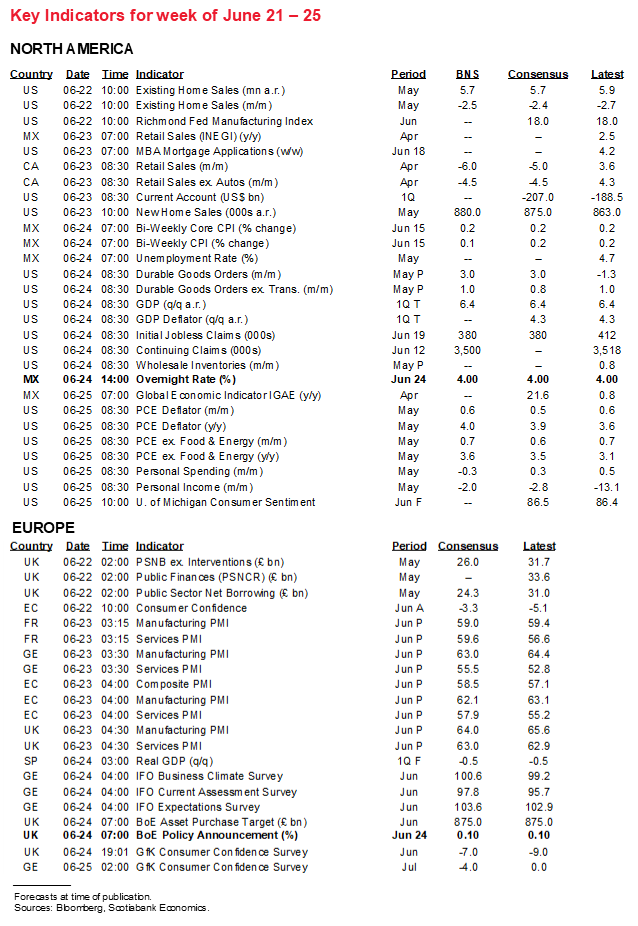

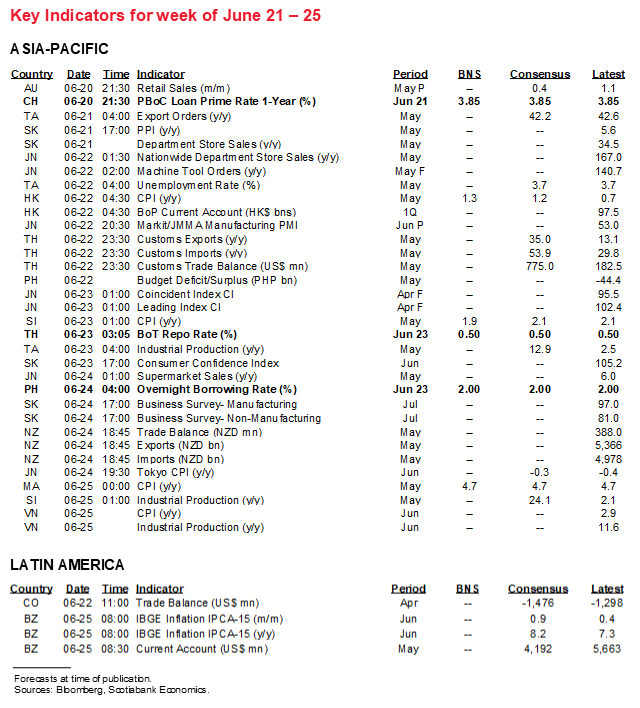

Next Week's Risk Dashboard

• The Fed’s reaction to the markets

• What’s driving bond markets redux

• Fed’s stress tests

• CBs: BoE, Banxico, PBOC, BoT, BSP

• PMIs: EZ, UK, US (Markit), Japan, Australia

• US PCE, consumers, housing, investment

• Canadian retail sales

Chart of the Week

THE FED IS NOT SO STRESSED ABOUT US BANKS

The Federal Reserve Board will release the results of annual stress tests on the US banking system on Thursday at 4:30pmET. They especially matter because the Board announced on March 25th (here) that banks that pass the stress test will have restrictions on dividend policy and share buybacks lifted after June 30th.

