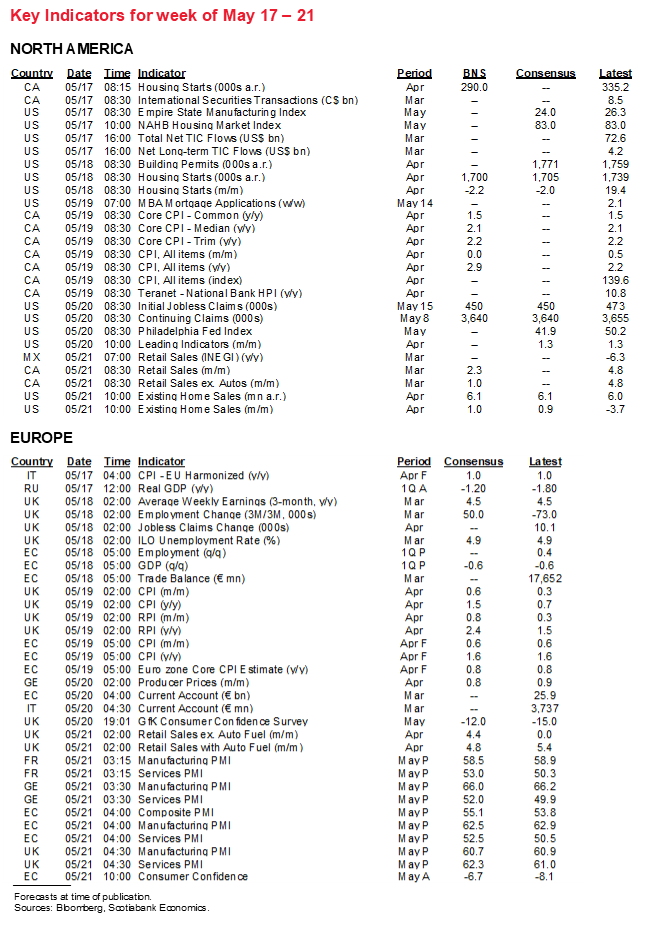

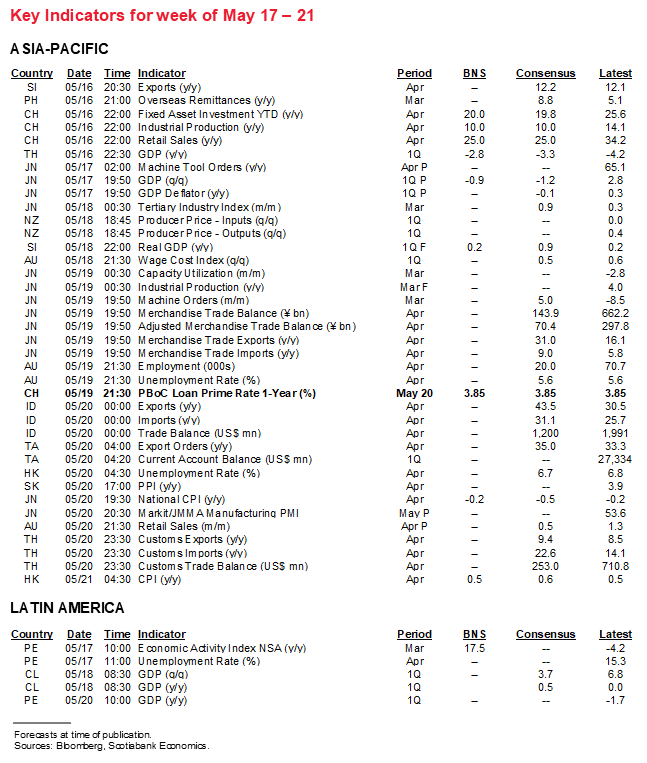

Next Week's Risk Dashboard

• The UK’s grand experiment

• Why Canada’s inflation differs from the US

• A UK inflation turning point

• FOMC minutes: dissenting taper talk?

