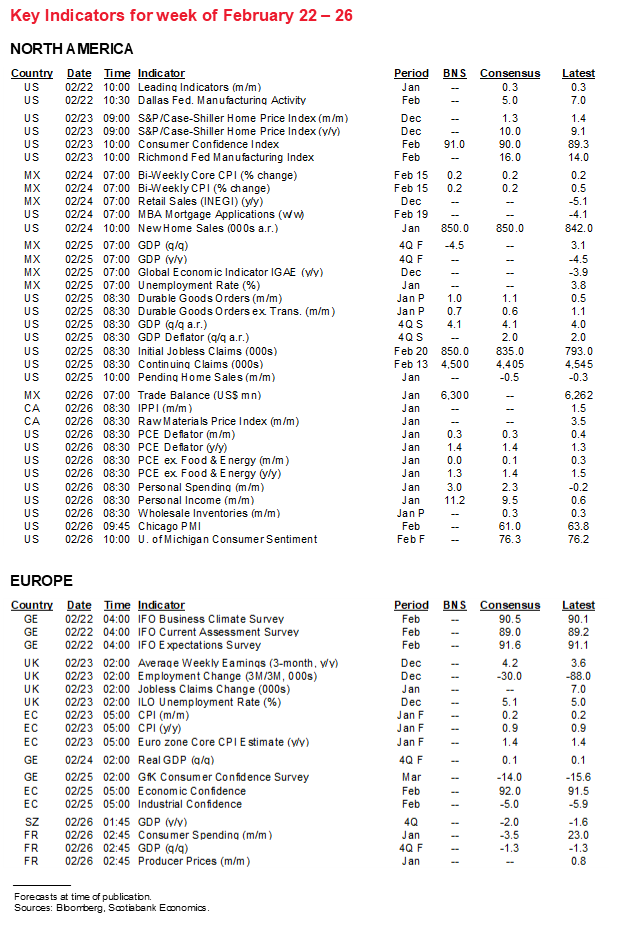

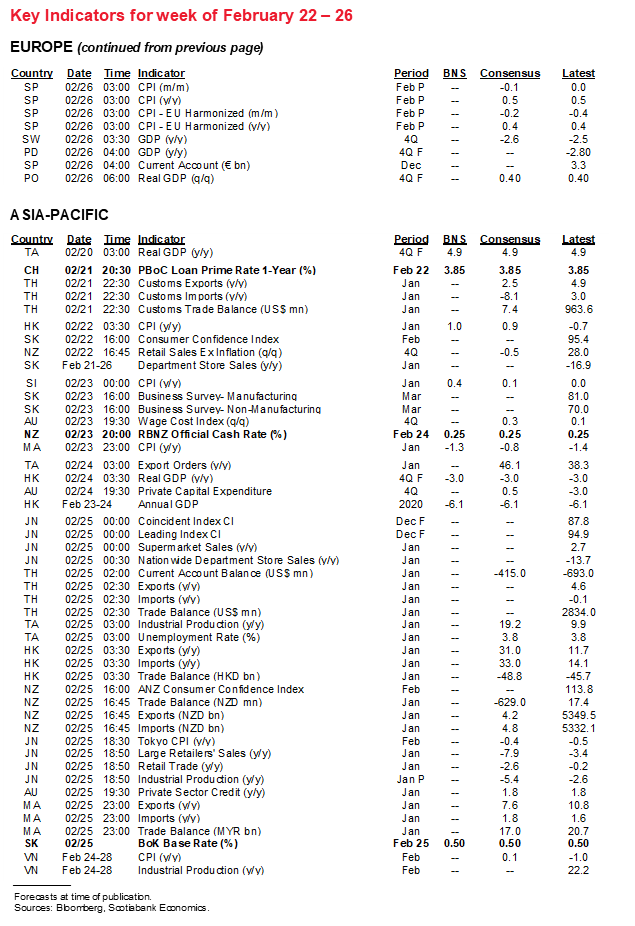

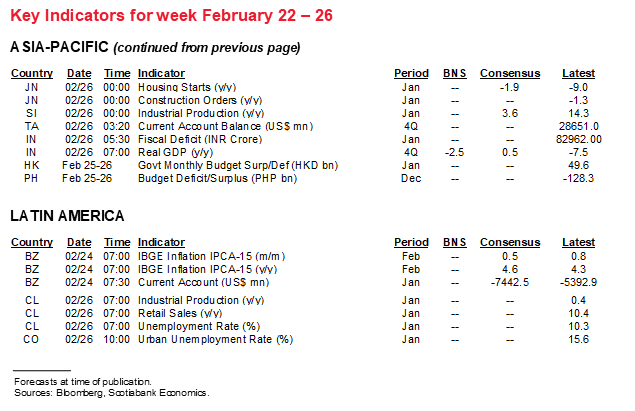

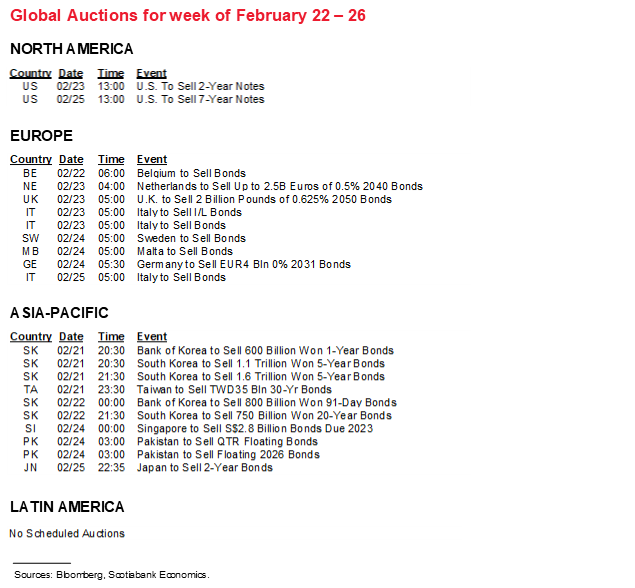

Next Week's Risk Dashboard

• US consumers & the Fed

• Fed’s Powell

• BoC’s Macklem

• ECB’s Lagarde

• G20 finmins & CB heads

• CBs: PBOC, RBNZ, BoK

• CDN bank earnings

• Alberta budget

• Global releases

Chart of the Week

1. US CONSUMERS & THE FED

When January’s figures for consumer incomes and spending roll around on Friday, they will further accelerate the debate over the outlook for US consumers and important related matters. That outlook likely puts upside risk to our near-term forecasts for US growth and potential spillover effects abroad and perhaps over time it could prove to be of such an order of magnitude as to bring forward the risk of a Federal Reserve hiking cycle.

Stimulus-fed income growth and how behaviour adapts as vaccines are deployed will be the main catalysts. I figure that personal incomes likely grew by just over 11% m/m at a non-annualized seasonally adjusted rate in January. That’s based on US$166 billion in transfers from government to households to fund stimulus cheques of US$600 per person that were deposited starting around mid-January plus an extra US$300/week for just under 10 million unemployed Americans, as well as reasonable assumptions on other income components.

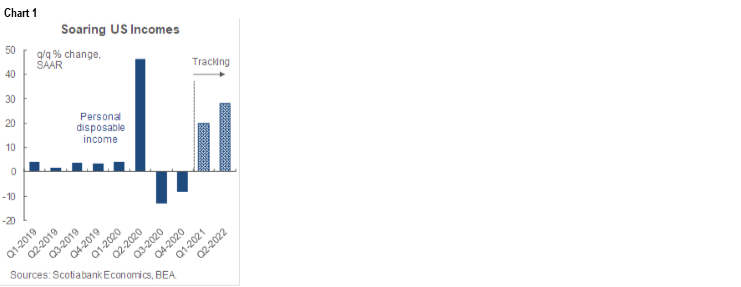

It doesn’t stop at that. If the Biden Administration’s plan for US$1,400 cheques per person at a cost of US$465 billion goes through, then that would equate to another annualized US$5.6 trillion lift to personal incomes in April assuming March passage. The effects on annualized income growth are shown in chart 1. Even if the cost of the cheques turns out to be smaller through stricter means-testing then we’re still likely looking at back-to-back annualized quarterly income gains of 20% or more in each of the first two quarters of this year. The second quarter of last year saw faster income growth in percentage terms at double such a rate, but only for one quarter; we’ve never seen back-to-back quarters for income growth of this magnitude in the history of the figures at least back to the 1940s.

In monitoring progress toward passing such stimulus, note that the House of Representatives is expected to take up a version of the bill next week which will begin the process of securing approval in both chambers of Congress including the ultimate horse trading before a bill lands on the President’s desk. Passage sometime in March with cheques going out in April is likely and probably through reliance on the go-it-alone budget reconciliation route. Then the debate may shift toward using this option a second allowed time for an infrastructure bill that would heap on further stimulus.