The Fed has said that the restrictions will end “for most firms” after June 30th. Vice Chair Quarles said on June 1st that the stress tests are showcasing a “very resilient” banking system. This would suggest there is low risk of any disappointment. Any individual banks that fail the stress test will remain subject to the restrictions through Sept 30th and, if they fail again at that time, then even tighter distribution limitations will be imposed. Total risk-based capital positions at banks have improved since the initial shock of the pandemic (chart 1). The FDIC’s overall assessment of the sector is summarized here until the next round of Q2 reports. The next phase will involve communications from across individual banks on capital management plans when the Q2 US bank earnings season begins on July 9th.

Stress tests apply to banks with more than US$100B in total consolidated assets and they are designed to ensure that there will remain adequate capital to absorb losses in a severe recession. All firms participated last year but smaller banks only need to participate every other year. Out of 33 eligible banks, 23 large banks have been stress tested including 19 mandatory banks and four firms that opted in (three of which are Canadian) out of 14 that could have.

The stress test involves a hypothetical global recession that began in 2021Q1 with strains in commercial real estate and corporate debt markets, plus firms with significant trading operations will be tested against the default of their largest counterparty. The scenarios are outlined here.

CENTRAL BANKS—THE FED RIPPLE

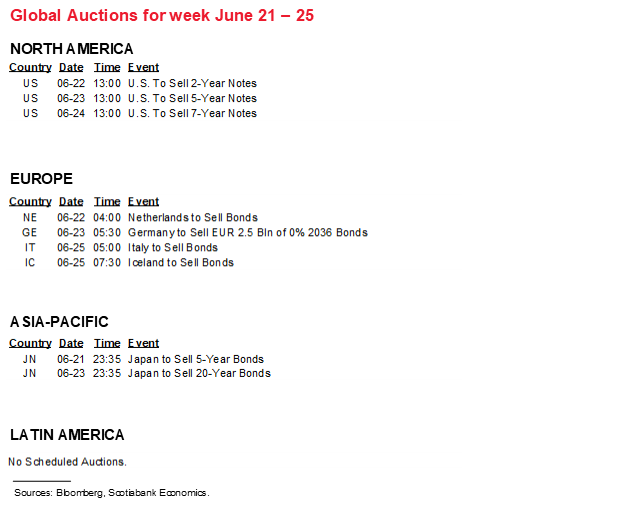

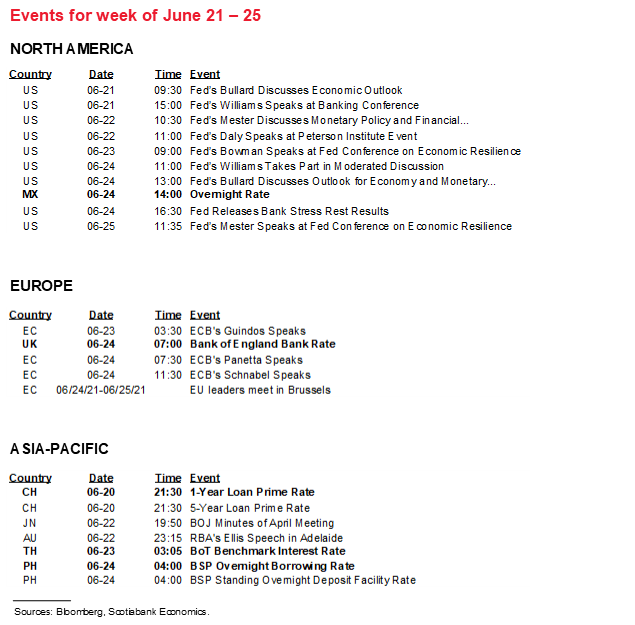

Fivw central banks will weigh in with policy decisions over the coming week, with most of the attention placed upon two of them. There will also be a heavy line-up of Fed-speak. I’ll focus comments on the BoE, Banxico and the Fed. Central banks in the Philippines (Thursday) and Thailand (Friday) are not expected to alter policy and the People’s Bank of China is widely expected to keep its Loan Prime Rates unchanged at the start of the week.

