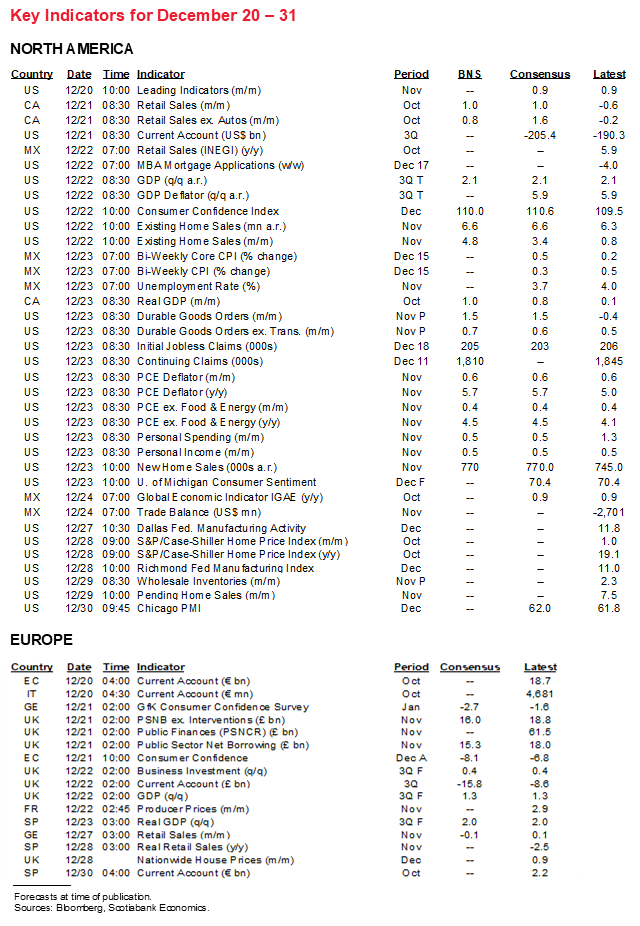

Next Week's Risk Dashboard

• Off-calendar risk to dominate

• Tracking omicron + delta

• China PMIs might begin capturing omicron effects

• Canada’s economy and the BoC

• Tracking the US economy

• The Fed’s preferred inflation gauge

• Chile’s election

• CBs: PBOC, BoT

Chart of the Week

First, I’d like to wish our clients, staff and friends the very best of the holiday season and the fast-approaching new year. Safety and one’s health remain paramount considerations while making the best of a traditionally festive time of year.

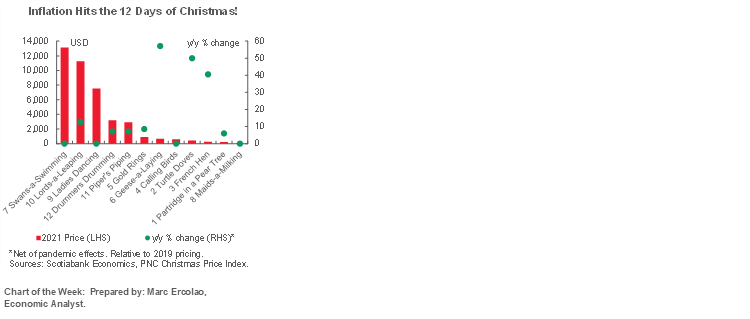

I sure hope Santa’s all vaccinated and boosted! It’s certainly a more expensive time of year as the inflation tax is taking its bite out of budgets! Marc Ercolao’s playful focus chart on the cover of this issue shows that it has never cost you more to buy the twelve gifts from the song titled “The Twelve Days of Christmas.” They’d set you back a cool US$41,206, with the source describing core prices (ex the expensive swimming swans) at US$28k.

Amid the festivities into the new year, calendar-based risks—including central bank decisions, economic indicators and events whose timing is known—will likely be rather light throughout the holiday period.

