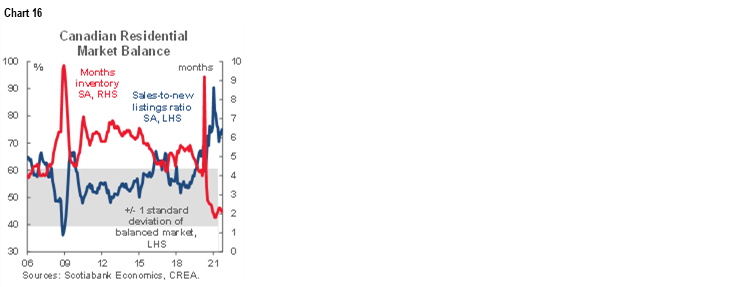

- Housing supply remains very tight. Cooler demand can be accommodated by tight supply conditions (chart 16).

- And last but not least, Canadians have a long and well understood history of paying our mortgages (chart 17). Pandemic-era policies helped keep households whole on cash flows and avert earlier fears on what would happen to delinquencies.

OTHER MACRO—DIAMONDS IN THE ROUGH

The rest of the week’s line-up is short on potentially jaw-dropping moments for global markets but contains a few gems.

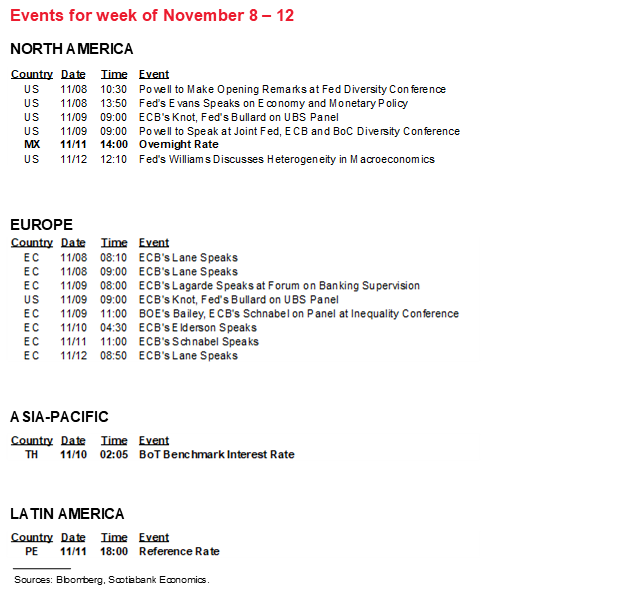

The dominant focus for US observers will be upon the possibility we hear an announcement on appointments to the Federal Reserve given reports that Chair Powell and Governor Brainard have held meetings with President Biden. Fed-speak will also focus upon Vice Chair Clarida’s remarks on monetary policy prospects on Monday, low risk around two appearances by Chair Powell at a diversity conference, and several other Fed speakers. Discord within the Democrats toward plans to offer additional fiscal stimulus will also be monitored. Apart from CPI (noted above), the rest of the release schedule will be light and only includes UofM consumer sentiment on Friday, producer prices on Tuesday, weekly claims on Thursday and the JOLTS job vacancy measures on Friday. The US Treasury market will be shut on Thursday, but stock markets will remain open.

While CPI will capture most of the attention regarding China, exports during October arrive this weekend and are expected to post cooler growth partly on COVID-19 restrictions and supply chain problems. We might get financing figures for October this week (if not, then the following week).

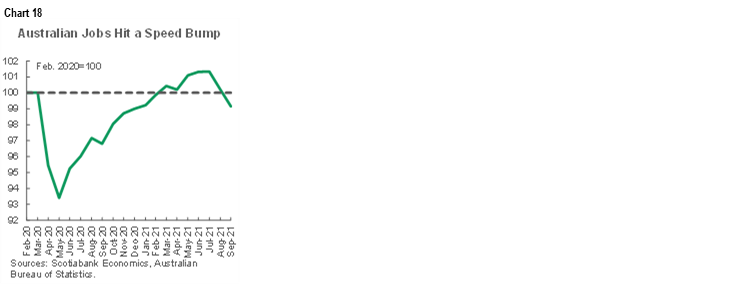

Australian employment figures for October will be updated on Wednesday night (ET). The Aussie labour market is poised to regain a small portion (consensus +50k) of the -284k jobs lost over the months of August and September. Lockdowns and restrictions eased throughout October, which should lead to a more material gain in November employment. It is still early, but market participants will be on watch for how recapturing of jobs and participation rates move the unemployment rate, which could subsequently lead to upward wage pressures in the near-term. Chart 18.

Canadian bond markets will be shut for Remembrance Day on Thursday while equities will remain open. BoC Governor Macklem delivers another Sunday interview on CTV at 11amET and then speaks on Tuesday, but only to deliver closing remarks at a diversity forum. The BoC releases its Survey of Senior Loan Officer Opinions on Friday, but it rarely captures market attention. There are no material macroeconomic releases on tap, but 75 TSX-listed firms will release earnings.

Limited European releases will focus upon German exports (Tuesday) and the ZEW investor confidence measure (Tuesday) which kicks off the main survey-based evidence on the economy’s performance during November that subsequently reveals readings for PMIs and IFO business confidence. The UK also updates exports, its services index and industrial output on Thursday.

Inflation figures will also be updated by Chile (Monday), Norway and Brazil (Wednesday), Mexico (Thursday) and India (Friday). Philippines and Malaysia update Q3 GDP next week as well.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.