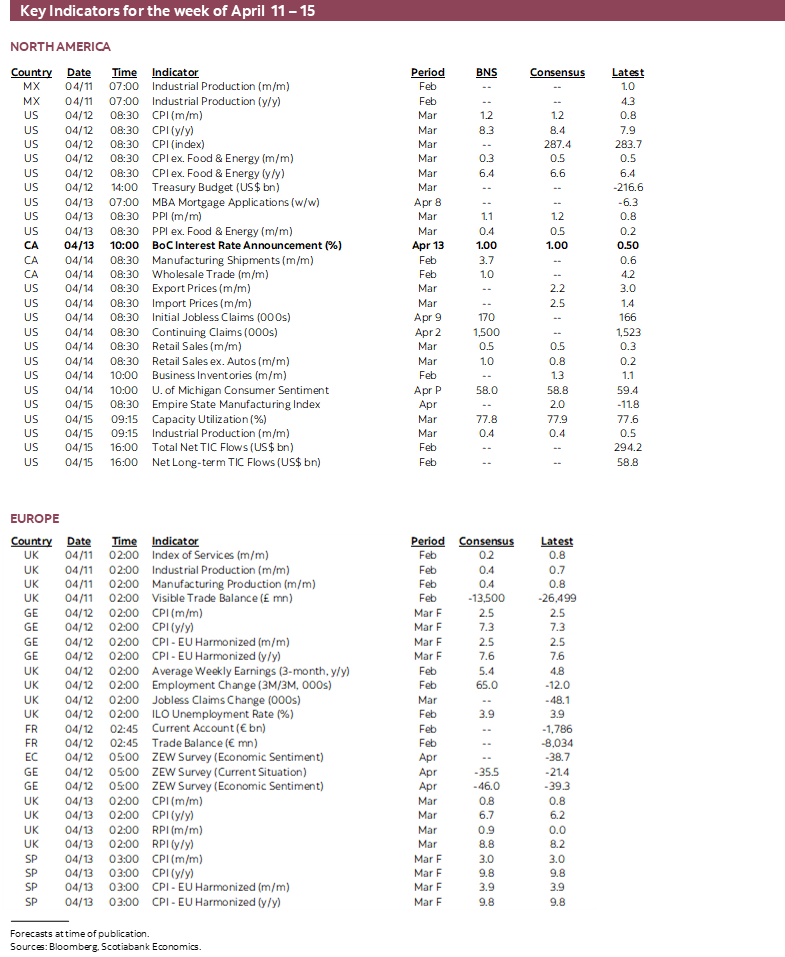

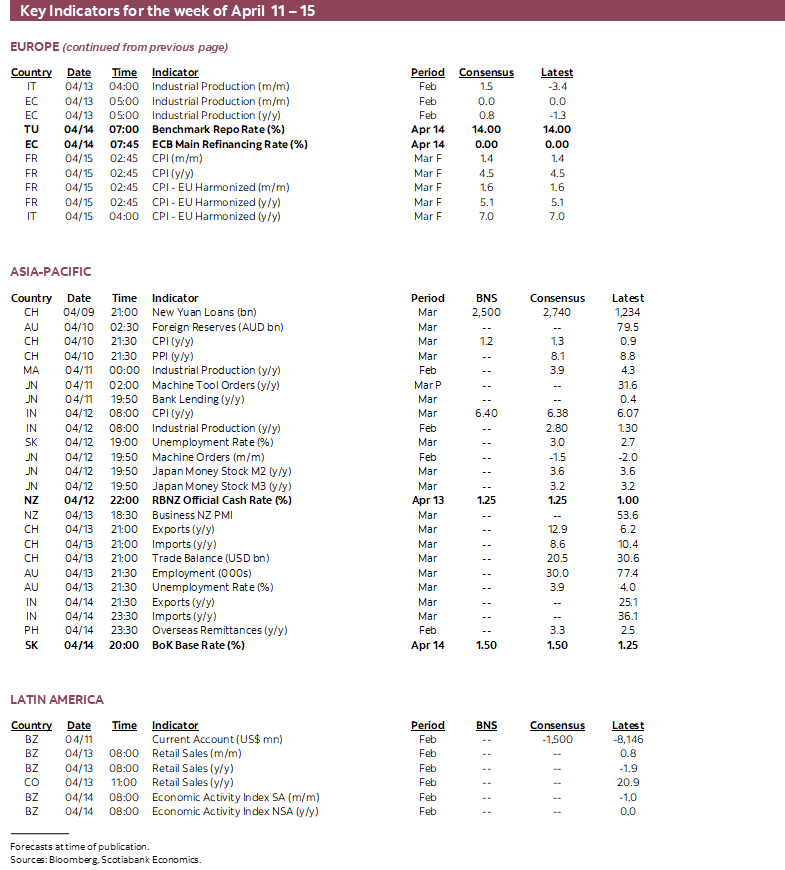

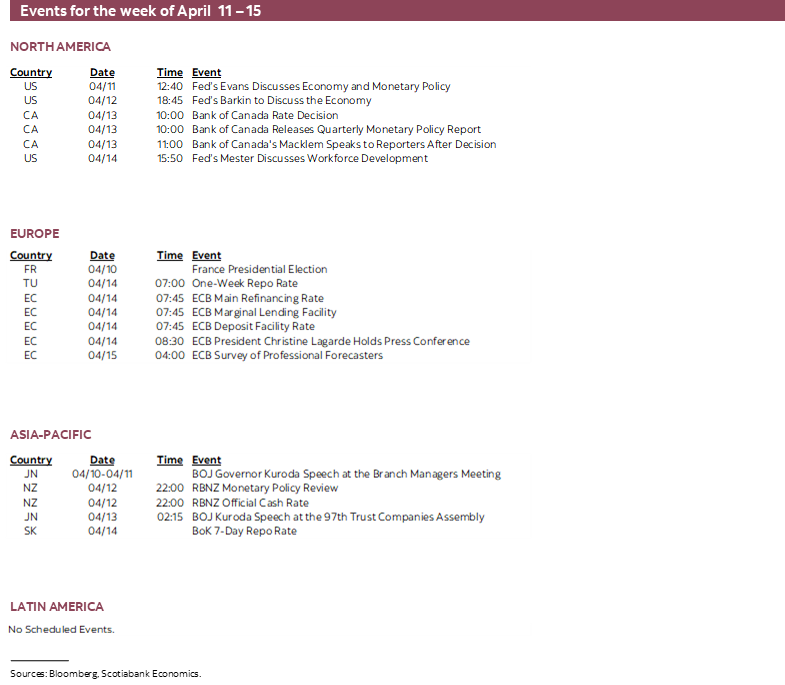

Next Week's Risk Dashboard

• France’s first-round election

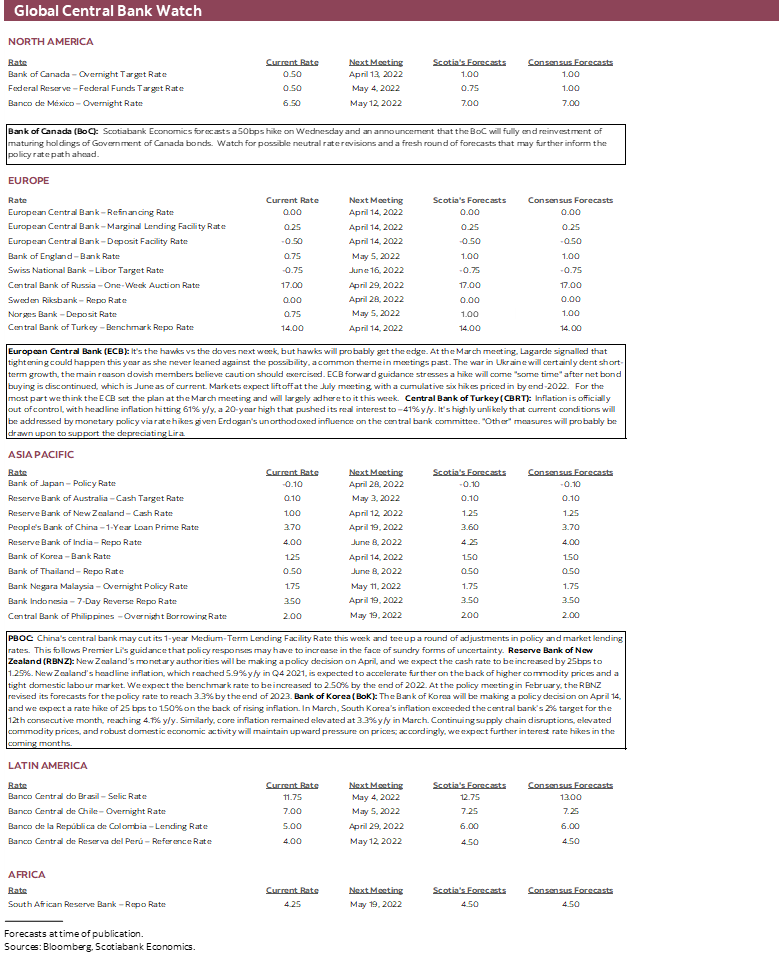

• BoC to ditch ‘gradual’

• ECB likely to stick to the March plan

• PBOC likely to cut

• US CPI inflation to hit 40-year high

• US Q1 bank earnings

• RBNZ, BoK to hike

• Jobs: UK, Australia, SK

• Other CPI: China, UK, India, Norway, Sweden, Argentina

• Other global readings

Chart of the Week

BANK OF CANADA—SO LONG, GRADUAL AND MEASURED!

It’s priced. They’ve intimated as much without explicitly saying so. So we can confidently say they’ll do it, right? Uh oh. Economics can be a rather ageing field of inquiry.

Anyway, we’ll find out on Wednesday at 10amET when the Bank of Canada issues its latest policy statement this time accompanied by a fresh Monetary Policy Report including revised forecasts. Governor Macklem and Senior Deputy Governor Rogers will host a joint press conference at 11amET for somewhere between a half hour and an hour depending upon the outside temperature.

We expect a 50bps rate hike and have been leading consensus in this regard. A larger hike cannot be ruled out. OIS markets have a full half-point hike priced and part of an additional quarter point for this meeting. Twenty-five of 31 economists in Bloomberg’s poll expect a 50bps hike including all major primary dealers, while the remaining minority expect 25bps. While there are two-tailed risks to the magnitude of a hike at this meeting, there is probably a fatter tail chance of hiking more than 50bps rather than less.

Why? Our case has been rooted in the view that the BoC is seriously behind in its fight against inflation. Central bank guidance appears to have recently pivoted in this direction. In her speech on March 25th, Deputy Governor Kozicki stated that “I expect the pace and magnitude of interest rate increases and the start of QT to be active parts of our deliberations at our next decision in April.” She also noted that “we are prepared to act forcefully.” That kind of central bank language followed by anything less than a half percentage point would be like confidently stepping up to the tee only to pull out a putter.

