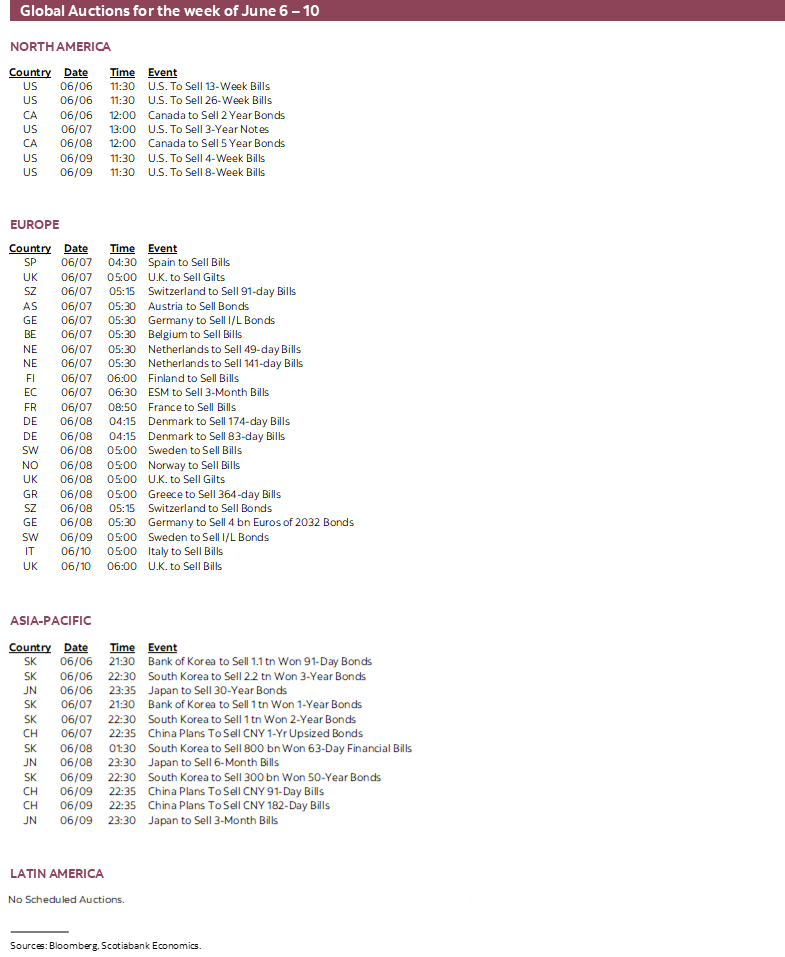

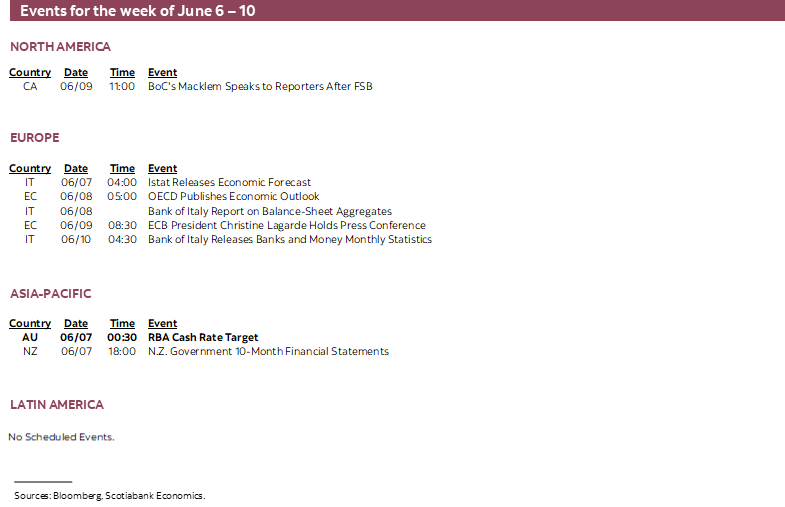

Next Week's Risk Dashboard

• ECB to tee up stimulus exits

• US inflation is still climbing

• Canadian jobs rebound?