The first-round effect of stimulus injections of this magnitude is to spend a little and save a lot. We know the retail sales control group went up by about 6% m/m last month which is likely to drive about 3–3.5% growth in total consumer spending in Friday’s figures for January. The net effect would likely see the personal saving rate soar to around 24%, or a level not seen since last May. As stimulus works through, we’re likely to see substantial consumption gains over 2021H1 with an elevated saving rate throughout the period that should gradually decline as precautionary saving motives diminish. Some of this may be put toward balance sheet repair. As the overall process unfolds, we’re likely to witness sustained strong consumption gains into the second half of this year.

What this could do is to put upward pressure upon consensus estimates for GDP and consumption growth right off the bat to start 2021 given Bloomberg’s consensus anticipates growth in both measures at an annualized pace of just 2–3% during 2021Q1. It’s not clear one should go as high as the Atlanta Fed’s ‘nowcast’ that is tracking 9½% annualized Q1 GDP growth before we get much data to put in the sausage grinder, but it’s feasible.

In addition to this massive positive income shock is the fact that consumers are sitting on top of a heavy overhang of accumulated extra cumulative savings (chart 2). Liquid deposits and cash balances have increased by US$4 trillion since last February. There is an element of a liquidity trap along with balance sheet repair that may restrain at least some of this overshoot from going back into the system, but if there is one thing I’ve learned it is never to underestimate US consumers’ spending capacity.

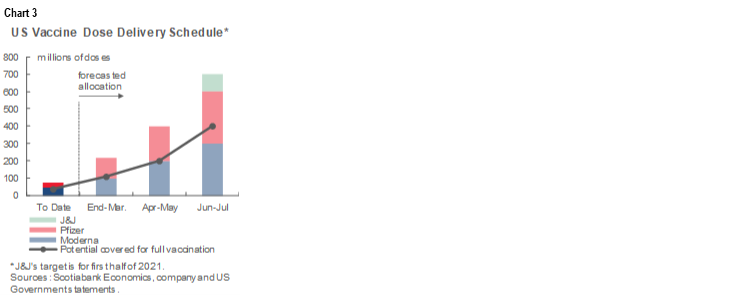

There is, however, the old adage about leading a horse to water. Will consumers re-engage in the economy and spend this manna from heaven (or from Joe, to be more accurate)? Vaccine progress is important in this regard. Chart 3 shows vaccine deliveries to the US by Pfizer and Moderna and indicates that, at two doses per person, the US will have enough doses to vaccinate pretty much all of its population by July. If evidence that Pfizer’s shot may not require two doses reduces the requirement then this could effectively happen sooner, plus there are still Johnson and Johnson’s plans to deliver 100 million vaccinations at a one-dose requirement by mid-year pending potential approval over coming weeks.

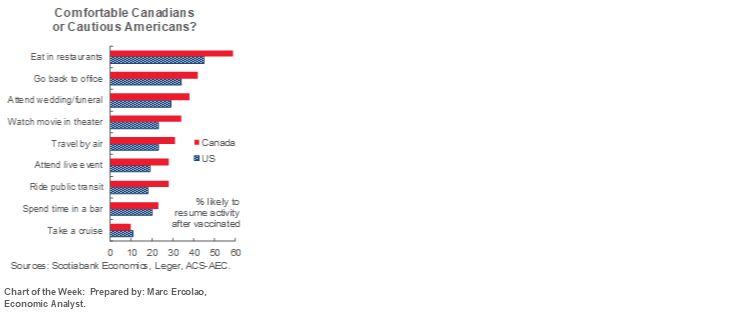

Once vaccinated, then what?...assuming the vaccines remain significantly effective against variants. See Marc Ercolao’s helpful cover chart on page 1 of the Global Week Ahead which suggests that many people will re-engage in pandemic-affected activities. The chart shows survey responses to the question of whether people will return to pandemic-affected activities after they have been vaccinated. Between 20–50% of respondents in both the US and Canada say they will do so across most activities. The debate on whether people return to pre-pandemic activities is likely too binary in nature, with polarized assumptions on how nobody will, or everyone will. The truth is likely somewhere in the middle and 20–50% response rates are significant at the margin which is what matters to predicting growth in consumption and the overall economy. It’s feasible that these response rates could build with confidence. Also note that perhaps somewhat curiously there are more Canadians than Americans indicating willingness to return to such activities; perhaps that reflects a much lower per capita cumulative COVID-19 case count north of the border.