On potentially hiking more than 50bps, the challenge here is a communications one. The BoC was slow to pivot toward recognizing deep underlying forces to inflationary pressures and only did so by December. Governor Macklem delivered a speech in December that intimated he was leaning toward tightening policy, and markets were almost fully priced for a quarter point hike, but he chose to pass only to hike by ¼% at the March meeting because of the weak argument they wanted to spell out a hike in the statement and then go weeks later. To swing around and hike by 75-100bps in one shot now would have some merit in terms of how far behind the BoC is in the inflation fight, but it would not build confidence in the BoC’s guidance that it prefers measured approaches.

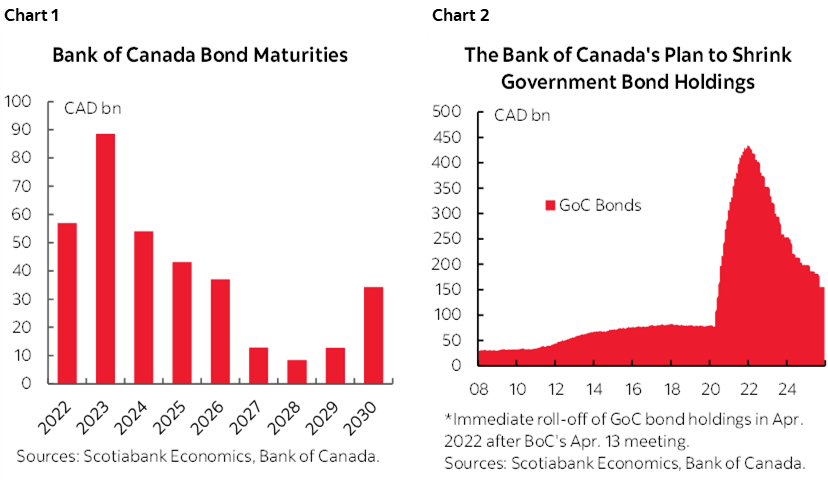

The BoC is also expected to end reinvestment of maturing Government of Canada bonds at this meeting. The maturity profile of its holdings by calendar year is shown in chart 1 and the flows are volatile and lumpy within each year. Chart 2 shows our estimation for how the holdings of GoC bonds will evolve. Governor Macklem’s speech on March 3rd (recap here) explicitly noted “When we initiate QT, we will stop purchasing Government of Canada bonds. From that point forward, maturing government bonds will not be replaced when they roll off the balance sheet.” This approach copied the RBNZ’s earlier abandonment of the reinvestment program but stopped short of the RBNZ’s guidance it would also consider managed sales. On timing such a move, a) Macklem has said they would wait to formally announce full-on QT until “at least” the first rate hike has been delivered as it was in March, and b) recall that the shift to end net purchases and embrace the reinvestment phase in October was set up by a speech in September and so there is likely to be a parallel here.

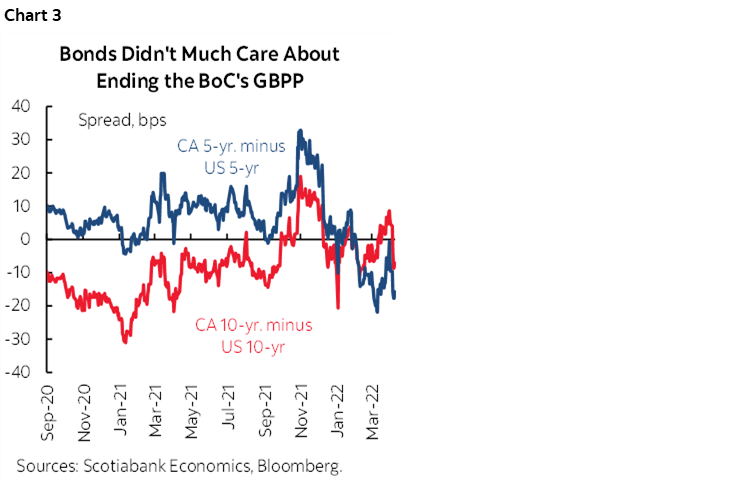

One thing to be careful toward is the possibility that Macklem will position an unwinding portfolio of Government of Canada bond holdings as having a rate equivalence effect to hiking the policy rate. It’s not impossible that he argues ending reinvestment now could afford him the opportunity to only hike by 25bps this time. I hope not. The balance of evidence as I see it does not support such an interpretation of the efficacy of the BoC’s purchase program. BoC staff research (here) estimates the announcement effect of the GBPP program at -10bps and the flow effect as small and highly transitory in that it fades away within a few trading days after each operation. We also know from chart 3 that as the BoC wound down its net purchases to zero between October 2020 and one year later while the Fed kept buying Treasuries and MBS by the boatload there was no obvious effect on Canada yields relative to the US. If the BoC’s QE purchase program was having an effect on Canada yields independent of other effects, then why did this period not impact Canada-US spreads?

All of this is not to say that pockets of the curve or some spread products may not have been impacted, but to a macrofinancial economist looking at the BoC’s QE program’s effects I find it hard to discern a significant effect independent of myriad other more important factors such as what the Fed is doing which has moved global bond markets fairly aggressively so far this year. The BoC’s first experiment with QE had merit in the beginning to address a serious liquidity shock to the financial system amid the risk of deflation and depression. Once globally coordinated stimulus worked through and vaccines along with shifting behaviour took over, the BoC’s QE program lost its usefulness relative to the Fed’s indirect effects upon Canadian yields.