• Chinese CPI to showcase Fed-PBoC divergence

• RBA to deliver another hike

• RBI is in a sudden rush

• Chile, Peru are still raising rates

• BoT has yet to join global tightening

• Russia’s CB to cut on phony ruble strength

• LatAm CPI

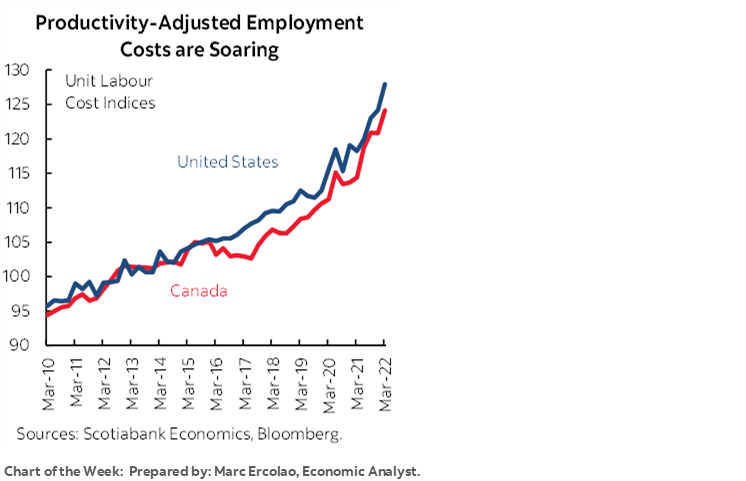

Chart of the Week

Inflation and what to do about it will be the dominant focal points this week. Seven central banks are under pressure to make fresh decisions and will be led by the ECB as the Fed digests another hot inflation reading during blackout ahead of its own full meeting with revised projections the following week.

US INFLATION—STILL NOT COOLING

US CPI inflation will be updated for May on Friday to potentially end the week with a bang. Another hefty rise in prices is expected.

A rise of approximately 0.9% m/m in seasonally adjusted terms is likely. The seasonally unadjusted rise would be a touch higher given that the month of May typically involves some seasonal price pressures. Such a seasonally unadjusted gain combined with base effects could on net be enough to lift the year-over-year rate a little higher to about 8½% y/y from 8.3% the prior month. This view is somewhat above consensus expectations again.

As for the drivers:

- The shift in year-ago base effects would push inflation downward all else equal to about 7.4% y/y.

- All else is not equal, and so among the upsides are May seasonality over April.

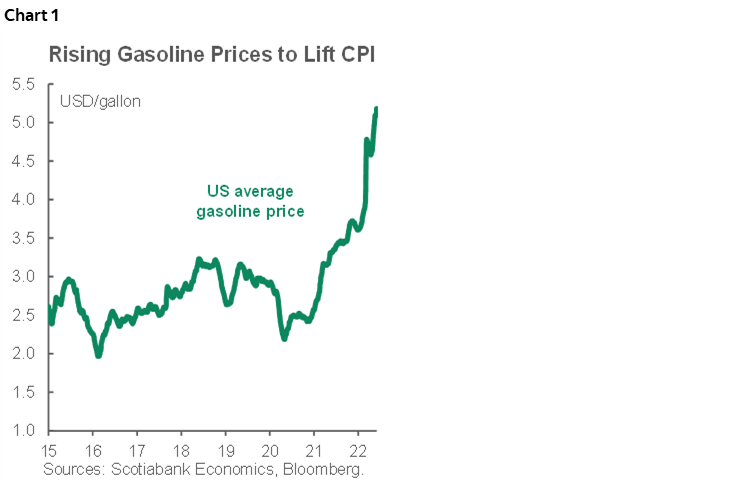

- There was a strong 8% m/m rise in unadjusted all-grades gasoline prices that gets tamped down to about half that after seasonal adjustment while the trend remains pointed sharply higher (chart 1).