• RBA minutes: further stimulus hints?

• Jobs: Australia, Eurozone, UK

• PMIs: US, Australia, Japan, Eurozone, UK

• CBs: FOMC minutes, RBA minutes, PBOC

• GDP: Eurozone, Chile, Peru, Japan, Thailand

• Retail sales: UK, Canada

• Housing: Temporary Canada-US divergence

Chart of the Week

THE WORLD IS WATCHING THE UK EXPERIMENT

The UK is embarking upon an experiment that will be closely monitored across the world. How this impacts inflation will be one among many perspectives on the issue at hand.

UK CPI inflation for the month of April will also have its own idiosyncratic drivers when it lands on Wednesday. For one thing, base effects should play little to no role in this case. Taking the March 2021 CPI index level over the April 2020 CPI index level would leave April headline inflation similar to the prior month’s 0.7% y/y reading. That’s rather different than the circumstances in the US and Canada.

If the UK were to see higher inflation in April then, barring revisions, it would have to come from month-over-month price changes as restrictions and lockdowns ease. That seems likely in such fashion as to pop the year-over-year inflation reading toward roughly double what it was the month before, and further easing effects are ahead in CPI reports over April through June.

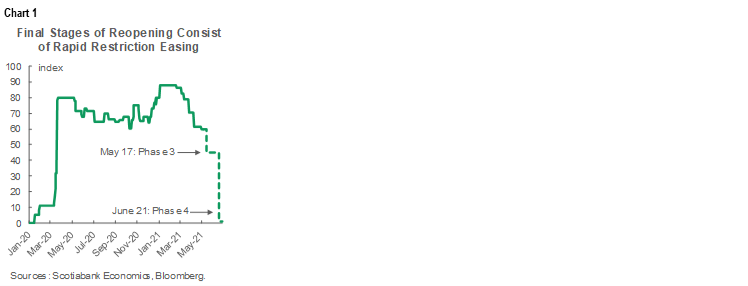

Recall that back on February 22nd PM Johnson outlined a four-step plan to end restrictions by June 21st. The first step reopened schools and colleges on March 8th followed by relaxed outdoor gatherings on March 29th, the reopening of non-essential shops on April 12th, the relaxation of indoor restrictions and the further relaxation of outdoor restrictions on this coming Monday May 17th and then full relaxation of restrictions by June 21st. The result could well return the “stringency index” which records the strictness of ’lockdown-style’ policies that primarily restrict people’s behaviour back toward the easiest conditions of the pandemic (chart 1). Johnson has said it remains possible to stay on track with this plan, though remarked that he sees “a real risk of disruption in new variant.” An emerging risk concerns the arrival and “widely seeded” India variant and the UK Chief Medical Officer Chris Whitty’s expectation that this will become the dominant strain within the UK.

Needless to say, this experiment in a major economy will be closely watched around the world to see if COVID-19 cases stay down and to observe how people behave and reengage with the economy. Success or failure in the UK could portend developments elsewhere.

INFLATION—CANADA IS DIFFERENT FROM THE US

So, Canada is just America, only (often) colder with less inequality and with way better beer, right? Not so fast. We might see some unique differences shine through in Canada’s CPI inflation report for April compared to the recent US CPI report. On balance, I wouldn’t expect the same barn burner of a report north of the border compared to what we just saw in the US.

In fact, it might be that the only parallel between inflation readings in the two countries may be the base-effect argument. Canadian headline CPI is likely to rise toward 2.9% y/y from 2.2% y/y the prior month entirely because the year-ago reference point shifts to April 2020 when the price level fell outright at the early stage of the pandemic. My estimates assume that we won’t get much of any other influence on CPI such that the year-ago reading will be 2.9% and the month-over-month measure in seasonally unadjusted terms as per Canadian custom will be 0%.

Here are several differences to consider that may point to materially less upward pressure on prices in Canada than in the US especially in month-ago terms.

