Next Week's Risk Dashboard

• Brexit

• A different sort of US government shutdown?

• CBs: ECB, BoC, Peru, Chile, Brazil

• Inflation: US, Mexico, Chile, Brazil…

• …Colombia, Norway, Sweden

• European macro

• China macro

Chart of the Week

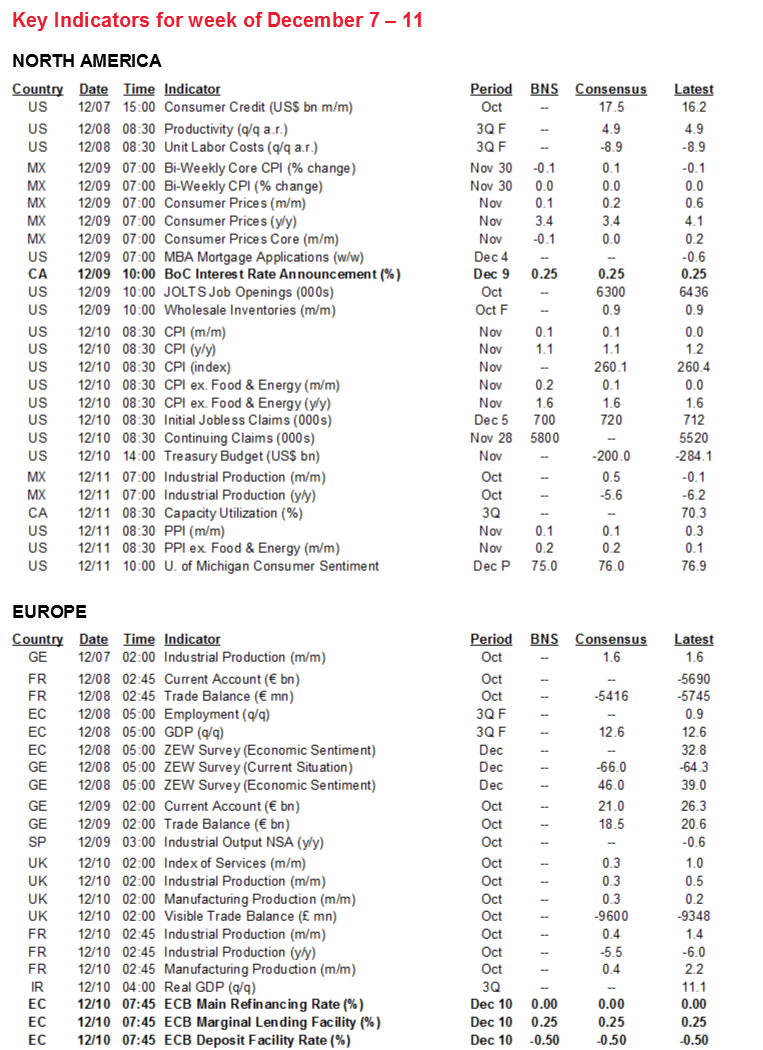

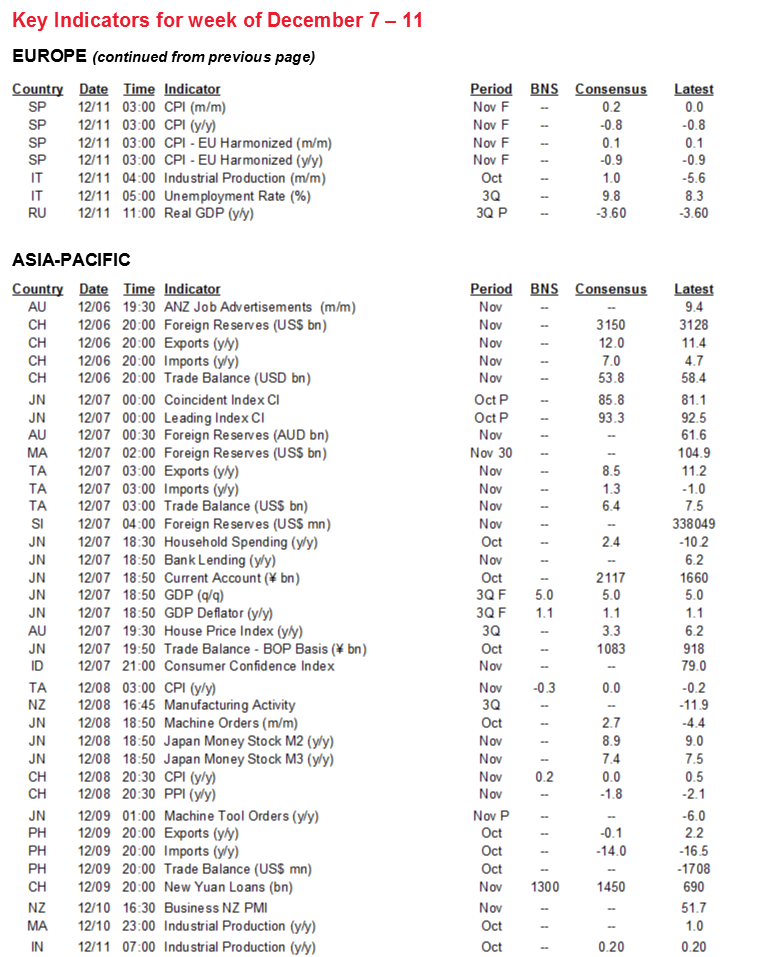

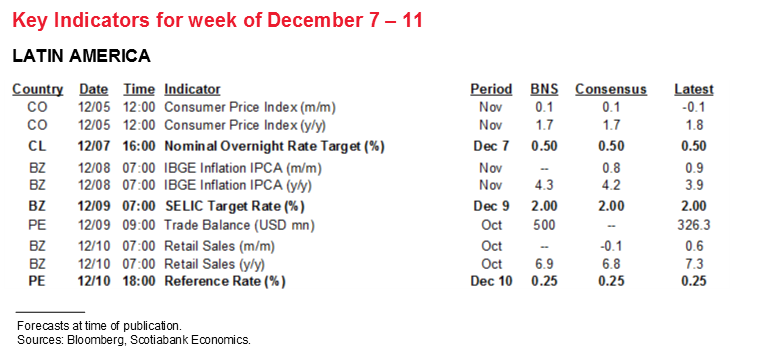

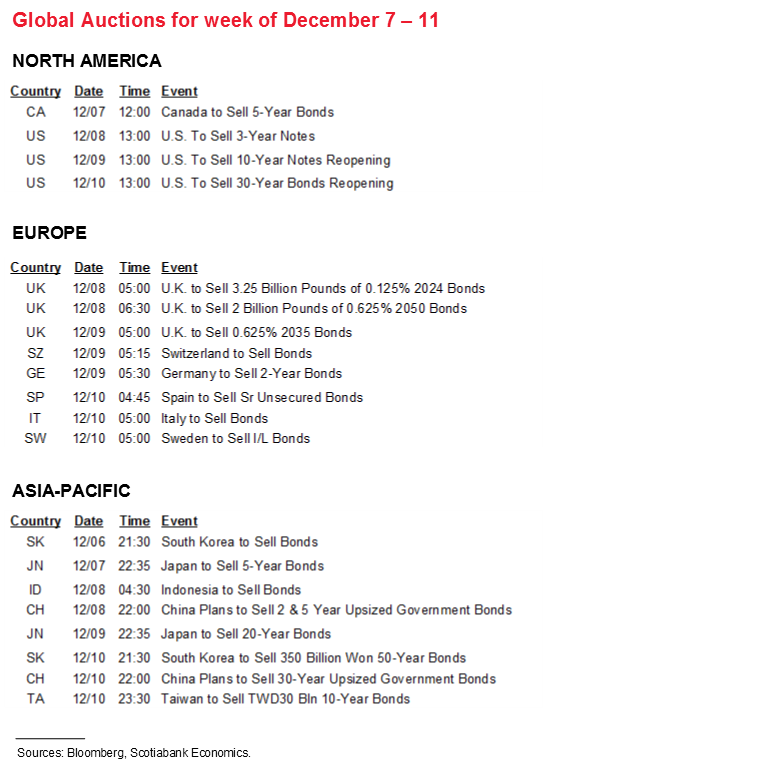

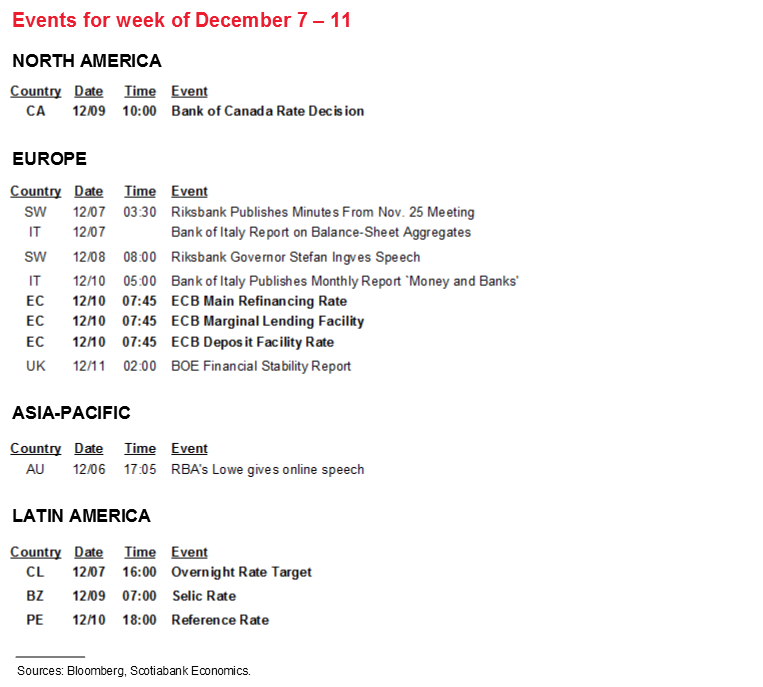

What if the week started with clearer evidence that the UK will leave the EU without a deal at the end of the year and ended with a US government shutdown? That is hardly a base case for how the overall week will unfold as it could wind up surprising for the better, but such will be the two dominant risks overhanging markets as the week progresses alongside