TRACKING COVID-19

That will probably mean that most of the risks facing markets will be off-calendar in nature and particularly focused upon monitoring the spread and impact of the omicron variant.

As this publication goes to virtual print, there is a blend of worrisome and encouraging evidence around COVID-19 developments applied to informing developments in the economy and financial markets.

On the worrisome side is that while the numbers are still small so far, more schools have been closing in whole or in part in some jurisdictions that are witnessing rising numbers of student cases (chart 1). That could make labour markets vulnerable into the new year particularly if this persists through the mid-January reference periods for reports like US nonfarm payrolls and Canadian jobs. The impact tends to fall disproportionately upon younger- to middle-aged women based upon pandemic experiences to date.

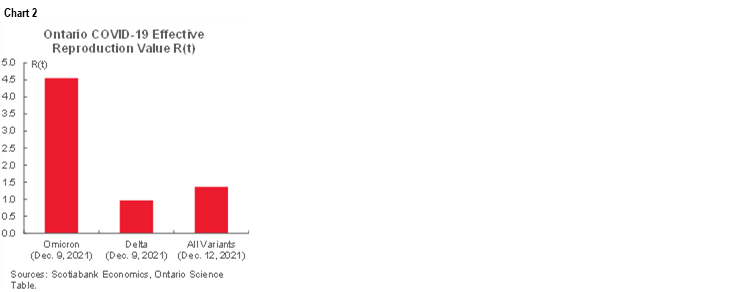

Furthermore, there is evidence that omicron may be much more transmissible than prior variants (chart 2) but it remains unclear whether it is comparable in terms of the severity of outcomes. Early evidence suggests that on average omicron may result in less severe outcomes, but an uncertainty is whether lower average intensity of effects may be applied against potentially vastly greater number of cases and pose still large numbers of hospitalizations and worse outcomes. Time will tell and forecasts from public health agencies suggest we will know a lot more about these risks by early 2022.

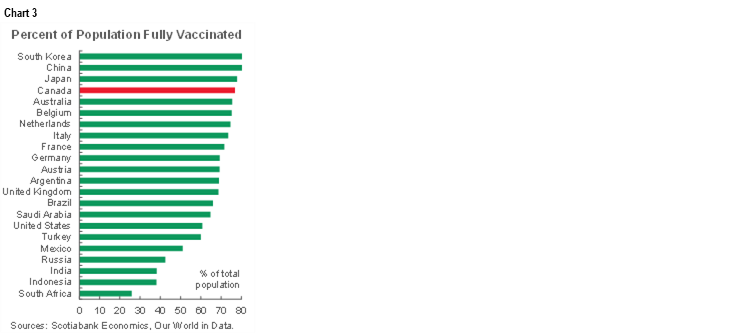

On the more positive side, early studies still tend to indicate that vaccines provide strong protection against variants other than omicron and that are still in circulation. Vaccines seem to perform reasonably well against omicron in terms of severe outcomes but less well in terms of protecting against any symptoms. It therefore remains extremely important to strive toward higher vaccination rates. Chart 3 is getting to be more encouraging in combatting variants prior to omicron.

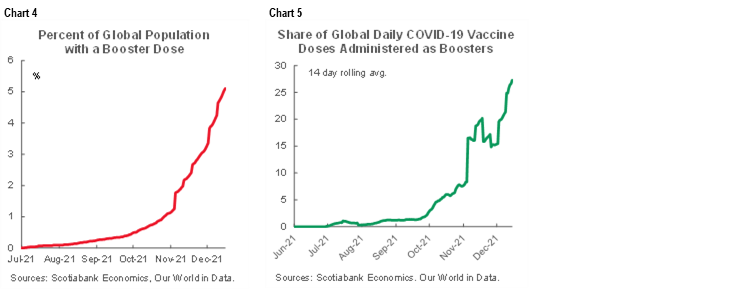

Progress on additional boosters remains at a very preliminary stage, however, which must rapidly improve given evidence they are needed to supercharge immune systems against omicron (charts 4, 5).