Bank of England—Debating Lift-Off

No material policy shifts are likely at this meeting. The prior round of communications on May 6th offered the more significant shift. Recall that the MPC decided to reduce the flow of gilts purchases to £3.4B/week while leaving the size of the gilt purchase program unchanged at £875B so that they could stick to prior guidance that they will keep buying until the end of 2021. They could have left the flow unchanged but that would have exhausted the size of the facility a few weeks beforehand. There is likely to be only one hawkish dissenter who will continue to prefer to reduce the purchase program, but Chief Economist Andy Haldane will dissent for the last time before leaving.

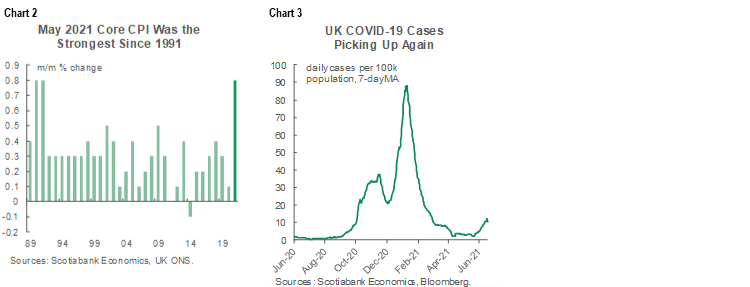

The May meeting also revised forecasts higher and indicated they expect slack to be eliminated by 2022-Q2 with no material change in the output gap thereafter. When questioned on this, Governor Bailey said the forecast for excess demand was “definitively temporary” as the effects of fiscal policy offer a temporary boost and because the BoE lowered its estimates of the scarring effects of the pandemic on the supply side. While he noted that there was high uncertainty around this forecast, developments over recent weeks are unlikely to have materially altered that stance. Also recall that Inflation was revised higher to 2½% this year and slightly softer at 2% next year. Since then, inflation has surprised higher with core CPI spiking to 2% (1.3% prior) and 0.8% m/m for the strongest gain in a month of May in decades (chart 2). The BoE has nevertheless done a better job at forecasting inflation so far than either the Fed or the BoC as the chart of the week on the front cover demonstrates. Regardless, the lifting of COVID-19 restrictions has been postponed by at least a month due to the rise of the Delta COVID-19 variant (chart 3). It’s unlikely the BoE will feel comfortable enough to rock the boat further at this meeting.

It’s unclear that the BoE would view it as being worthwhile to offer further adjustments to the stock and flow of its gilts purchase program given its expiration by year-end anyway. The more meaningful debate concerns when the policy rate may begin to lift off. Markets are sensibly pricing rate hikes into Q2 of next year which roughly coincides with the BoE’s forecast for spare capacity to shut (chart 4). It’s unlikely that there will be much if any attention placed upon spillover effects of the Fed policy shift, particularly since the BoE is already scheduled to end bond purchases perhaps even before the Fed begins to dial them back, while markets are pricing BoE hikes well ahead of the Fed.

Banxico—Watching Inflation

Governor Herrera. Well, not quite yet, but former Finance Minister Arturo Herrera becomes Governor in December when current Governor Diaz de Leon steps down. That could offer an interesting transition point for the central bank. The December meeting will be on the cusp of when Scotia’s Eduardo Suarez, based in Mexico City, thinks the central bank will begin to raise its policy rate in 2022-Q1. Also bear in mind that current inflation readings are surprising higher. The catch is that Herrera is a dove and has already signalled that he sees no need to rush toward raising the policy rate. That’s probably sensible for now, but we’ll see as the year progresses.

For now, Thursday’s communications are unlikely to offer any material shifts. Inflation is running at 5.9% y/y with core accelerating to 4.4% and hence well above the 3% +/-1% target range (chart 5). Banxico forecasts inflation to remain above the target until early 2022. Signs of greater-than-expected pressures and persistence could alter this stance at subsequent meetings. One risk to monitor is the impact of the Fed shift on imported inflation given the peso’s extra 3%+ post-Fed depreciation to the USD and 5%+ since the prior week.

Fed-Speak

Several Fed officials will take to the virtual podium. Post-FOMC comments from individual members will be watched for possibly further clues on how many members wish to discuss tapering now and potential timelines for doing so. Fed Chair Powell delivers testimony before the Select Subcommittee on the Coronavirus Crisis of the US House of Representatives on Tuesday at 2pmET. His topic will be the Fed’s response to the pandemic. There is likely low risk to his testimony especially after his performance this past week.