In all, we’re left with a picture of a central bank that is increasingly pivoting toward an expedited pace of withdrawal of excess monetary stimulus. Half point or bigger hikes and no reinvestment is more like a head-for-the-hills approach than ‘gradual’ and ‘measured’ as their preferences used to guide. The latter approach would have been more likely had the BoC been more balanced in its views toward inflation risk and chipped away at stimulus in small steps earlier. It is now in an expedited rush to do so.

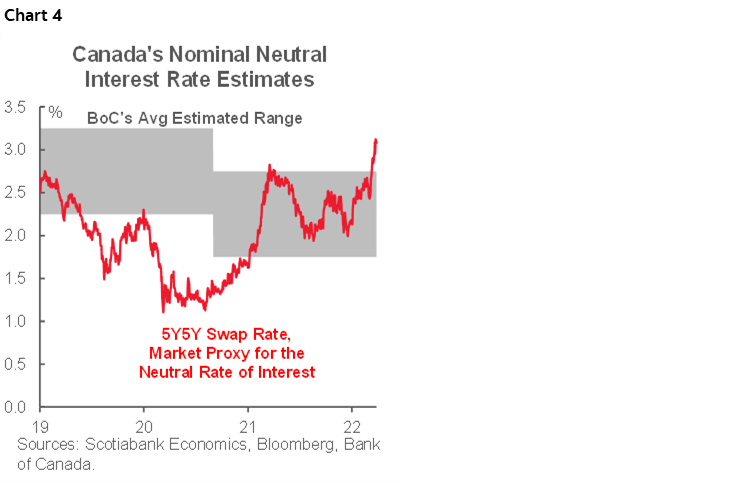

This is also the time of year when the BoC revises its estimates of the neutral policy rate. After lowering the estimated range by 50bps in research publishing in October 2020, the April 2021 MPR left it unchanged within a 1.75-2.75% zone. Market proxies are overshooting this range (chart 4). Personally, I find it would be futile to adjust it again now. The underlying drivers like productivity growth, labour force growth and influences on global neutral rates are not necessarily changing in unison and the neutral rate concept is a highly uncertain gauge in any event. I’d watch for a similar range and for Macklem to lack much conviction around the topic. It may be more fruitful to markets to broach the topic of whether the terminal rate will need to overshoot the neutral rate range in this cycle as we forecast with a 3% cap into early 2023.

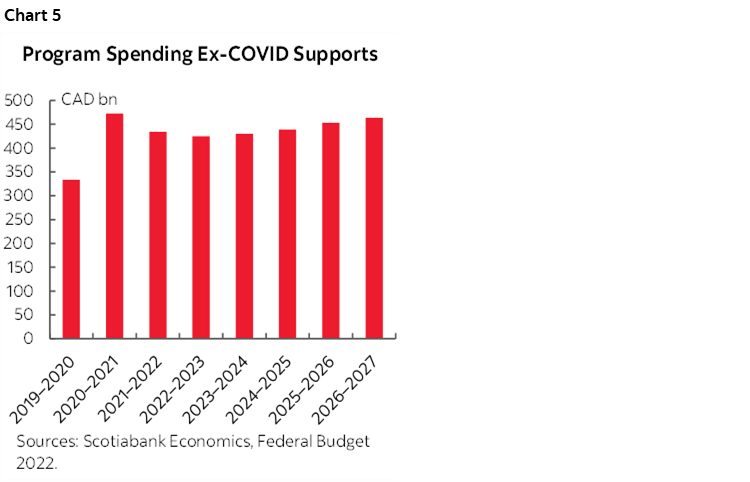

At the same time, the BoC would probably be wise to fade the Federal Budget. Deficits have improved because of positive revenue surprises but also perhaps because major platform commitments have been deferred (e.g., pharmacare). They may be deferred to give more time to develop programs, or because of uncertainties around the sixth wave and the war in Ukraine, or because more fiscal stimulus is being timed for later in the LNDP pact rather than peaking too early and having the BoC pounce more aggressively upon it. That should make the BoC leery toward future fiscal stimulus in the context of program spending excluding COVID supports that remains well above pre-pandemic levels and that will continue to rise in the years ahead even without further spending announcements (chart 5). It’s simply untrue to characterize Federal government spending as not being on a path marked by a twelve-figure upward adjustment each year compared to spending levels just before the pandemic and after excluding COVID supports! There is most definitely more spending to come yet as the size of government continues to grow.

US INFLATION—HELLO 1982

The CPI inflation reading for March (Tuesday) is likely to cross 8% y/y for the first time since January 1982. Using a bottom-up approach I’ve gone with 8 ¼% y/y and 1.2% m/m for headline CPI, while estimating core CPI at an unchanged 6.4% y/y and 0.3% m/m.