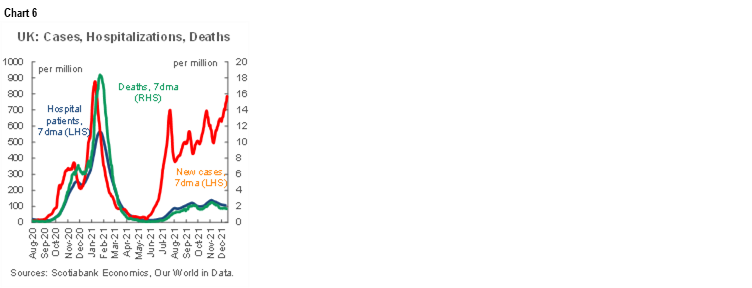

Hospitalization and death rates are so far better behaved than during prior waves (chart 6), but obviously the uncertainty around severity of outcomes associated with the omicron variant and the lags involved following infection make it too early to judge.

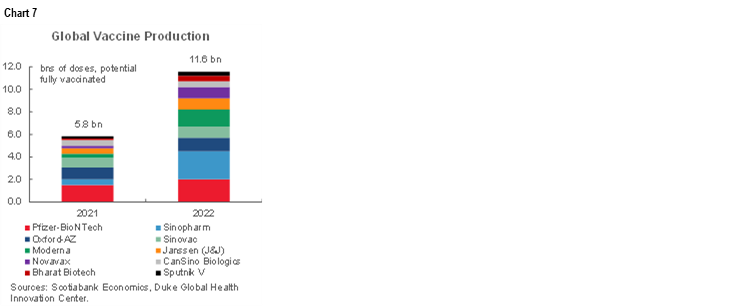

Finally, if new vaccines are required, I’d repeat the point about how the ability to supply enough should not be the issue into 2022 that it was in the early days. Chart 7 shows the massive increased in vaccine production plans in addition to what has already been an explosive rise this past year.

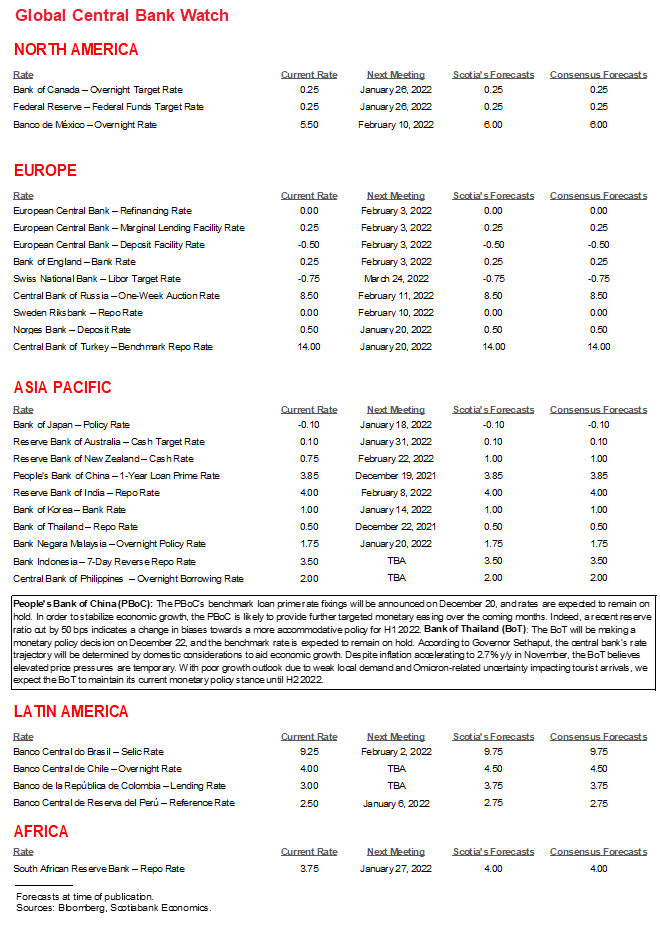

CENTRAL BANKS—JUST TWO LEFT IN 2021!