Fed-speak will also bring out St. Louis President Bullard and NY Fed President Williams (Monday), Cleveland’s Mester and San Fran’s Daly (Tuesday), Governor Bowman on community development, Atlanta’s Bostic and Boston’s Rosengren (Wednesday), Bostic again with Philly’s Harker, Williams and Bullard (Thursday), and once again Mester and Rosengren (Friday).

WHAT’S DRIVING BONDS?

With so many Fed speakers on tap it might be useful to hear them share their thoughts on bond market developments. Are they surprised by the magnitude of curve flattening in Treasuries since the FOMC communications? If they indicate surprise, then could it impact their views on appropriate policy stances going forward since market signals provided by deep and liquid markets could offer information to consider? After both 2s and 10s initially cheapened following the full suite of communications, the Treasury curve flattened with the 2 year yield ending the week about 10–11bps higher and the 10 year yield ending about 3bps lower compared to before the Fed communications.

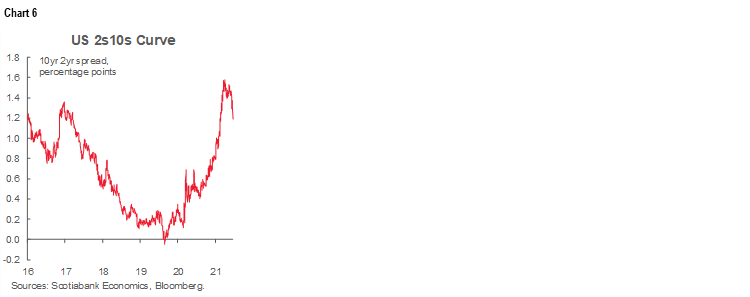

This is an important issue not least because we all know the dismal evidence on how Treasury curve flattening can portend challenges ahead. If curves are flattening because the market perceives the Fed to be committing a policy error with trouble ahead, then that’s obviously not a good sign. Such a risk signal seems to be pretty low so far given that the 2s10s curve remains fairly steep (chart 6) and models based on the Treasury curve’s slope indicate low risk of such trouble ahead (here). An awful lot would have to go horribly wrong against the narrative of a vaccine- and stimulus-fed recovery in order for trouble to lurk within a reasonable time frame.

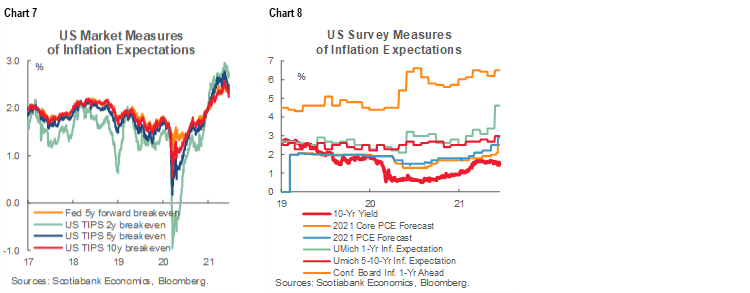

If curves are instead flattening because markets think the Fed won’t quite let inflation run as hot as previously thought, then that might offer more of a mixed signal. It might be resetting inflation expectations at a modestly lower level and, once reset, market positioning could then turn more neutral. So far, it seems that market-based and survey-based measures of inflation expectations continue to indicate that markets believe in the reflation trade relative to the Fed’s guidance it plans to modestly overshoot 2% for some time (charts 7–8). Or it could be driving a very crowded repositioning away from reflation trades in commodities and inflation product that may be undershooting the ultimate resting point. Alternatively, there may be another explanation.

From what I’ve gathered, it seems that the bandwagon consensus narrative in the markets right now is that inflation is already on its way out, the Fed’s going to prematurely snuff out the recovery and that growth will disappoint. Good luck with all of that.

On the Fed (recap here), since when do two hikes three years from now expressed in dots of dubious merit that most of us had already anticipated anyway result in prematurely snuffing out a recovery that is expected to shut spare capacity this year? Even by the end of 2023 the FOMC is saying they’d still expect to be running 175bps below what they say is the nominal R* measure. Even the most hawkish among FOMC officials—all two out of 18 of them—think that by the end of 2023 the policy rate range will be 1.5–1.75%. The most hawkish among FOMC officials appears to be St. Louis Fed President James Bullard and, while I have a bias toward his arguments, his caution that the Fed could raise rates later in 2022 is a minority view at present and still probably leaves the Fed trailing developments. Snuff out? You’ve gotta be kidding me. We don’t have anything close to that kind of information on our hands at this point. The Fed is more likely to be years behind and will get further and further behind. Flatteners don’t usually arrive this early ahead of the first hypothetical hike in the dots that Fed Chair Powell dismissed as requiring a “mountain of salt” to take literally.