In addition to the question of whether consumers will re-engage in pre-pandemic activities and over what time period is what they might do with their bounty instead. There will likely be high reticence to engage in many pandemic activities for a substantial number of folks for some time yet. Each cycle, however, drives changes in the composition of consumption and this cycle is likely to be no different. Instead of spending on monthly transit passes, cruise tickets or airfare, and sporting or concert tickets, consumers are likely to spend on other things and likely with a bit of a nesting focus around the home digs. Remember, it wasn’t that long ago that alongside strained housing affordability folks started to willingly spend thousands on fancy phones, iPads and laptops. Speaking of which, where’d my phone go….

All of which brings us on the long Charlie Brown route back home to what it all means for the Federal Reserve. Could Larry Summers be correct in warning that fiscal stimulus will overheat the economy and bring the Fed to hike as early as late-2022? It’s not our base case at this point, but I wouldn’t rule it out by any means. If Okun’s ‘law’ between stimulus-fed consumption and GDP growth boosts employment on the back of such stimulus and organic drivers take over to propel employment and consumption in a post-vaccine world, then we could be at full employment much sooner than the Fed thinks. Ditto for inflation as the inventory cycle struggles to keep up with a potential consumption boom (hint: order early ahead of Spring…).

To then hike as soon as the end of next year would probably require the Fed to deviate from the 2013–15 playbook specifically with respect to reinvestment. My reading of Fed communications has not seen anything on reinvestment plans whereas they’ve just indicated in the meeting minutes and speeches that the 2013–14 taper experience is a likely model for today. The process of teeing up a taper and ending purchases could come to an end by late-2022 at which point it’s unclear that the Fed would want to keep rolling over maturing securities and providing extended support through maintaining the size of the overall SOMA bond portfolio through 2023. Note that the Bank of Canada did not embrace reinvestment from the beginning. The Fed could well embrace roll-off and let maturing securities drop off the books and hike soon after ending purchases.

Such a scenario would conform to the longstanding argument that this is a transitory shock being solved by science as monetary and fiscal policy dramatically overshoot requirements. To get to full employment and on inflation targets sooner than feared would be a wonderful achievement after tragic losses of loved ones, employment, financial and overall health. It could also coincide with an abrupt move higher in bond yields, market dislocation effects, concern over whether the US administration will know when to reverse its spending addictions, and concern over the long-run imbalances in the US economy including fiscal and current account deficits of such potential magnitude as to one day make the country undeserving of its reserve currency status and its associated privileges.

2. CENTRAL BANKS—HEAVY HITTERS AND ROLE PLAYERS

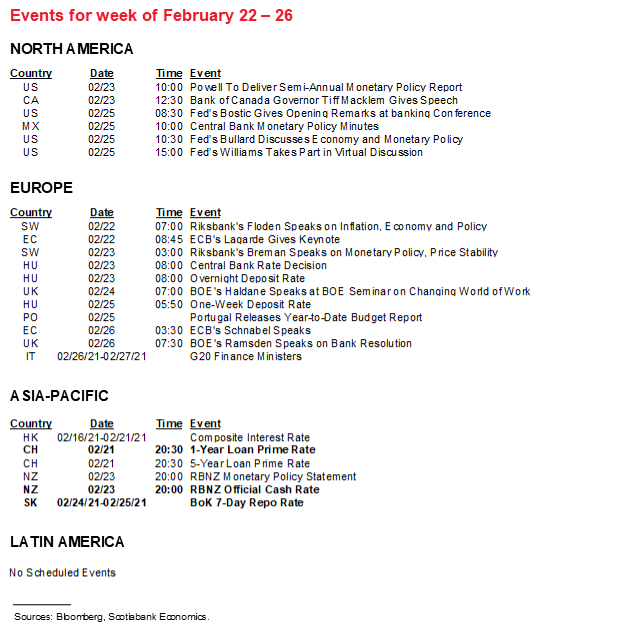

Three senior central bankers take to the stage next week from the Fed, ECB and Bank of Canada and three other central banks deliver policy decisions.

Federal Reserve Chair Jay Powell delivers the semi-annual Monetary Policy Report testimony on Tuesday at 10amET before the Senate Banking, Housing and Urban Affairs Committee and again the next day before the House Financial Services Committee. The MPR is available here, but it’s always the opening remarks that get released that day plus sometimes the early stages of questioning that matter. If he is asked about reinvestment and if he waffles, then ride the curve steeper yet.