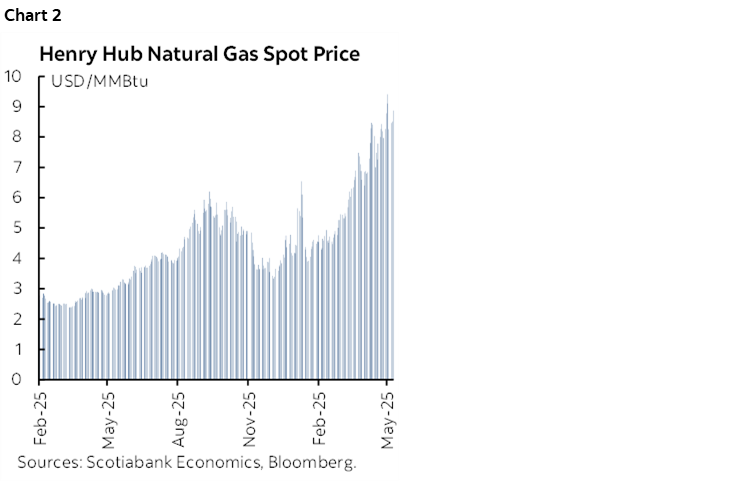

- Natural gas prices were up another one-quarter over April which despite the very small weight should still make a meaningful contribution to price pressures (chart 2).

- New vehicle prices appear to have fallen by just under 1% m/m NSA according to industry guidance and used vehicle prices appear to have risen by enough to offset the new vehicle decline.

- I’ve assumed food prices climbed again in accordance with efforts to weight food prices according to the consumption basket.

- There is also likely to be another positive reopening effect on high-contact service prices like airfare, travel and lodging, car rentals, take-out and dine-in food prices, etc.

As for core CPI inflation, 6% y/y and 0.5% m/m NSA and 0.5% m/m SA are expected. If these estimates are on the mark, then inflationary pressures will be showing no signs of cooling. The monthly gain in headline CPI could remain toward the upper end of the multi-decade experience.

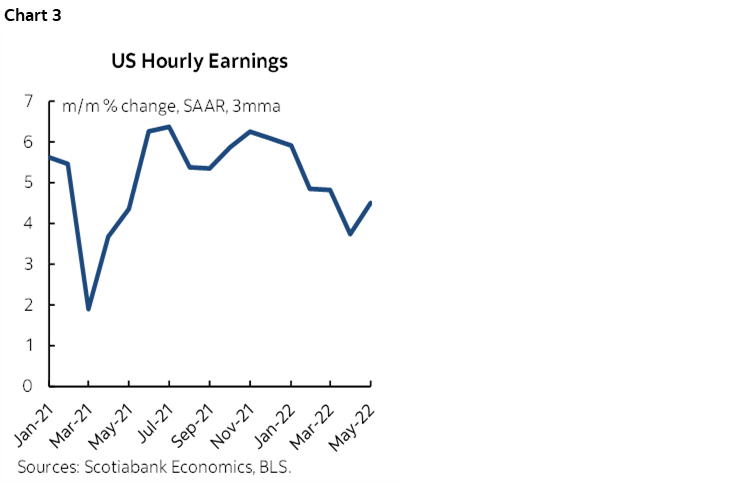

At issue in determining whether inflation is close to peaking, however, is how to define it. Year-over-year won’t inform this debate and focusing upon base effects has already done enough damage to the quality of discourse around monetary policy developments during the pandemic. Continue to watch the month-over-month seasonally adjusted price increases at an annualized rate which have continued to be very high. The three-month moving average measure was 10% in April (chart 3).

CANADIAN JOBS—RRRREEEEEBOUND?

Canada updates job market figures for May on Friday. I’ve gone with an estimated gain of 50k that would dip the unemployment rate a touch lower. Wage growth will also be key.