Also on the Fed, while they are talking about it in greater numbers than “a number” who raised it at the previous meeting, they are still saying ‘substantial further progress’ has not yet been achieved to merit tapering. Data flow over “coming meetings” doesn’t say one meeting (July) so strong signals just yet are likely premature. The FOMC is likely to want several months of payrolls and inflation data in order to shift gears meaningfully. Maybe ‘coming meetings’ was actually a dovish taper signal to those among us who thought it possible that Powell could drop the taper bomb at the late August Jackson Hole symposium or at the September FOMC. To go from $120B to zero and then presumably reinvest for a while before hiking is still going to take a while. In the meantime, there are hundreds of billions more Treasury purchases forthcoming into the period in which the debt ceiling is going to be reinstated that, in my opinion, is excessive central bank buying.

On inflation, it’s premature to price in a return to very low numbers in my view (US CPI recap here, and the Canadian CPI recap takes a similar approach here). Be wary of the cherry-pickers who choose to emphasize data that fits their thesis that it’s all just transitory because of upsides like gas and autos, while ignoring potential transitory downsides that could heat up as the economy reopens—like broad services price inflation that hasn’t even begun in earnest. Or clothing, because the workforce will be wearing threadbare pyjamas to work from home years from now... Or food and medical care price inflation that is flat now compared to high year-ago base effects but likely isn’t busting up a multi-decade trend of rising pressures. Further, secular forces that held inflation back in the past pre-pandemic decade may well not be the same disinflationary forces going forward even if we didn’t have history-busting monetary and fiscal policy stimulus that is expected to persist on top of it all. When was the last time the Fed blew up its balance sheet and sat on zero for years while fiscal policy joined in and all in response to a transitory shock solved by science? #never. In any event, inflation risk is to be judged over the full cycle ahead and not just the past few months, or the next six months.

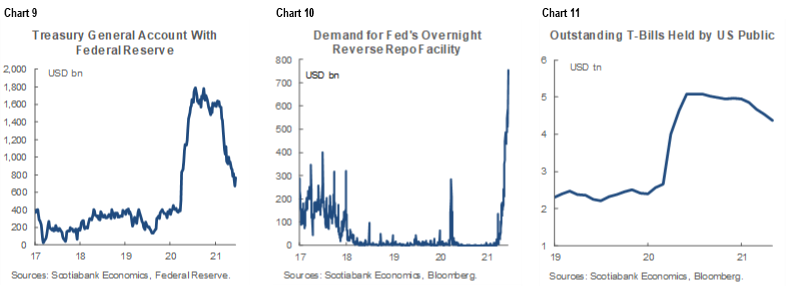

Scarcity and liquidity may still be the more likely explanations for Treasury curve flattening. The debt ceiling reinstatement on August 1st is messing up the markets and will for a while yet. The policy-induced flows in and out of bond markets are more important than inflation views in driving yields. Since about mid-February, the Treasury General Account has dropped by ~US$865B (chart 9) while the Fed’s o/n repo facility has drained about $750B (chart 10). Bills outstanding have dropped by about $600B over a similar time frame (chart 11). The Fed has bought hundreds of billions of more Treasuries over that same period and is fanning relative scarcity pressures. That’s a lot of money on net that has to go somewhere else and that drives reach for yield pressure.

Overall, I’m personally uncertain regarding the overall blend of bond market drivers and it may be that we’ll have to wait until the forces over coming weeks before the August 1st debt ceiling reinstatement subside before we can judge the durability of these flows and what’s causing them. Maybe by then we’ll be getting closer to tapering. At that point, it could still dawn upon markets that the Fed’s first action is more likely to offer much less support to bond markets. If the Dems move to raise the debt ceiling and wrap it in a stimulus package that can get past Congress, then less buying and more issuance could well drive renewed curve steepening.

