- Weakness isn’t over, but a Springtime rebound is likely ahead

CDN nominal retail sales, m/m %, headline/ex-autos, SA, November:

Actual: 1.1 / 0.7

Scotia: 1.2 / na

Consensus: 1.2 / 1.2

Prior: 1.5 / 1.3 (revised from 1.6 / 1.3)

December ‘flash’: -2.1 / na

What consumers gave in November they took away in December, leaving the overall quarter roughly flat for retail sales volumes. The data should have zero bearing on next week’s Bank of Canada decisions.

Why? Because there are strong caveats that should prevent over-reacting.

- Inventories are very lean. Consumers can’t spend if they can’t get product. They may be deferring consumption amid robust indicators of household finances for when goods become more readily available. How robust? The debt service burden has fallen, cash stockpiles have risen, there is the massive gain in home equity, and we’re 240k above pre-pandemic employment amid evidence of accelerating wages.

- There was probably of rotation of the composition of spending more toward services at least over say the first two-thirds or so of December. More air travel and spending at restaurants probably contributed to this until omicron drove mobility readings lower. That’s not captured well—in some cases at all—within retail sales.

- The rise of omicron cases is viewed as a transitory shock. A bad one, but transitory such that our shop’s assumption is that as we will transition toward Springtime when we’ll have a higher level of antibody protection driven by cases and vaccines including boosters. Diminished cases and higher protection with relatively low average severity of outcomes compared to the Delta variant may lead to a pent-up rebound.

- StatsCan flagged flooding in BC with one-fifth of retailers in BC and the Atlantic provinces affected and 16% of retailers responding their operations were disrupted by transportation effects. Retail sales were nevertheless up 0.8% m/m in BC and higher in three-out-of-four Atlantic provinces, though we’ll wait to see the results for December. The disruptive effects, however, could reasonably have affected retail supply chains nationwide.

- Sales may have been brought forward to drive the strong start to Q4 when volumes were up by almost 1% m/m in October. Black Friday in October….

- and of course we had the early tightening of restrictions in Quebec in December that probably weighed on the -2.1% m/m flash guidance, though we’ll have to wait for details in the next report in order to assess the impact on a regional and sector basis.

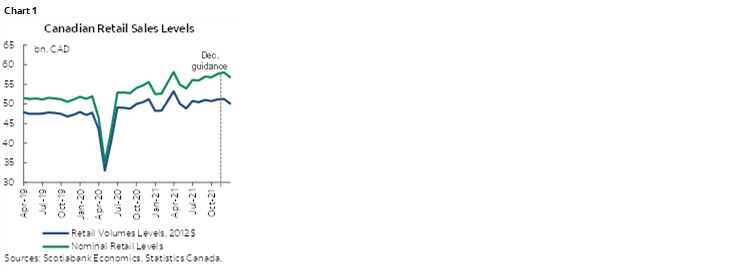

Chart 1 shows the tracking for monthly sales values and volumes over the pandemic.

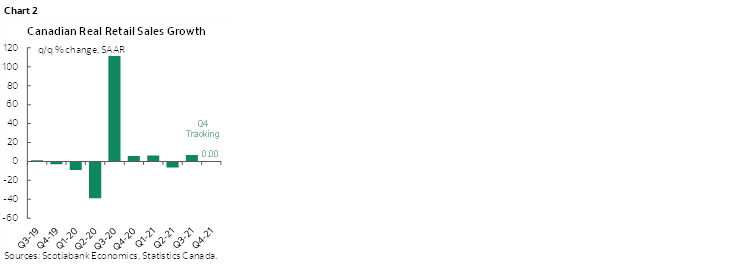

After a 6.9% q/q SAAR gain in retail volumes in Q3, Q4 is tracking up another 1.4% assuming all of December's flash guidance for nominal retail sales shows up as a decline in volumes. If vols fell even more (given higher prices) then I'd figure the quarter came in flat (chart 2).

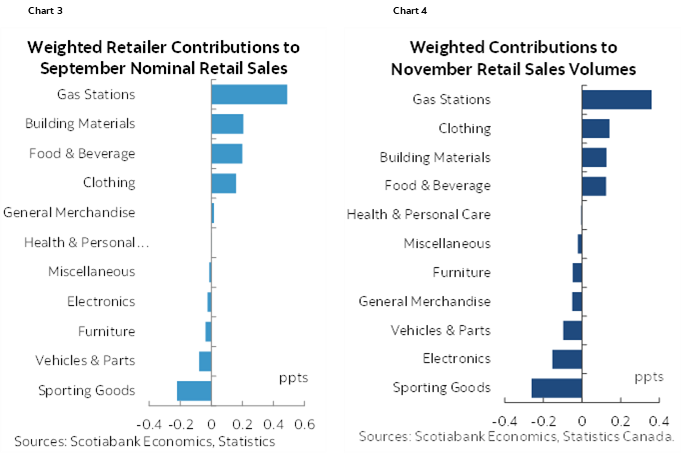

Charts 3–4 break down the composition of sales during November. December is unavailable.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.