possibly tying US stimulus talks to the overall outcome. How the ECB delivers on earlier promises to deliver stimulus may well be informed by one or both matters, while other regional central banks like the Bank of Canada and a trio in Latin America will largely watch from the sidelines. The calendar of top-tier macroeconomic reports will be otherwise sparsely populated and summarized in the accompanying indicator tables.

1. NOT JUST YET ANOTHER US GOVERNMENT SHUTDOWN?

The US system of governance has pros and cons and probably at least its fair share of quirks that either entertain, frustrate or mystify observers at home and abroad. To the list that includes Electoral College rules, endless vote recounts, deeply partisan tactics, and the absence of a clear mechanism for removing a President who lost, one can add the obscure ways that it funds government. The latter risks becoming glaringly evident once again over the coming week.

Absent an agreement, funding for almost all federal agencies will expire on December 11th. What is needed is a bill that would allocate US$1.4 trillion in funding through to the end of the fiscal year on September 30th 2021. Failure would mean shutting whole government departments until agreement can be reached.

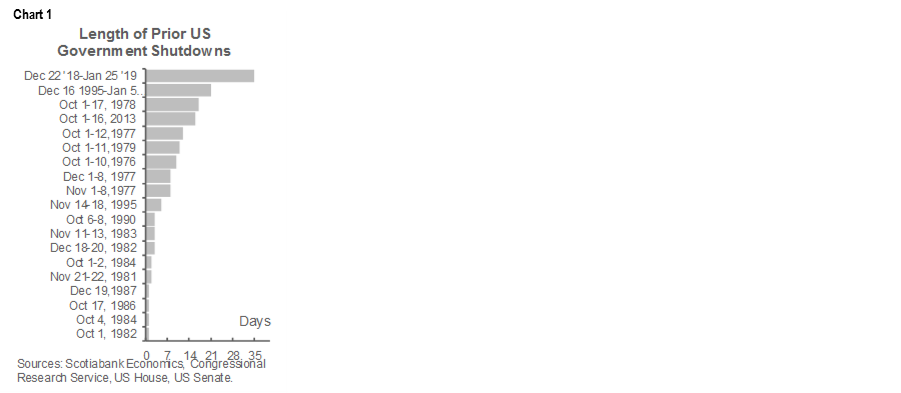

Market observers have seen this movie many times. Chart 1 depicts government shutdowns that have occurred since the 1980s and ranks them in order of length. The 35 days in late 2018 into early 2019 over Trump’s border wall funding dispute was a record breaker and serves as a clear warning with respect to his single-minded obstinance.