INDICATORS—PMIS TO INFORM MOMENTUM

Regional growth variations will be further informed by the latest monthly batch of purchasing managers’ indices for the month of June. The measures reflect what global purchasing managers in the manufacturing and service sectors are seeing and expect for new orders, current sales and production, price pressures, hiring intentions, and supply chain readings on backlogs and inventories.

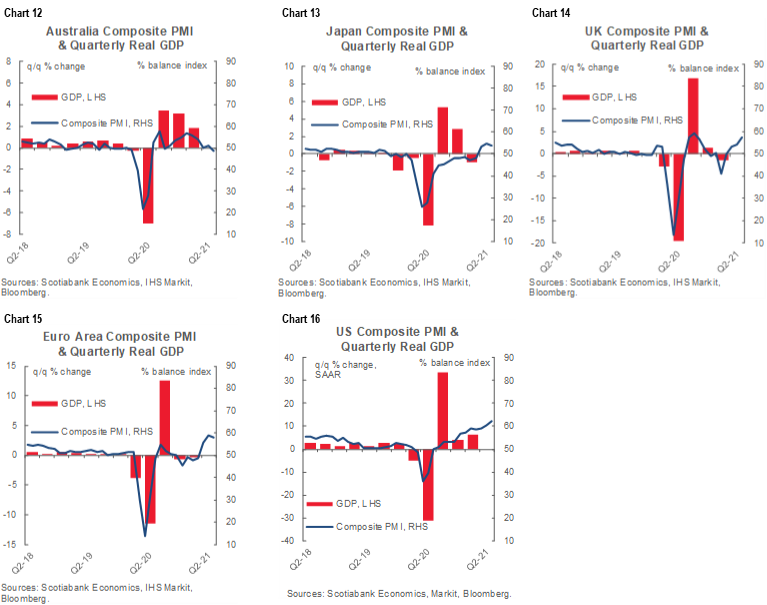

Japan and Australia kick it off with their readings on Tuesday followed by Eurozone and UK PMIs on Wednesday. The US will also consider updates of the Markit PMIs on Wednesday but the more widely followed ISM gauges will follow in early July. See charts 12–16 for depictions of the trends in these readings and how the strongest growth signals are coming from the UK and US.

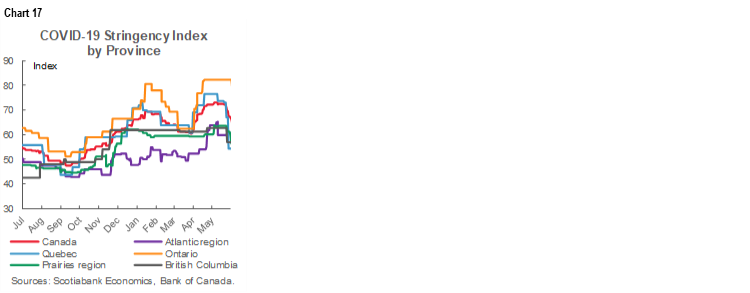

Canada updates April retail sales on Wednesday as the lone development of the week. There are two things to watch. First, we already have ‘flash’ guidance based upon 46% of companies surveyed that sales fell by 5.1% m/m. Since that is only about half of the typical full survey response rate there could be revisions. At the same time, however, we should get preliminary ‘flash’ guidance for May which is also likely to be on the soft side. Much of Canada remained in lockdown through April and May. Markets are likely to look past the figures with eyes on timing the potential magnitude of a rebound that could start as soon as June if readings on restrictions and mobility are a guide (chart 17).

The main US releases arrive on Friday when the Fed’s preferred inflation gauge plus income and consumer spending during May will be released. Incomes probably fell by about 2% m/m in May because even though stimulus cheques continued to be disbursed, the pace at which they are being distributed even in June has been markedly slowing compared to the initial burst. Consumer spending could slip given the already known decline in retail sales that now represent just under half of total consumer spending; if services rebound more rapidly, then that could spare a decline in total spending.

Other US releases will include home resales during May (Tuesday) that are expected to dip given the trend in pending home sales, new home sales for the same month that could bounce back from the prior decline, May durable goods orders that are expected to recover from the prior month’s weakness, and the final estimate for Q1 GDP that is expected to be unchanged around 6.4%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.