1. There won’t be a reopening effect like there was in the US as Canada tightened restrictions through April. US CPI wasn’t only a reopening report, but components like lodging and airfare were materially stronger because of the effect and that’s unlikely to occur in Canada. Another way this will impact prices is via gas prices that didn't get a usual seasonal up-tick in Canada as mobility usually improves in Spring.

2. No effects from stimulus cheques. Sorry, Uncle Joe forgot about us. Americans are likely to share their bounty from two rounds of cheques so far this year, but they’ll do so indirectly through importing more. Canadians won’t get this spare cash effect to drive anything like the massive gain in US retail sales.

3. The two countries evaluate core inflation in very different ways and, as a result, the year-over-year change in Canada’s core rate won’t be subject to the same base effect pop higher that occurred with core PCE in the US. The Bank of Canada’s preferred core measures might not change much at all. Canada uses central tendency measures of core inflation like trimmed mean CPI, weighted median CPI and common component CPI. The trimmed mean gauge is a monthly compounded rate of change over twelve months after stripping out the top and bottom 20% of the basket of prices each month. The weighted median compounds the price change at the 50th percentile each individual month over twelve months. The common component is factor-driven and designed to evaluate common drivers of price changes. A common approach is to average them. Upon doing so, it isn’t a simple exercise in just shifting the year-ago reference point forward a month to when many prices fell in April of last year.

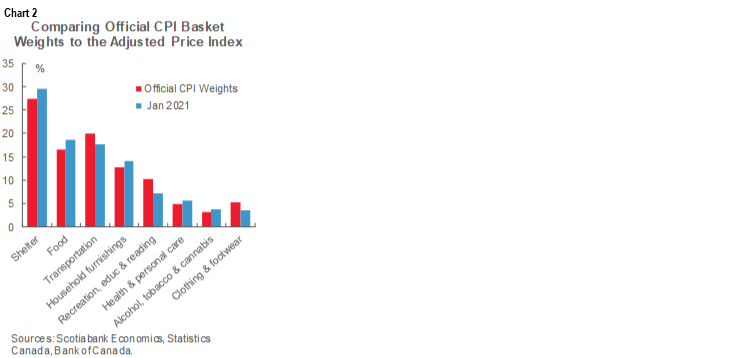

4. Be sure to add roughly a half percentage point to the official year-over-year CPI reading next week to get a more accurate number. Canada is slowly adapting to a different way of making CPI respond more rapidly to changes in consumption patterns as a makeshift way of addressing shortfalls relative to US PCE inflation measures that dynamically track changes in consumption patterns and weights on prices over time. The official Canadian CPI reading is based upon the composition of spending that existed back in 2018 and is normally updated every two years. The pandemic blew that off track and the shifts in consumption patterns made those earlier spending weights less relevant to today. That’s why Statistics Canada has been publishing unofficial ‘shadow’ CPI estimates that reflect estimates of today’s spending weights. These updated weights are not available for the full suite of spending categories that are necessary to accurately update the core measures of inflation but the subcategories that are available are shown in chart 2. The year-over-year shadow rate has been tracking 0.4%–0.5% above the official measure over recent months. The shadow measure will become the official measure with the June CPI report released in July. For now, be cognizant of the fact that 0.4% or so should be added to the official measure to get where the true headline inflation rate is tracking. So, for instance, the 2.2% y/y rate in March was more like 2.6% y/y and next week’s measure will likely cross 3% and hence the upper end of the BoC’s 1–3% flexible inflation targeting band. See the cover chart on the front page of this publication for a depiction of this. Also note that the updated more detailed weights may result in changing tracking of the core inflation measures with a bias to higher readings by July.

CENTRAL BANKS—STILL NOT TALKING?

Ahhhh, peace. Wait a minute, there’s no such thing in the markets. Ok, let’s just settle for little by way of central bank action over the coming week. No protests here!