Market observers also generally understand that shutdowns usually have little effect on GDP growth. For example, the CBO estimates for the impact of the 2018–19 shutdown on quarterly GDP growth are shown in chart 2 (and explained here).

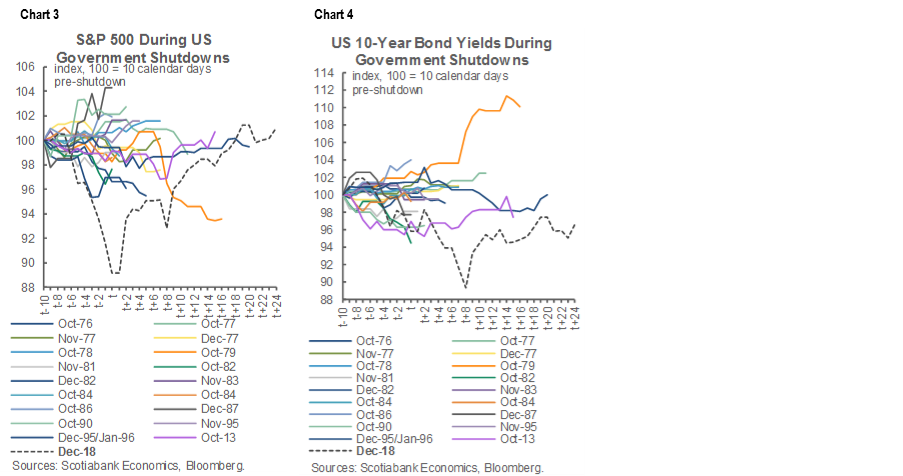

The de minimis impact on markets is also generally understood. Charts 3 and 4 plot the performance of the S&P500 and the US 10 year Treasury yield leading up to and after past government shutdowns. Every instance is different, but a clear-cut risk-on or risk-off pattern is hard to detect.

If an omnibus spending agreement is not passed in time, then it’s possible Congress passes a continuing resolution to bridge funding needs which would make it a problem for the next Congress that convenes in January. A full government shutdown is a modest risk in my opinion, but at least this is not like the debt ceiling crisis in late 2013 and early 2014 in that the debt ceiling was already suspended in mid-2019 for two years until next summer when it may become an issue again.

All that said, this could get a bit more complicated than the plain vanilla shutdowns of the past. One reason is Trump and his agenda in his final days in office. For example, he has threatened to veto a defense authorization bill if it includes a provision to rename military bases presently named after Confederate leaders. Some would say that’s the President being consistent, but not terribly ‘woke’ to say the least.

Further, this time Congress is trying to nail two birds with one stone which magnifies the negotiating risks as well as the potential reward. In addition to the December 11th deadline is the expiration of various forms of CARES Act aid on December 31st including jobless benefits and eviction moratoriums. House Speaker Pelosi and Senate Majority Leader McConnell are seeking to combine an omnibus funding bill with a stimulus package in one. That could be quite constructive if they can pull it all off, but it raises the spectre of everything getting stuck in Washington’s dysfunctional wheels.

Enter competing proposals for the stimulus part of the equation that are in significant disagreement. A bipartisan proposal would spend US$908 billion while the GOP-controlled Senate led by McConnell is aiming for about US$500 billion. It may be a positive thing that the previously much wider gulf has been narrowed at least until the Democrats can take another swing at stimulus when President-elect Biden takes office. The bipartisan proposal includes US$288 billion in Paycheque Protection Program loans to small businesses, an extra $300/week supplemental jobless benefit and US$160 billion for state and local governments plus targeted spending efforts. McConnell’s bill would temporarily extend jobless benefit eligibility, fund PPP loans and include targeted measures but would not include more jobless benefit payments or aid to state/local governments. A sticking point is that the GOP plan would shield businesses from any COVID-19 related lawsuits which the Democrats object to doing. Added sticking points include additional funding for the Mexican border wall, for immigration detention, for education and environmental programs and for contentious family planning programs.