Central bank watchers, you deserve a break! Just about every central bank on the planet fired off missives of late. There are only two left before the calendar flips over to 2022 and they are expected to stand pat.

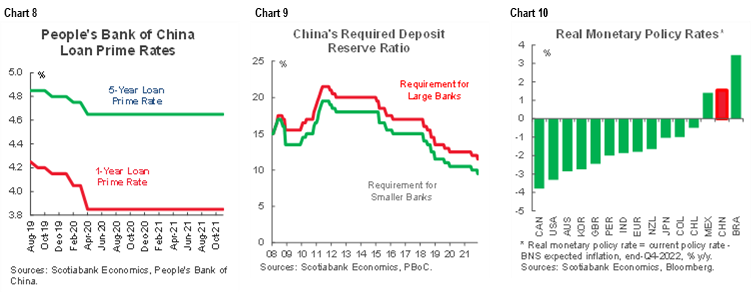

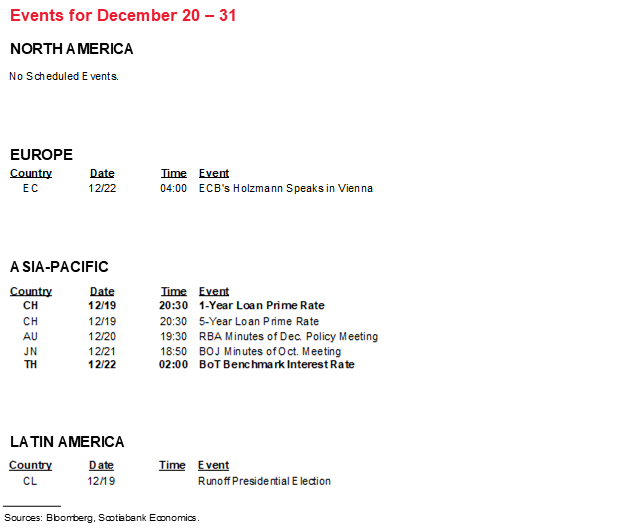

The People’s Bank of China is expected to leave its de facto policy rates unchanged at the start of the first week of the holiday season. The 1-year and 5-year Loan Prime Rates are unanimously forecast to remain at 3.85% and 4.65% respectively. The PBOC has not cut its LPRs since April 2020 as part of an easing campaign that pre-dated the pandemic (chart 8). Policy easing since then and through other means has been relatively modest including a recent reduction to the required reserve ratios (chart 9). China is still left with among the world’s highest real (inflation-adjusted) policy rates (chart 10).

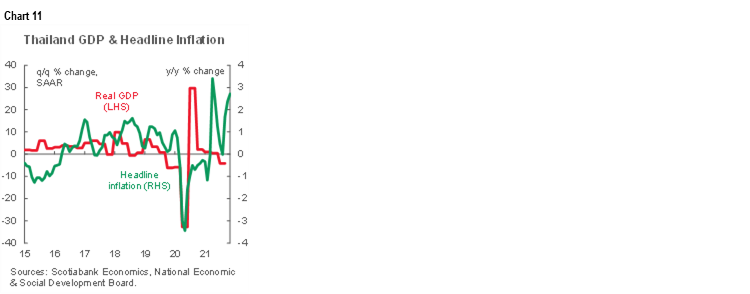

The Bank of Thailand is universally expected to stay on hold at a policy rate of 0.5% on Wednesday. The central bank is very unlikely to be thinking about hiking, given moribund economic growth in an economy that has incurred damage to its tourism business due to the pandemic. Furthermore, by contrast to many other parts of the world, there is very little inflationary pressure. Chart 11 shows the growth and inflation dynamics. On the flip side, the BoT is also unlikely to cut its policy rate that is basically toward the lower effective bound already and given concern that further easing would drive destabilizing capital outflows that could drive additional weakness in the currency. The Thai Baht has depreciated by over 10% to the USD this year. This is among the financial stability concerns that have resulted in Thai monetary policy being stuck between a rock and a hard place.