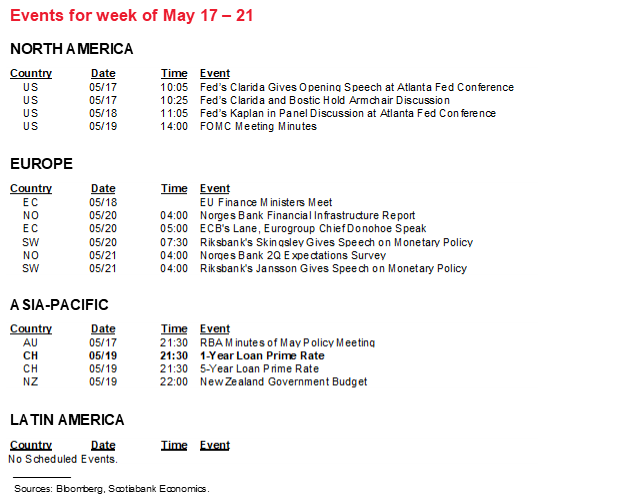

FOMC Minutes

Remember the April 28th FOMC statement and press conference? That’s ok. It wasn’t terribly memorable anyway and the Fed was likely quite fine with that! A recap is available here. Oddly enough, however, there were some out there who had thought Chair Powell might start to broach the topic of tapering on that day so when he did not there was a mild rally in Treasuries and stocks gained a bit. When asked during the press conference whether it was time to “start talking about talking about tapering” Powell simply said “no, we’ve said we would talk well in advance and it is not yet time to do so.”

I wouldn’t be surprised to see the minutes reveal that there was indeed a discussion around tapering regardless of what Powell indicated. A small risk is therefore focused upon the extent to which other FOMC officials agreed with him at this meeting and we already know that Dallas Fed Kaplan (nonvoting 2021–22, voting 2023) leans toward having such a discussion while others have more recently indicated that, while now is not the time, they will be monitoring developments including inflation and jobs numbers over the coming months (e.g. Waller, Bullard).

I have a lot of time for Kaplan’s willingness to step forward and risk being pilloried by his colleagues. The Fed’s fallible history from the Great Depression through 1970s inflation and the early 1980s about-face straight through to the pre- and post-GFC era serve as appropriate cautions against unquestioning faith in its ability to engineer a perfect soft inflation landing this time around.

RBA Minutes

Minutes to the Reserve Bank of Australia’s meeting on May 4th will be divulged on Monday night (always eastern time references in this publication). They too could spice it up a bit with a further dialogue on conditions and possible parameters around expanding stimulus, though this is more likely to occur later. Recall what the RBA said at that meeting:

“At its July meeting, the Board will consider whether to retain the April 2024 bond as the target for the 3-year yield target or to shift to the next maturity, the November 2024 bond. At the July meeting, the Board will also consider future bond purchases following the completion of the second A$100B of purchases under the government bond purchase program in September. The Board is prepared to undertake further bond purchases to assist with progress towards the goals of full employment and inflation.”

PBOC On Hold

The People’s Bank of China will likely keep its one-year Medium-Term Lending Facility rate unchanged at 2.95% and its de facto policy rates—the 1-year and 5-year Loan Prime Rates—also unchanged at 3.85% and 4.65%, respectively, on Wednesday night.

MACRO RELEASES

A fairly active week lies ahead for global macroeconomic indicators ranging from PMIs to GDP growth, jobs to retail sales and on to North American housing market conditions.