Bank of Canada Governor Tiff Macklem speaks on Tuesday at 12:30pmET at a joint Edmonton/Calgary Chamber of Commerce event. His topic will be "Labour market impacts of COVID and sectoral implications." There will be a press conference at 1:30pmET. The topic suggests he will repeat his prior emphasis upon how the recovery is expected to continue to be uneven and many are being left behind. There are still 850,000 fewer employed people than there were last February before the pandemic and so, for now, the BoC is right to be in monitoring mode. Pushing back on curve steepening, however, may prove unwise given it’s a pretty haughty bet by a modest central bank to lean against powerful forces in global bond markets. The ways in which it may be attempting to do so include communications tactics, like emphasizing the currency (whatsoever the merit!) and present slack considerations, plus altering purchase programs such as raising provincial bond buying (again, whatever the merit).

ECB President Christine Lagarde speaks on Monday at about 8:45amET at a conference on stability, economic coordination and governance in the EU (here). Watch for remarks on forecast risks ahead of the next update on March 11th as well as potential elaboration upon her warning against "brutally" withdrawing supports plus her support for speedier implementation of common EU borrowing.

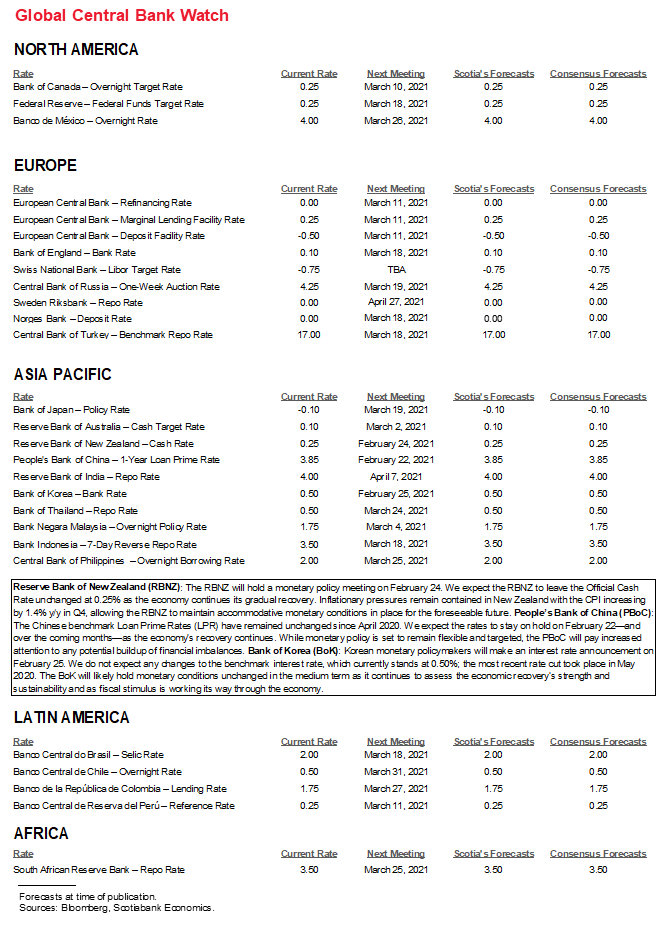

The People’s Bank of China is not expected to alter its 1-year Loan Prime Rate of 3.85% or the 5-year rate of 4.65% when it makes its decision early in the week. The Lunar New Year had a less pronounced effect on liquidity management by the PBOC this year. Like the US, given the managed yuan peg to the dollar, China’s bond market has also sold off recently (chart 4).

The Reserve Bank of New Zealand hasn’t delivered a policy decision since November 10th but is expected to leave its official cash rate unchanged at 0.25% on Tuesday while its government bond purchase program slows (chart 5). First implemented last March, the Monetary Policy Committee’s initial NZ$30 billion purchase program in the secondary market over a one-year period was subsequently increased over three separate announcements to a NZ$100 billion program by last August with a completion date of June 2022. To date, the program has bought just over NZ$45 billion of bonds. The central bank introduced a new Funding for Lending program at its last meeting and markets have largely priced out a negative overnight cash rate.

Bank of Korea is also expected to stay on hold at 0.5% on Thursday. The last statement on January 15th guided a prolonged hold by stating "the recovery in the Korean economy is expected to be modest and inflationary pressures on the demand side are forecast to remain weak." Governor Lee Ju-yeol has emphasized some concern toward household sector and market imbalances.