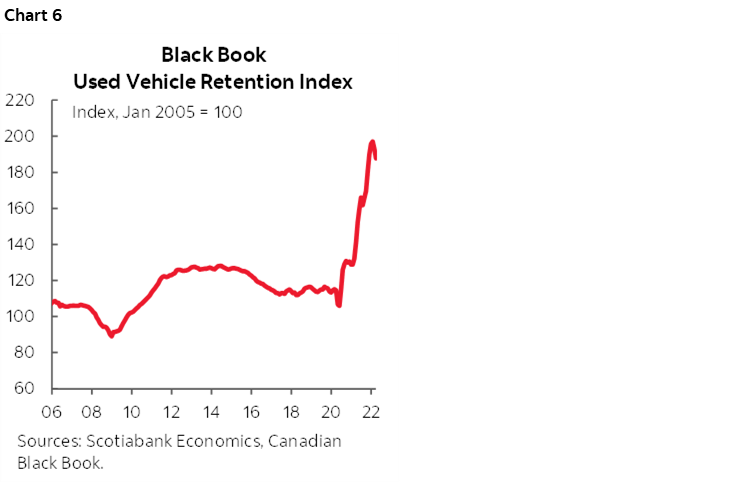

Base effects alone would cool the headline and core rates to 7.1% y/y and 6.0% y/y from 7.9% and 6.4% respectively. Gas prices soared and, given a weight of just under 4% in the basket, could wind up adding a weighted contribution in the vicinity of ¾% in m/m terms. Other fuel prices climbed, but the small weight in CPI should make for little weighted contribution. New and used vehicle prices both declined according to JD Power for new vehicles as well as a variety of sources for used vehicles including JD Power, Blackbook and the Manheim index (chart 6). Both used and new vehicles combined should shave around ¼% off m/m headline inflation. Higher food prices and continued effects from reopening, mobility and stringency assessments should drive guesstimated weighted contributions of 0.3-0.4% to headline and core CPI.

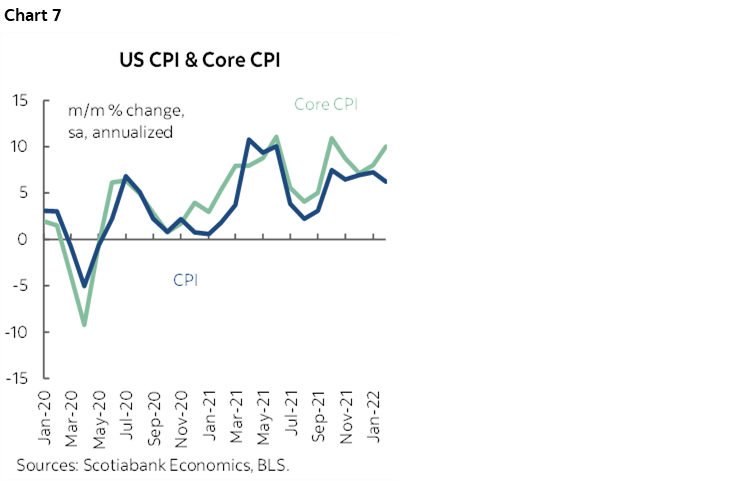

The US has entered the phase during which the focus needs to shift toward momentum in inflation readings defined in month-over-month, seasonally adjusted and annualized rates of inflation. Such a measure is free of year-ago base effects and will be as important to emphasize going forward as it was on the way up when assessing price pressures at the margin. So far, those pressures are accelerating (chart 7).

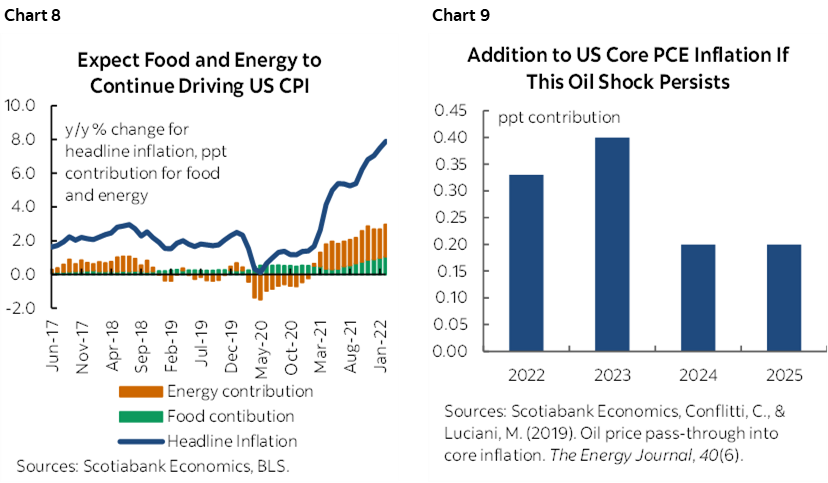

A significant uncertainty going forward is how much of the rise across a suite of commodity prices may be passed through the rest of the basket. Most of the inflation is derived from non-food-and-energy prices thus far (chart 8) and chart 9 shows one set of estimates for the impact of higher energy prices passed through core inflation.

CHINA’S CENTRAL BANK MAY CUT

Four other central banks will also make policy decisions over the coming week.