i. GDP & PMIs—Something Old, Something New

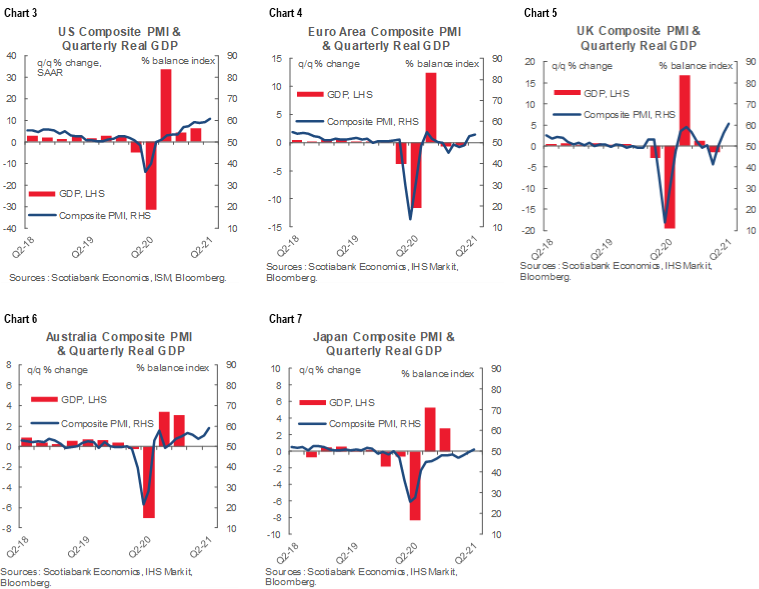

The coming week will improve our understanding not only of how some regions of the world economy performed during Q1 of this year but also how they continue to perform throughout the second quarter. Charts 3–7 serve as reminders of the linkages between global purchasing managers’ indices and GDP growth.

This interplay will be informed by Q1 GDP readings out of a few economies. Japan’s economy is expected to contract again when Q1 GDP arrives on Monday night. The drop is expected to be led by consumption but watch Japan’s PMIs for May on Thursday night to see if recent progress continues.

Eurozone GDP contracted by 0.6% q/q non-annualized in Q1 and we’ll get revision on Tuesday, but the end of the week’s PMIs for May will hopefully confirm expectations for improved momentum through Q2.

After the UK economy contracted by about 1 ½% q/q non-annualized in Q1, a strong rebound is expected during Q2 and Friday’s PMIs for May are likely to drive that message home with improved growth as the economy reopens.

Australia’s May PMIs (Thursday) should continue to indicate solid growth with a composite reading in the upper-50s reaffirming the recent acceleration.

The US is rather more of a wildcard of sorts. Another round of monthly regional Fed surveys kicks off with the Empire gauge for May on Monday, followed by the Philly Fed’s measure on Thursday and then Markit’s PMIs on Friday. These are difficult calls with probably more downside than upside given ongoing supply chain bottleneck issues.

Also watch for Q1 GDP estimates from Thailand (Wednesday, contraction), Chile (Tuesday, our Santiago team expects -0.3% y/y) and Peru (Thursday, our Lima-based economists expect 3.2% y/y).

ii. Jobs—The Start of Better Things to Come for the UK?

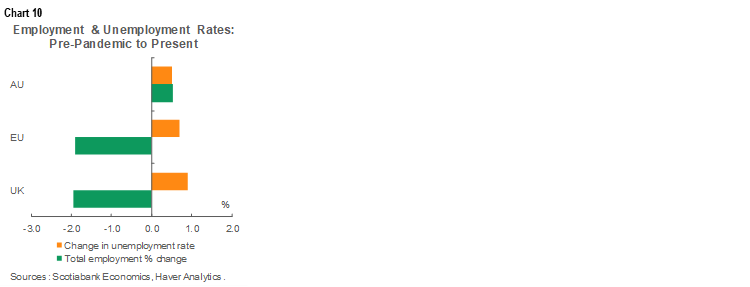

Could this finally be a turning point for UK jobs? There was a glimmer of hope in the February jobs numbers that edged very slightly higher, but unlike countries like the US, Canada and Australia, there has been no notable recovery in UK employment...yet (chart 8). March’s figures could add to some momentum as the economy gradually reopens before the reopening process outlined above should drive more rapid gains over subsequent months.