MACRO REPORTS—US, CHINA, CANADA IN FOCUS

Amid forward-looking risks, most of the very limited number of global macroeconomic indicators that are on tap throughout the two-week period will be of modest consequence because they are backward-looking.

China’s PMIs Could Show Early Global Omicron Effects

The state’s versions of China’s purchasing managers’ indices may be an exception, and they arrive on December 30th in the evening (eastern time zone). These sentiment gauges will be fresher than much of the rest of the global line-up but will probably still lag in terms of the implications of recent global pandemic developments. The composite PMI has been mildly rebounding of late but could be vulnerable to damaged global supply chains (chart 12).

Canada’s Economy and the Bank of Canada

Canada will offer updated tracking of the economy’s performance during Q4 through both firmer estimates of activity in October and preliminary ‘flash’ estimates of what happened in November. All of the (limited) action lands in the first of the two weeks before the country’s macro calendar goes to sleep. It’s worth spending a bit more time on this given that a BoC rate hike looks to be increasingly in play.

Canadian GDP for October (Dec 23rd) had been guided toward a rise of 0.8% m/m by Statistics Canada back on November 30th, but the subsequently strong 1% m/m rise in hours worked could add upside risk to this estimate which is why I went a little higher than the preliminary estimate. Very few readings are available thus far for the month of November, but a 0.7% m/m rise in hours and a strong 26% m/m gain in housing starts are encouraging. Retail sales figures during October and November’s flash guidance (Dec 21st) will also marginally help to further inform GDP tracking and so far we have the preliminary estimate for a 1% m/m rise in October.

Based upon monthly GDP estimates, we could be tracking growth on the order of ~5% q/q at a seasonally adjusted and annualized rate. An alternative ‘nowcast’ approach estimates Q4 growth at just over 6½% (here) based upon quarterly expenditure-based GDP accounts. This may face downside risk as BC flooding effects are more fully incorporated, but that could still leave growth tracking materially stronger than the Bank of Canada’s forecast Q4 GDP growth rate of 4% in its most recent iteration in late October.

If so, then the output gap measure of slack might be shutting faster than the BoC anticipated. If the BoC figures that price and wage signals may be indicating greater than previously assumed damage to the supply-side and perhaps further downgrades estimates of potential GDP growth, then whether slack closes in Q1 or Q2 could be a very close call.

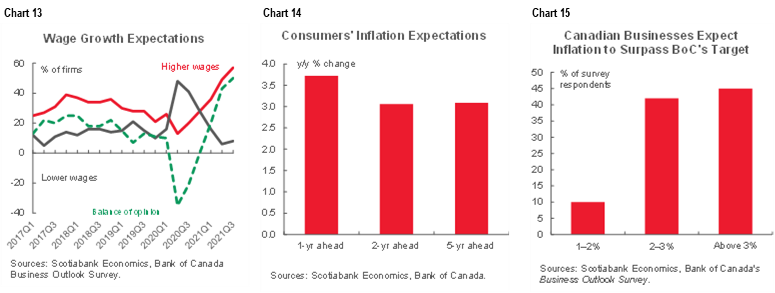

Nevertheless, high inflation and inflation expectations are capturing the Bank of Canada’s attention much more of late than output gap references. A January hike that would be earlier than our April forecast cannot be ruled out. It could be delivered by either dropping prior forward guidance not to hike until slack is fully shut, or by amending its estimates of when slack in the economy is eliminated. In addition to the output gap dynamics cited above, Governor Macklem has recently been much more pointed about his inflation concerns (recap here). His emphasis upon “closely” watching measures of inflation expectations and wages and “watching incoming data very closely” set up increased focus upon wage updates plus measures of wage and price expectations in the next Bank of Canada surveys on January 17th after the prior versions accelerated (charts 13–15).