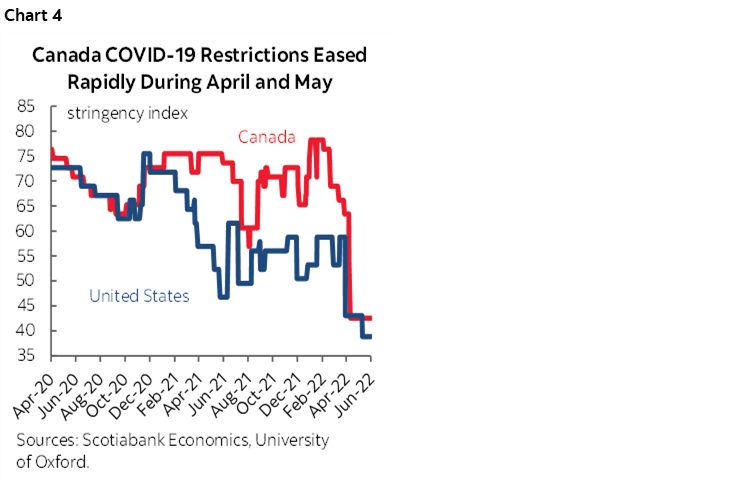

Recall that the prior month posted a disappointing gain of 12,500 jobs, though all of that was driven by full-time employment. The surprise was that Canada had massively eased COVID-19 restrictions (chart 4) and so many—including me—had thought that the month would have seen an acceleration of job growth on a return-to-work effect particularly in the sectors most affected by the restrictions. Not. Whoops.

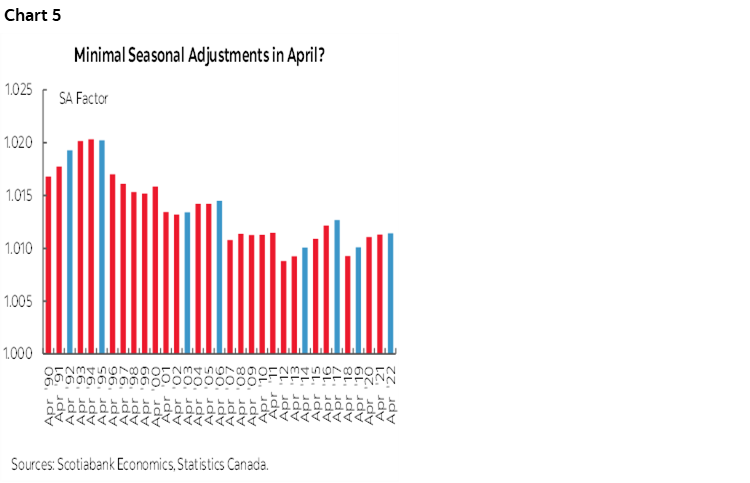

Why not? One theory was that a sick Easter Bunny stomped muddy footprints all over the report as argued at the time (here). The Easter Bunny enters the picture because the Good Friday holiday shifts around every year in relation to the Labour Force Survey’s reference week which is (usually) the week including the 15th of each month. Seasonal adjustment factors might not have adequately controlled for this as evidenced by the fact that the SA factor didn’t really change in April of this year (chart 5).

Why sick? Well, because many people were indeed sick in April. Parsing through the figures from the Ontario Science Table (here) shows that the month of May appeared to see significant improvements in cases (although most definitely undercounted by a lot) but also in hospitalizations, patients in ICUs and wastewater testing results. All of this suggests that the massive drop in hours worked that fell 20.7% m/m at an annualized rate and the soft jobs headline may have been at least partly caused by sickness and Easter.