In all, I’m inclined to be hopeful that the worst-case scenario may be a continuing funding resolution and modest stimulus to bridge through the year-end expirations. The fact that so much is tied together with this potential shutdown while anything that is done needs Trump’s signature is a bit nerve-rattling and perhaps more so than during past shutdowns.

2. CENTRAL BANKS—WHEN IS ENOUGH ENOUGH?

i. ECB—Over-promise, Under-deliver?

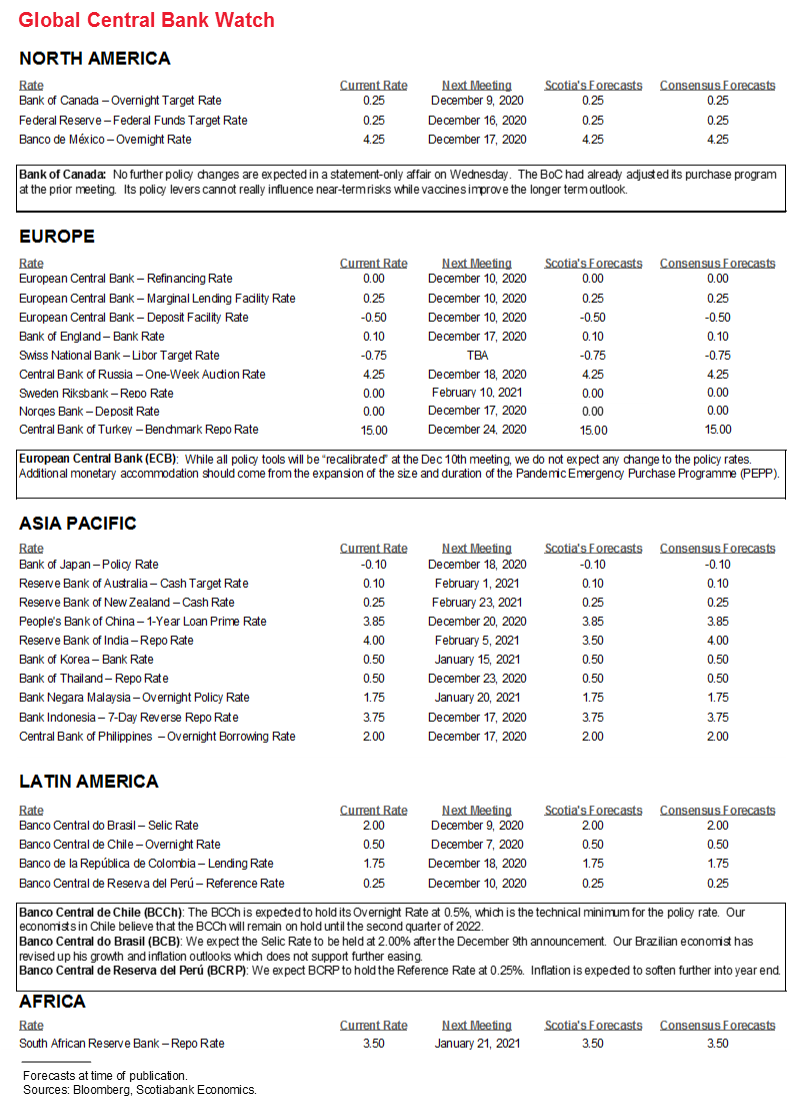

The European Central Bank delivers its last policy decision of the year on Thursday at 7:45amET (statement) followed by President Lagarde’s press conference at 8:30amET. The central bank had built high expectations for policy action into this meeting, but exactly what it may deliver is uncertain not least because of events since the last meeting.