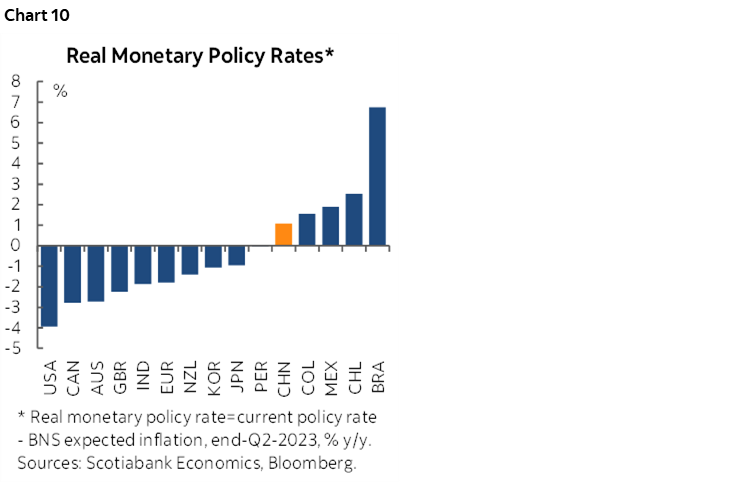

The People’s Bank of China is widely expected to cut its one-year Medium-Term Lending Facility Rate on Wednesday. This follows Premier Li’s remarks on how the economy faces greater uncertainties and that policy measures need to be increased. Even though inflation is expected to rise in this week’s estimates (see below), it will remain absurdly below the annual 3% target while China maintains among the world’s highest real policy rates (chart 10). China started to face downside risks with successive waves of COVID-19 hitting their export markets, then risks escalated in its property finance market before zero COVID domestic policies coincided with an imported commodity shock to growth. China long ago needed greater policy stimulus and has frankly been doing little to help world growth.

ECB—THE SCRIPT WAS ALREADY SET TO LAST INTO SUMMER

The European Central Bank (Thursday) won’t steal the thunder away from US CPI this time! They land on separate days unlike last month when a hawkish sounding ECB stomped all over global markets and left US inflation in the dust. Similar guidance is expected at this meeting with policy decisions deferred to a later date. Most of the pivot was done at the March meeting which buys them time to monitor conditions into the summer. Recall that at the March 10th meeting, the ECB did the following:

1. No More PEPP

The Pandemic Emergency Purchase Program ended in March as had been previously guided.

2. Other Purchases Were Tapered

Purchases under the Asset Purchase Program—that encompasses all other purchase programs of public sector, corporate sector, ABS and covered bond instruments—were unexpectedly tapered at a faster pace than previously guided and purchases are conditionally guided to end some time during Q3. Prior statement guidance was:

"monthly net purchases under the APP will amount to €40 billion in the second quarter of 2022 and €30 billion in the third quarter. From October onwards, the Governing Council will maintain net asset purchases under the APP at a monthly pace of €20 billion for as long as necessary to reinforce the accommodative impact of its policy rates. "

And was replaced by two references:

"Monthly net purchases under the APP will amount to €40 billion in April, €30 billion in May and €20 billion in June."

And

“If the incoming data support the expectation that the medium-term inflation outlook will not weaken even after the end of its net asset purchases, the Governing Council will conclude net purchases under the APP in the third quarter.”

Lagarde emphasized in the press conference that the conditional ending of the APP could occur at any time in Q3 from July though the September meeting.

3. Rate guidance

This changed in a subtle way that leaves all options on the table in terms of timing lift-off. The prior statement said that the APP would end “shortly” before raising rates and now the current statement says that raising rates could happen “some time” after ending APP purchases. What’s meant by “some time”? Lagarde did not reintroduce language around how a 2022 hike would be “very unlikely” that she had been saying before the hawkish pivot at the prior meeting. Instead, Lagarde said that "some time after is all encompassing" and "it could be the week after" or “it could be months after."

With that kind of guidance, markets will always price the earliest scenario which is probably that they end purchases as early as July and then hike as soon as at the next meeting in September. All options from that point forward are on the table conditional upon, well, just about everything from inflation tracking to growth tracking to further developments in the war in Ukraine and stability considerations.

4. Breadth of opinions

Lagarde was asked about how much agreement there was around accelerating the policy exits. She said that the discussion started off with widely divergent views around the table, but that all Governing Council members ultimately supported the decisions that emphasize optionality. She somewhat defensively noted that the decisions made today were not to accelerate normalization but rather to progress step-by-step and to acknowledge uncertainty and add optionalities in order to be able to respond in all circumstances in an agile way.

Overall, they sped up the APP taper, brought forward its conditional end and guided that hikes could commence as soon as right after. In all, that’s a hawkish set of messages and they were taken hawkishly by markets.

5. Forecasts

No further forecasts are expected for this meeting after issuing new ones in March. The ECB staff revised down GDP growth this year while revising up inflation forecasts for 2022 and leaving both variables’ forecasts little changed in subsequent years. Lagarde emphasized increased confidence that inflation expectations will durably converge upon the ECB’s 2% target which added to the general sense of hawkishness around the communications.

TWO MORE HIKERS!

The Reserve Bank of New Zealand probably gets the gold medal in central banking for proactively backing away from stimulus in the face of rising inflation risk. Most economists expect another 25bps hike on Tuesday with some expecting 50bps. That would make for at least 100bps of hikes since it started to tighten policy last October while too many other central banks either misread inflation and/or were too timid to begin pulling away the extreme amounts of monetary stimulus.

The Bank of Korea also chimes in at mid-week and consensus slightly tilts toward expecting a 25bps hike. This one will be a bit of a challenge in that the BoK presently lacks a Governor to steer the show as Rhee Chang-yong’s nomination will be put before Parliament afterward. Inflation is running at 4.1% y/y and rising but the awkward circumstances are contributing to some of the divided expectations.

Turkey’s central bank is expected to leave its one-week repo rate unchanged at 14% on Thursday.