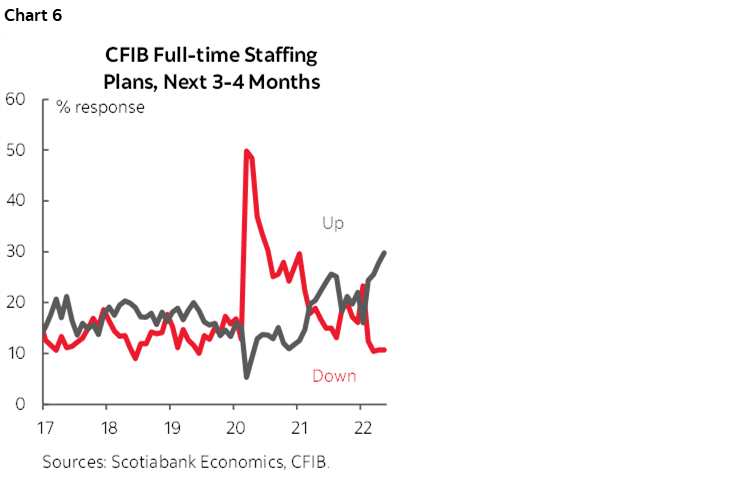

With both in the rear view mirror, this might be the report that bears the fruit of the liberalization of those restrictions and the positive impact upon high-contact service sectors in particular. Weather effects on some of those seasonal categories may also be mixed. Nevertheless, key small businesses continue to indicate aggressive hiring plans (chart 6).

At least as important as the jobs tally may be wages. They’ve stalled in Canada. After rising at a pace of between about 6–9% in m/m seasonally adjusted terms at an annualized rate from July 2021 until January 2022, this figure then fell 4.1% in February, another 1% in March and fell a further 3% in March. I’m not entirely sure of why in terms of the balance of labour tightness, omicron and compositional effects and other considerations, but it’s the way to look at wages in Canada as opposed to the year-over-year rate for evidence of wage pressures at the margin.

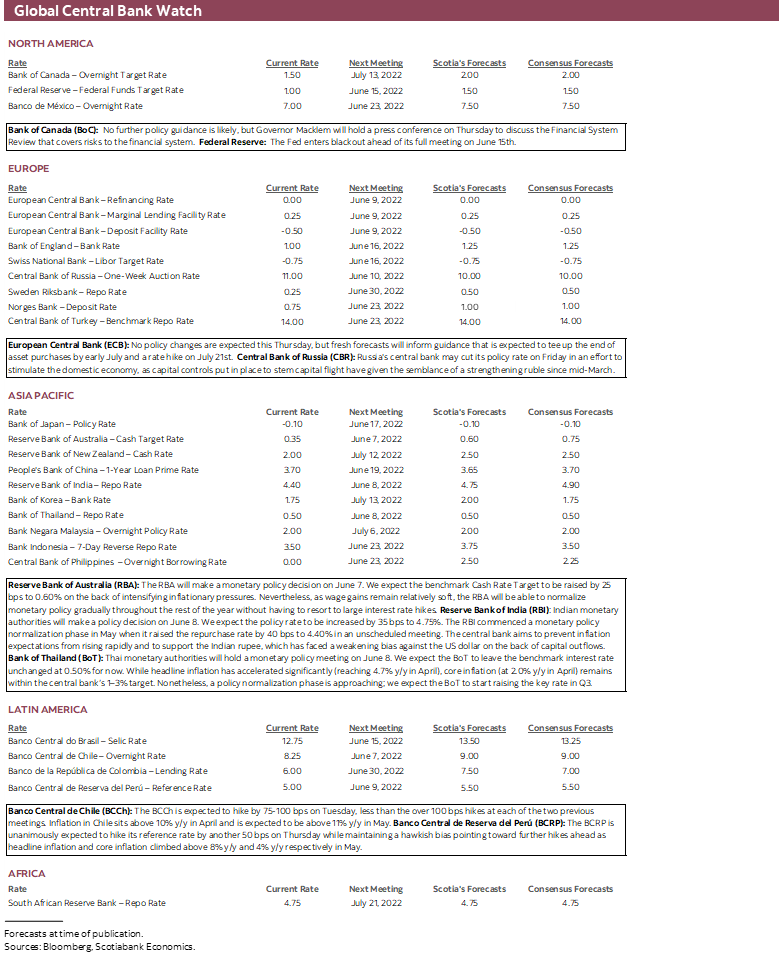

ECB TO HEADLINE GLOBAL CENTRAL BANKS

Seven central banks that we follow will offer policy decisions while the Federal Reserve slips into communications blackout ahead of its meeting the following week and Bank of Canada Governor Macklem makes an appearance.