On October 29th, Lagarde made it clear that the ECB would be expanding stimulus at the December 10th meeting. The statement noted that “Governing Council will recalibrate its instruments” at the coming meeting which is ECB code language for expanding stimulus. Lagarde noted that Governing Council was unanimous in its belief that more needed to be done and that this involved looking at all instruments. Since that time, COVID-19 cases across the whole of the European Union went from just under 6 million to more than double that now. Furthermore, the euro has appreciated by another 4% to the USD, although inflation has been little changed at -0.3% y/y and with core CPI at 0.2% y/y. Nevertheless, all of the positive vaccine trial announcements were made since the last meeting.

So where does that leave the ECB? It has to do something material after promising it would, but it might not want to over-commit to multiple tools over an extended horizon. That could risk disappointment in the near-term. As this past week drew to a close, anonymous officials at the rather leaky ECB were reportedly considering a one-year extension of its existing €1.35 trillion Pandemic Emergency Purchase Programme (PEPP) from “until at least the end of June 2021” to at least one year later. It sounds like garbled guidance to me with some preferring six months and some advocating a conditional withdrawal trigger should things really rip as they may well do. Presumably they might extend reinvestment guidance beyond “at least the end of 2022” if they are buying until mid-2022.

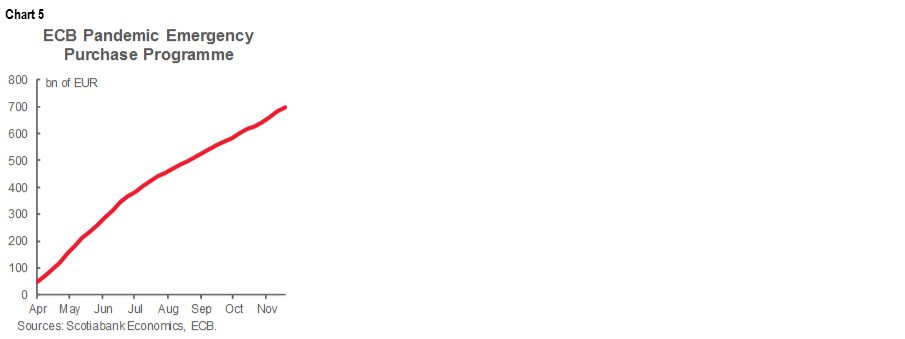

Nevertheless, only half of the existing potential size of the PEPP has been utilized thus far and the rate of increase of the assets held within the program has slowed since July compared to prior months (chart 5). Extending and raising the purchase horizon and time horizon by at least 6–12 months is one thing, but what markets think it might actually implement may differ. Underutilized facilities are hardly a rarity across central banks including the Fed and the Bank of Canada as other examples.

ii. Bank of Canada—Uncertainty Surrounds its Certainty

The Bank of Canada issues its final policy statement in a wild year on Wednesday at 10amET. It will be a statement-only event followed by the next day’s Economic Progress Report speech to be delivered by Deputy Governor Paul Beaudry at 1:30pmET.

Expectations are set rather low for this one. No changes in either the policy rate or the BoC’s Government of Canada bond purchase program are expected. The statement will be a full rewrite compared to the prior forecast-oriented one, but it is likely to convey some sense of three main messages: near-term risks have risen with the spread of COVID-19 and tightened restrictions; vaccines offer greater hope and the US election is out of the way; but an extended period of accommodation is likely as it will take time to repair the damage brought on by the pandemic.

For one thing, the BoC is in between forecast exercises following the October 28th Monetary Policy Report and with the next one not until January 20th. The BoC might still view its late-October forecasts as roughly on the mark given how increased COVID-19 cases are dampening the near-term but vaccines are lifting longer-term optimism.

For another, the BoC only just changed up its purchase program at the late-October meeting when it lowered the purchase flows into Government of Canada bonds from at least C$5 billion per week to at least C$4 billion per week and shifted the composition of those purchases toward longer term maturities.

Recent remarks by Governor Macklem emphasized further policy flexibility, but only conditional upon a worsened scenario. They included possibly cutting the overnight rate a little further below 0.25% while staying positive, negative rates being in the toolkit but not under present consideration, and scaling existing purchase programs. None of these steps are expected next week but if there is a risk then the most likely might be to reduce the overnight rate by 10–15bps. I don’t think that will happen and it would be kind of pointless anyway.