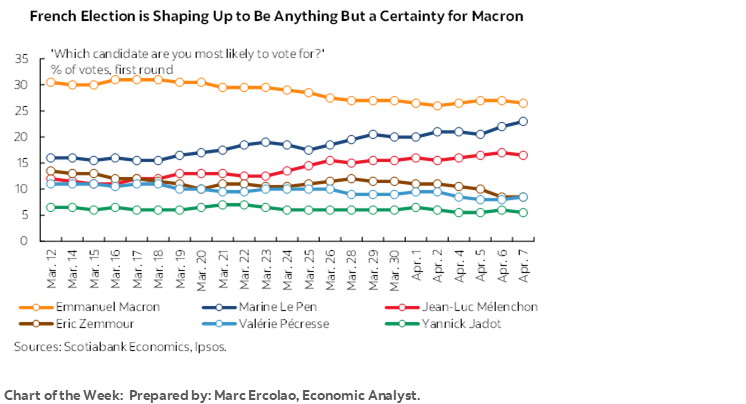

FRENCH ELECTION—NARROWING THE FIELD

France heads to the polls on Sunday April 10th for the first round of Presidential voting. Barring a very surprising first-round victory by one of the twelve candidates, the top two candidates will then face off in the second round two weeks later on Sunday April 24th.

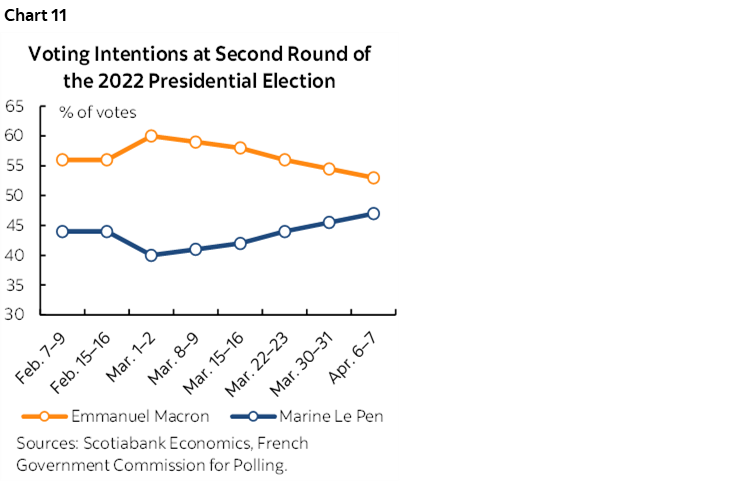

Polls are very tight as shown in this week’s cover chart. Chart 11 also shows that a second-round run-off between President Macron and Marine Le Pen—his main challenger—would result in a modest margin of victory for Macron. The Economist magazine gives Macron 98% odds of getting to the second round and 78% odds of winning it all.

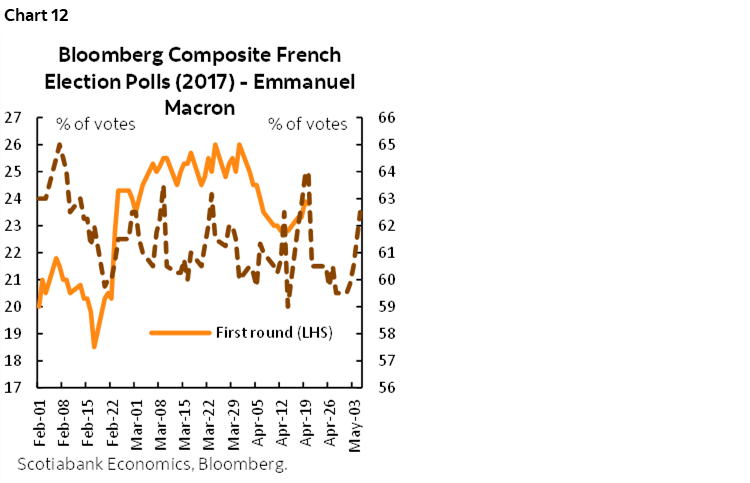

In a sense, France is used to this. The far right has been challenging in French Presidential elections for decades but has never pulled off victory in the end. Jean-Marie Le Pen—founder of the National Front, changed in name by his daughter to the National Rally—lost in the second round to President Chirac in 2002 and his daughter Marine lost to Macron in 2017. The 2017 election had some polling similarities to current results in that Macron’s support in first- and second-round polling was waning, yet he still pulled off a resounding victory over Marine Le Pen by about a two-to-one factor (chart 12). A major difference this time, however, is that Macron’s polling margin is much tighter and the consolidated right wing vote is much higher in that it accounts for about one-in-two French voters.

At stake are numerous domestic and international matters. Macron is widely noted to be the only candidate who is strongly pro-NATO. He is a centrist leader within a cross spectrum of extreme choices. Le Pen’s party is generally anti-immigrant and Europe is dealing with an immigration crisis. Le Pen has also previously cozied up to Russian President Putin but downplays this fact today. A victory by the far right could drive further concern about the rise of the right across other parts of Europe.

OTHER MACRO—INFLATION’S DAMAGE ESTIMATES

US bank Q1 earnings will be closely watched over the back half of the week when JP Morgan, BlackRock, Morgan Stanley, Goldman Sachs and Citigroup will be among the names releasing. Inflation will be the main focus on the economic release calendar with numerous other countries joining the US with updates, but regional job market figures and a few gems here and there are also due out.

CPI inflation will also be updated with March readings by China (this weekend), Norway (Monday), India (Tuesday), the UK (Wednesday), Argentina (Wednesday) and Sweden (Thursday). In all cases a synchronized upswing is likely to reflect similar forces to that which were discussed in the US CPI section but to sharply varying degrees. At least a half point is expected to be added to UK CPI from 6.2% y/y the prior month. China’s reliance upon imported oil and other commodities will likely raise inflation from just 0.9% y/y in February to around 1½%. Ditto for India’s import reliance, but CPI is starting at a much higher rate that is expected to rise toward 6 ½% y/y and further outside of the RBI’s target range. Countries like Norway are on the opposite side of the commodity effects with inflation expected to leapfrog toward 5% y/y (3.7% prior). Its Scandinavian neighbour—Sweden—is likely to see inflation jump by over a percentage point toward 5 ½%.