European Central Bank (Thursday): The other central banks that follow below will be the opening acts for the ECB that will headline this week’s central bank line-up. This full meeting includes a statement (7:45amET), President Lagarde’s press conference 45 minutes later and refreshed quarterly macroeconomic projections. It’s widely expected to tee up the end to net purchases under the Asset Purchase Program in early July and set the scene for the first rate hike of the cycle that is likely to be delivered on July 21st. That would generally be consistent with Lagarde’s guidance that was provided on May 11th when she said:

“The first rate hike, informed by the ECB’s forward guidance on the interest rates, will take place some time after the end of net asset purchases. We have not yet precisely defined the notion of ‘some time,’ but I have been very clear that this could mean a period of only a few weeks.”

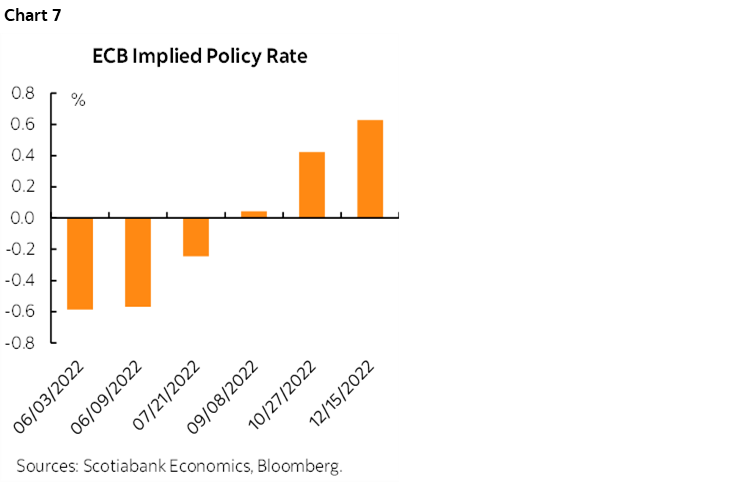

Global financial markets will be particularly attuned to whether Lagarde offers guidance toward a gradual initial pace of lift-off defined as a quarter point hike, or a half percentage point hike as some of her colleagues prefer. Markets lean more toward the quarter-point scenario with the deposit facility rate expected to rise by 125–150bps by year-end into early 2023 (chart 7). Inflation that is running at over 8% y/y with core at just under half that would lend itself to a quickened pace of lessening massive monetary policy stimulus.

Reserve Bank of Australia (Tuesday): Economists think the RBA could hike by between 0.25% and 0.5% and markets have just over a quarter point hike priced in futures contracts. When it first hiked on May 3rd, the RBA guided that further rate hikes will be required to achieve its over 2% inflation target that climbed to 5.1% y/y in Q1. Since then, Australia has seen a mild acceleration of wage growth to 2.4% y/y and 0.7% q/q non-annualized, a soft employment report of +4k with a large full-time gain offset by a part-time loss, and strong Q1 GDP growth and retail sales in April. The RBA has already ended QE purchases of Australian bonds (January), chosen to end reinvestment of maturing bonds (May) and provided explicit guidance that it views outright bond sales as only a remote possibility.

Reserve Bank of India (Wednesday): This one’s in a sudden rush. Another 50bps hike is expected for the RBI’s repurchase rate. This follows the unscheduled emergency rate hike of 40bps on May 4th. Inflation is running at just under 8% y/y with core climbing to over 7% y/y in April.