Modest US Updates

US releases will be light and almost entirely concentrated in the period before Christmas.

- PCE inflation (December 23rd): The Fed’s preferred inflation gauges are likely to follow CPI higher but a little less acutely so. I’ve gone with an acceleration in headline PCE inflation to 5.7% y/y (5% prior) and core PCE at 4.5% y/y (from 4.1% prior).

- Consumption and incomes (December 23rd): Total consumer spending in November might have posted a stronger gain than the soft retail sales report that was little changed. One reason is an assumed rotation toward heavier services spending. This rotation could be vulnerable again if rising COVID-19 cases turn more shoppers back to shopping online for goods. Income growth was probably similar to the prior month’s gain of ½% m/m and so far the quarter is shaping up to post relatively modest income growth (chart 16).

- Durable goods orders (December 23rd): Key here will be whether the streak of 8 consecutive months of rising core orders (ex-defence and air) that serve as a proxy for underlying business investment is kept alive (chart 17). That would serve as ongoing evidence of gradual repair to capacity shortfalls.

- Q3 GDP (December 22nd): No material revision is expected to the final take on Q3 growth of 2.1% q/q annualized. This round of estimates incorporates more complete services information from the Census Bureau’s Quarterly Services Report (here).

- Consumer Confidence (December 22nd): The Conference Board’s measure for December faces competing risks between a strong job market and rising wage pressures versus the early effects of omicron and delta cases on consumer attitudes.

- Housing: On December 22nd, existing home sales should benefit from strong gains in pending home sales that get inked 30–90 days ahead of completed resales. New home sales for the same month of November (December 23rd) could post a further gain given evidence of rebounding model home foot traffic (chart 18). Pending home sales for November arrive on December 29th.

Europe’s calendars will be quiet with nothing out in the first week of the holiday season. German retail sales during November and Spain’s kick-off to another round of Eurozone inflation data will be the mild focal points.

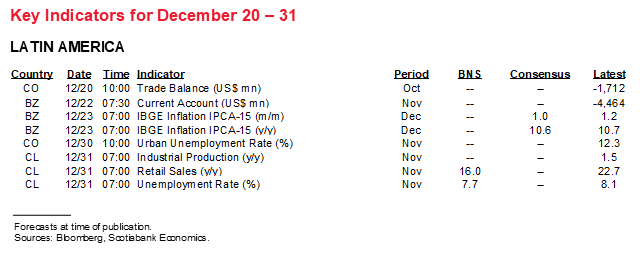

The main focus across Latin American markets will be Chile’s election outcome. The indicator line-up is fairly unimpressive. Mexico updates retail sales for back in October, bi-weekly inflation and the unemployment rate before Christmas. Chile’s retail sales, industrial production and unemployment rates will be focal points during the second week.

The rest of the Asia-Pacific line-up will be light. Most of the focus will be upon Japan’s monthly data dump that includes CPI for November (23rd) followed by releases on December 26th for retail sales, jobs and industrial production. South Korea also updates CPI on December 30th.

CHILE’S ELECTION

Chile’s final run-off vote in its Presidential elections will be held on Sunday December 19th. Financial markets and particularly the peso will be closely monitoring the outcome both in the immediate aftermath and as resulting policy stances are evaluated.

Polls are very tight and with a sizable undecided component (chart 19). José Antonio Kast represents the Partido Republicano which appeals to conservative voters whereas Gabriel Boric appeals to far left supporters. Here is a useful additional primer on the candidates, the lead-up to this final vote and to some of the key election issues.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.