Canadian markets will be mostly focused upon the Bank of Canada in a shortened trading week given Good Friday ahead of Easter. Residual data risk will land on Thursday when manufacturing shipments are expected to rise by ~3.7% m/m and wholesale trade is forecast to rise by 1%, both based upon advance guidance from Statistics Canada for February readings.

US CPI will be the main event in US (and global) markets, but retail sales for March also land on Thursday. A gain of ½% m/m with sales ex-autos up 1% seems feasible. Vehicle sales fell by ~5% m/m in volume terms and there was a mild decline in new vehicle prices. Gasoline prices skyrocketed as an offset since retail sales are first released in nominal terms. A modest rise in sales ex-autos and gas is expected that accounts for about three-quarters of retail sales. Producer prices for March (Wednesday) will inform the magnitude of supply chain pressures before some of it may pass through to CPI. Industrial output (Friday), the UofM’s consumer sentiment measure (Friday) and weekly claims round out the main other releases.

A round of employment figures lands next week with UK and South Korean jobs leading on Tuesday followed by updates out of Australia on Wednesday.

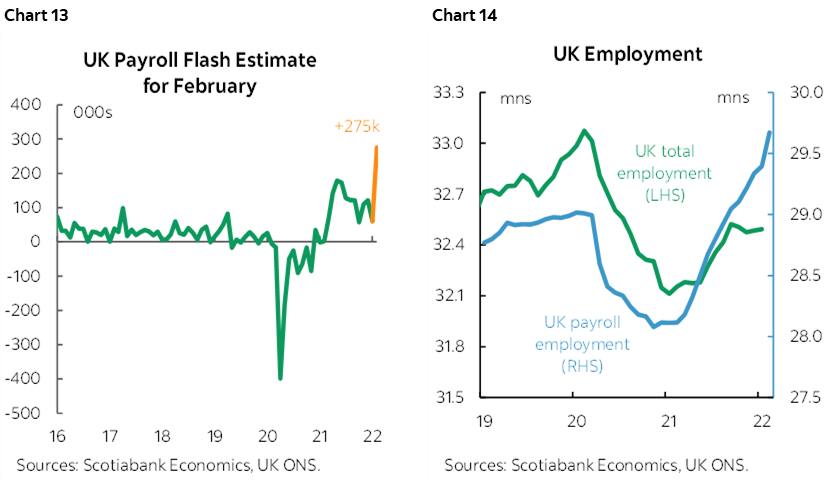

Flash UK payroll data published by the Office for National Statistics in advance of Labour Force Survey data pointed to a reading of +275k jobs in February (chart 13). Total employment has been lagging payroll employment in recent months (chart 14) but record high job vacancies are indicating a very tight labour market. Inflation, rather than job market data, is likely to be more of a factor in the BoE’s next rate decision, but strong job figures will likely add insurance to the consensus rate hike call for May.

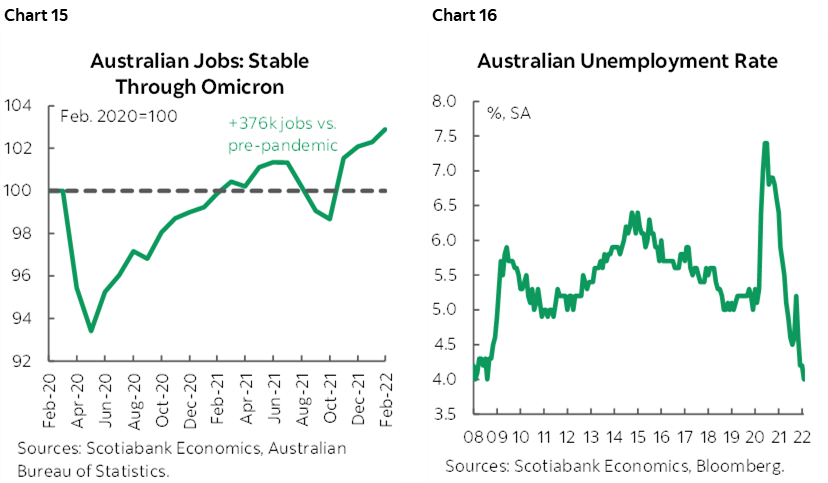

Australia’s job market is expected to keep chugging along, with an additional +30k jobs to be added to the +376k tally above pre-pandemic levels (chart 15). The unemployment rate currently sits at 4.0%, the lowest since early 2008 (chart 16), and may tick a tenth of a percent lower if employment growth can outpace strengthening participation numbers. Look for hours worked to extend its rebound from January’s hit.

South Korea’s labour market clocked the second largest monthly gain in February (+417k) alongside a sharp rise in the participation rate (chart 17). COVID cases in South Korea peaked in mid-March, later than their Western counterparts, so job figures could temporarily soften for the month—the unemployment rate is expected to tick back up to 3.0% from February’s 2.7%.

The UK also updates a stale round of monthly figures for February including industrial output, construction, a services index and trade figures. The Eurozone’s fresh round of monthly sentiment surveys kicks off with the ZEW investor-sentiment gauge on Tuesday. China will also likely release financing and credit figures, exports and producer prices.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.