Chile’s central bank (Tuesday): They are expected to hike by 75–100bps. Believe it or not, that’s actually a cooler pace if delivered compared to the over 100bps hikes at each of the two previous meetings. Like everywhere else, the central bank is chasing inflation that crossed above 10% y/y in April with the next day’s report for May expected to cross above 11%.

Bank of Thailand (Wednesday): Most expect the BoT to hold its benchmark rate unchanged at 0.5% on Wednesday. It has not hiked once yet during the pandemic as growth concerns in an economy hit particularly hard by COVID’s effects on tourism have dominated. Still, Monday’s inflation figures are going to apply further heat at least in terms of guidance when headline inflation likely climbs to just under 6% y/y and core inflation is expected to rise above 2% y/y compared to the central bank’s 2% headline target in a 1–3% range.

Peru’s central bank (Thursday): Is unanimously expected to hike its reference rate by another 50bps while maintaining a hawkish bias pointing toward further hikes ahead. Inflation climbed to 8.1% y/y in May with core CPI crossing above 4% at 4.2% y/y.

Bank of Canada Governor Tiff Macklem will speak on Thursday alongside Senior Deputy Governor Rogers, but only to present the bank’s Financial System Review. There will be a press conference at 11amET that day. The Governor has usually deflected questions on monetary policy at this event. That probably means we won’t get any further insight into the BoC’s policy bias than was presented at its most recent statement (recap here) and Deputy Governor Beaudry’s speech (here) and press conference. The broad takeaway from those communications was the statement-codification of the BoC’s willingness to hike “forcefully” and this time strengthening the urgency by adding “more” in front of it alongside removing reference to “timing” that makes it only about pace. Coupled with Beaudry’s comments in what I thought was one of the better speeches and appearances of late, the overall message is that the BoC could be leaning toward both a bigger-than-50 move in July and a terminal rate of at least 3%.

Russia’s central bank (Friday): In last place and rather deservedly so I’d say, Russia’s central bank may cut its policy rate again on Friday. Capital controls have stemmed capital flight and accordingly created the mirage of ruble strength as the currency has appreciated by over 120% since its bottom on March 7th. Stemming the currency’s freefall has given the ability to cut the policy rate in an effort to stimulate the domestic economy as imported inflation risk ebbs, but not without the usual costs associated with capital controls.

MACRO REPORTS—INFLATION OVERLOAD!

The main focus across other global indicators will be a batch of CPI releases from Asian and Latin American economies of which only one may impact global market sentiment versus regional market effects for the others.

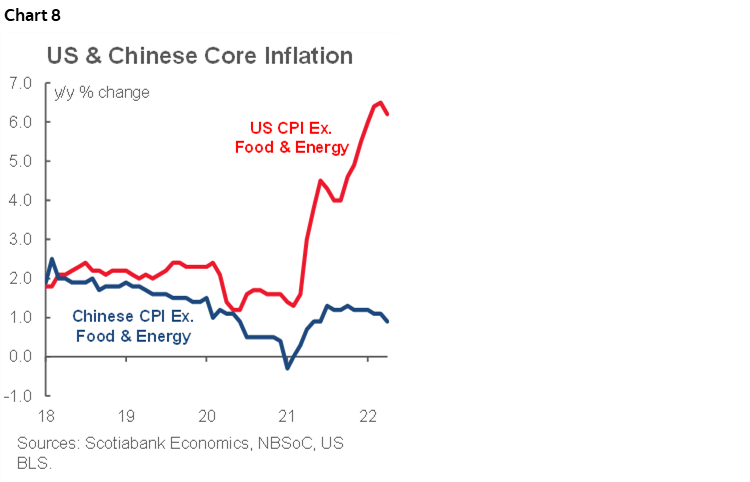

China’s CPI print for May is expected to witness marginally greater upward pressure on Thursday evening (eastern time as always). The kind of pressures driving inflation in China are the sort that the People’s Bank of China should be looking through in favour of an easing bias. Headline inflation might tick up to about 2¼% derived significantly from higher oil prices, but core inflation has been falling from 1.3% last October at a pandemic-era peak to just under 1% now in a stark contrast to the US that explains relatively central bank policy divergence and pressures on the yuan (chart 8). If higher energy prices continue to crowd out incomes with no offsetting benefits in an economy that is a large net importer of energy, then further disinflationary pressures to core inflation may lie in the cards.