In a stylized facts sense, the BoC should feel no compelling urge to alter stimulus now and the dialogue over 2021 is likely to gradually transition toward bracing markets for eventual policy exits. For one thing, while COVID-19 has carried tragic effects upon too many, Canada’s break-out is considerably lower than in the US (chart 6).

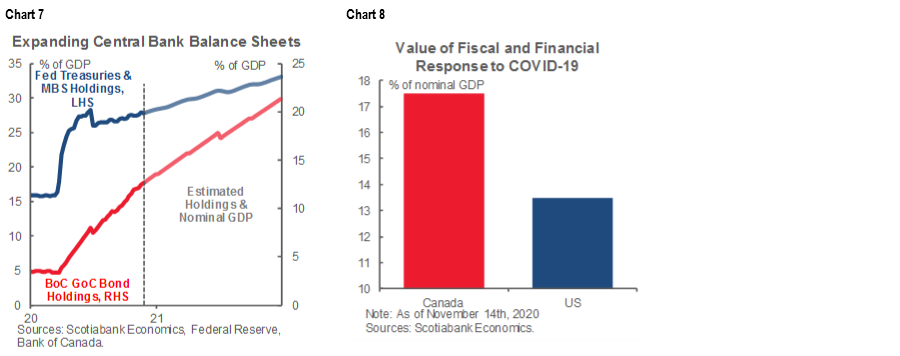

For another, the stimulus response has been greater in Canada. The BoC’s bond buying program has risen as a share of GDP at a quicker pace than the Fed’s this year, though you could argue the Fed had a running start because it had already been in the QE game for many years and so its bond holdings are a higher share of GDP overall (chart 7). As a share of GDP, fiscal stimulus in response to the pandemic has also been materially greater in Canada than in the US (chart 8).

By extension, the impact upon inflation has perhaps also reflected fewer COVID-19 cases and greater stimulus. Canada’s core inflation is running materially higher than in the US (chart 9).

While there was a more vibrant debate on possibly further policy options over the Fall, the arrival of vaccines across the US and UK now followed by Canada as 2021 unfolds should give reason to press pause on concepts such as yield curve targets.

The BoC needs to be careful that it does not over-promise what it can deliver upon. Telling heavily indebted Canadian households to count on rates staying very low for years to come may be over-reaching. Ditto for many small businesses. For one thing, the BoC does not have full control over longer maturity borrowing costs, such as the five-year Government of Canada bond yield that has been modestly climbing since mid-October and that would be expected to rise well ahead of an eventual BoC rate hike. This yield serves as input into determining the popular five-year mortgage rate. For another, it seems incongruent to say that forecasting is marked by such high uncertainty—especially with vaccines on the horizon that may buoy the outlook—versus saying that it is certain the policy rate won’t budge for years to come.

iii. Latam

Three Latin American central banks issue policy decisions but none of them are expected to alter their stances. Chile’s central bank weighs in on Monday followed by Brazil’s central bank on Wednesday and Peru’s on Thursday.

3. BREXIT

Brexit talks didn’t exactly end the week well! They spent the whole week trying to break the logjam over issues related to British sovereignty, but in the end largely failed to do so. The way the talks ended leaves risks to global markets—but particularly sterling and local UK assets—hanging in a state of total ambiguity into the Asian market open.

At the time of publishing, negotiations had just broken up. The EU’s negotiator, Michel Barnier, stated “After one week of intense negotiations in London, together with @DavidGHFrost, we agreed today that the conditions for an agreement are not met, due to significant divergences on level playing field, governance and fisheries. We agreed to pause the talks in order to brief out Principals on the state of play of the negotiations.”

European Commission President Ursula von der Leyen and British Prime Minister Johnson will have a discussion on Saturday afternoon. About what isn’t exactly clear. Barnier is expected to brief EU ambassadors on Sunday. I’d like to be cautiously optimistic that perhaps now the rubber hits the road with the elected leaders forced to step up and decide what’s supportable by way of compromises that their negotiators could not achieve. That wouldn’t be the first international agreement settled in such fashion, but it’s hard to see how one could have much confidence in this expectation after years of trying. Either way, there are less than three weeks until the January 1st 2021 leave date with-or-without a deal and no finalized legal text and no translations underway.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.