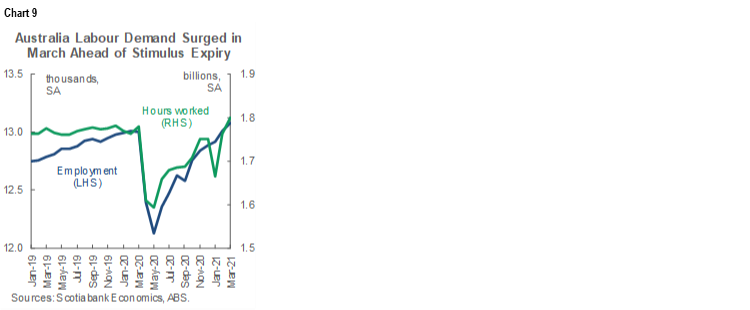

Australia has already recouped all jobs and hours worked lost to the pandemic and is likely to continue to build upon that track record in Wednesday’s figures for April (chart 9), but the reason the RBA remains dissatisfied is that the unemployment rate remains somewhat higher than it was before the pandemic (5.6% versus 5.1%). Nevertheless, the participation rate is at a multi-decade high of 66.3%. Overall, it’s unclear that the job market requires another round of RBA bond buying when the current batch ends in September unless they do indeed expand purchases again in July but inflation continues to track well below the RBA’s 2–3% target range.

With the Eurozone economy having contracted in Q1, don’t expect great things for Tuesday’s employment report. Like the UK, the party hasn’t started (chart 10).

iii. Retail sales—UK and Canada Likely to Diverge

This could be a relatively good week for the world’s retailers. Or rather, they would already know that to be true or not on a general basis, but we’ll find out the hard evidence at the macro level for several economies.

Canada (Friday) has already issued ‘flash’ guidance that retail sales back in March climbed by 2.3% m/m. Apart from any revision to that estimate, the more important matter may be how badly flash guidance for sales probably slipped during April given widespread third wave restrictions.

As previously noted, the UK economy is reopening and so there are fairly widespread expectations for Friday’s retail sales print for the month of April to post another large gain on the order of 4–5% m/m.

There is somewhat less conviction that Australian retail sales will be able to post another rise when April’s figures arrive on Thursday night (ET). Just under a quarter of consensus has gone against the median estimate for a modest gain.

Mexico will also update retail sales for March (Friday) and, in China’s case (Monday), be careful toward April’s reported figure in that the year-ago rate is likely to begin to fall back down but only because the year-ago reference point will become gradually less favourable than it was in March of last year. That same advice may also apply to Chinese industrial production (Monday).

iv. Housing—Canada and US to Temporarily Diverge

Canada will update existing home sales and housing starts for April on Monday. Both are likely to retrench. Housing starts hit an all-time high in March partly on the catch-up to earlier softness and perhaps partly in anticipation of further tightening of restrictions. They are likely to fall back and perhaps quite markedly given various nationwide restrictions. Home sales probably also fell based upon reports from a select number of cities to date. Tighter restrictions into lockdowns with stay at home orders and banned open houses will do that. Those restrictions are likely to last through May and into early June after which there may be a burst of pent-up buying activity.

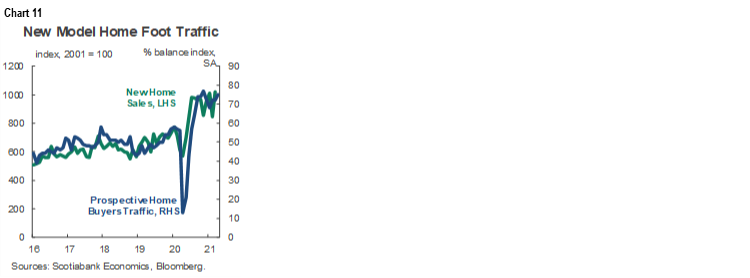

A trio of US housing readings will also be on tap. Watch US homebuilder confidence (Monday) for an early indication of appetite for buying new homes as the economy reopens through the measure of prospective home buyers that proxies the number of folks visiting model homes (chart 11). Housing starts in April probably gave back some of the prior month’s massive 19% m/m gain (Tuesday). Existing home sales might rebound a bit from the prior month’s weakness (Friday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.