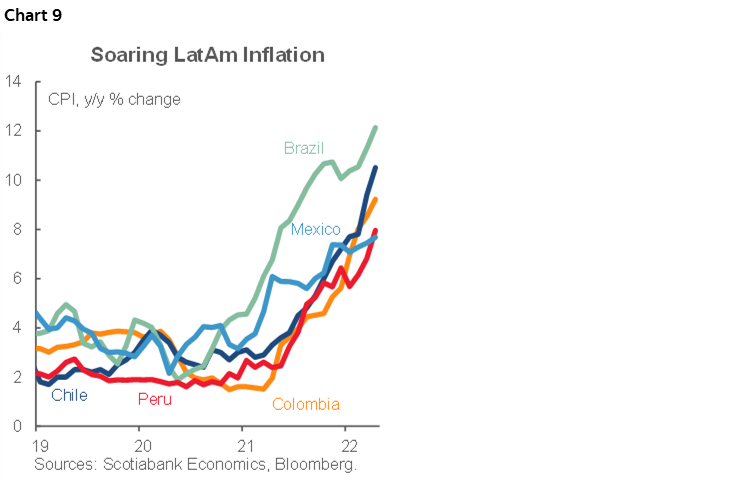

Latin American markets are expected to see little if any relief from inflationary pressures (chart 9).

- Colombian inflation may rise a little more slowly at under 1% m/m which could bring slight relief to the 9.2% y/y rate which is the highest since 2000 with core inflation at 5.9% and its highest since 2016.

- Chilean CPI inflation is forecast to remain hot at over 1% m/m which would drive the year-over-year rate over 11% for the highest rate since 1994.

- Mexico’s CPI figure for May is expected to rise at a muted pace on Thursday which could flatten the year-over-year rate around 7.6% and based upon what can be observed from bi-weekly figures into the first half of the month. Bi-weekly core inflation is still relatively persistent.

- Brazil updates inflation for May on the same day and the month-over-month rise is expected to ebb but remain hot enough to keep headline inflation around 12% y/y which is the hottest since 2003.

Three other Asian economies are expected to see further jumps in inflation including Thailand (Sunday) where inflation is forecast to approach 6% y/y, Philippines (Monday) that will cross north of 5% y/y and Taiwan (Tuesday) that is expected to hold around 3.4% y/y.

Other US releases will be light including a trade deficit that should narrow as the already known narrowing in the merchandise deficit is added to the usually fairly stable services balance (Tuesday), and UofM consumer sentiment for June (Friday) that is guessed to be little changed as strong jobs and high gas prices are among the competing effects.

Canada updates trade for April on Monday which will hopefully begin turning around the quarterly export picture, as well as the Ivey PMI figure for May that our econometricians use as an input into modelling CPI (here).

Across Europe, nothing will hold a candle to the ECB, but limited data may catch a glance or two. German factory orders (Monday) and industrial output (Wednesday), Spanish (Monday) and Italian industrial output (Friday), and French payrolls wayyyy back in Q1 (Thursday) are due out. Norway’s inflation rate is expected to pull off a bit in May’s reading (Friday) when prices are expected to marginally dip in month-ago terms while underlying inflation crosses above 3% y/y. Either way, Norges Bank has made it clear through forward guidance that it intends to hike again on June 23rd.

China will also update the private composite PMI for May into the Monday open which is expected to post a slower pace of contraction as per the already released state versions. China might also update financing figures either this week or next, and will update trade figures around mid-week for May.

Finally, the OECD will update its Economic Outlook on Wednesday. Its forecasts are usually a lagging indicator of ground already covered by private consensus forecasters, but often catches market attention nonetheless.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.