3. GRAB BAG!

i. G20: The G20’s finance ministers and central bankers meet virtually on Friday and Saturday, February 26 and 27. Expect a wholesale defence of fiscal and monetary policy efforts designed to nurture the global economic recovery.

ii. Canadian bank earnings: Fiscal Q1 earnings (Nov–Jan) arrive starting with BNS (my employer) and BMO on Tuesday, followed by RBC & National on Wednesday, and then CIBC & TD Thursday.

iii. US indicators: In addition to the consumer and inflation figures previously cited, there will be a sprinkling of other releases. Consumer confidence for February (Tuesday) might get a lift from stimulus cheques and enhanced unemployment insurance. The Richmond Fed’s manufacturing gauge on Tuesday will be a tie-breaker between the improvement in the Empire measure versus the modest dip in the Philly Fed’s results. New home sales (Wednesday) may face downside risk in January’s tally stemming from the decline in model home foot traffic from November to January, albeit that foot traffic remains at elevated levels. January’s durable goods orders (Thursday) will be shooting for the ninth consecutive gain in core orders ex-defence and air that serves as a proxy for equipment investment. The week wraps up with the first revision to the initial 4.0% Q4 GDP growth estimate.

iii. Alberta’s budget: Scotia’s Marc Desormeaux thinks we could see improved budget balance projections when Alberta releases its first pandemic era budget on Thursday and the comments in this section are his own. In line with guidance provided in November’s mid-year fiscal update (here), the government may delay providing a timeline to balance its books until more progress is made on COVID-19 inoculation, and continue to target a net debt-to-GDP ratio below 30%. That would update estimated deficits of C$21.3 bn (6.9% of GDP), $15.5 bn (4.7%), and $9.9 bn (2.8%) in FY21, FY22, and FY23, respectively.

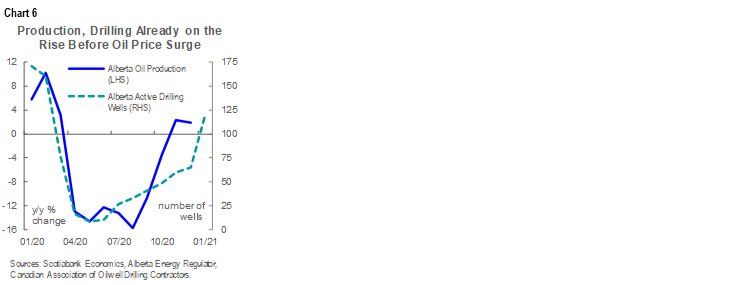

WTI climbed toward US$60/bbl this week, lifted by still-high OPEC+ quota compliance, broadly improving vaccination prospects, and demand- and supply-side effects from the blast of cold weather that is hammering southern US oil-producing regions. A lot can happen on all three fronts before the end of the next fiscal year, but the early-2021 surge puts crude closer to the optimistic 56 USD/bbl scenario outlined in November than the 45-dollar base case, and adds to production and drilling momentum building since late last year (chart 6). As a rule of thumb, the last several Alberta budgets have associated each 1 USD WTI price movement with a bottom-line impact of C$300–350. Partial offsets to economic growth and revenue may come from second wave restrictions—implemented after the last update was released—and diminished local employment and investment activity related to cancellation of the Keystone XL pipeline.

Government communications in recent weeks suggest that spending restraint will remain the focus of consolidation efforts. The mid-year update assumed a 9.6% reduction in program expenditures over FY22–23—a two-year pace influenced by expected drawdown pandemic spending but still not far off that completed during the historic, albeit longer consolidation period in the 1990s (chart 7). To the extent that a revenue surprise materializes, the Province may opt to ease FY22 expenditure cuts.

iv. European indicators: UK job markets and German business confidence will be the main focal points. The UK updates jobless claims for January and the change in employment during December on Tuesday, following a string of employment losses dating back to May by contrast to job market recoveries elsewhere (chart 8). German IFO business confidence in February (Monday) follows a rise in the ZEW investor expectations reading and completes the round of monthly sentiment gauges. Eurozone CPI will be revised for January on Tuesday after the initial -0.3% y/y reading. Sweden and Switzerland will release Q4 GDP estimates at the end of the week and both may be cooler following solid Q3 gains.

v. Asian indicators: Apart from central banks noted above, there will only be two batches of releases. India registers Q4 growth on Friday that should see the year-over-year rate barely turn positive after two steep quarterly declines. Japan’s monthly data dump unfolds toward the end of the week including updates for industrial production that should rebound nicely, retail sales that are expected to remain weak, Tokyo CPI that is likely to remain in mild deflationary territory, and housing starts.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.