Canada’s national net worth ticked up slightly in Q2 due to the recovery in global equity markets.

Household savings rate spikes to record 28.2%, while debt-service ratio and credit market debt to personal income fall by record amounts.

Record levels of government borrowing boosted household income, softening the economic shock to households.

NET WORTH EDGES UP IN Q2

Canada’s national net worth increased CAD 13.7 bn to CAD 12.7 tn in Q2, with increases in Canada’s net foreign asset position offsetting the decrease in national wealth (chart 1). Net foreign assets increased 17.0% to CAD 1.1 tn, mainly on the back of the rebound in global stock markets since a large proportion of assets are held in equities. National wealth on the other hand decreased 1.3% to CAD 11.6 tn due to the continued weakness in energy prices and draw down in inventories in the face of supply chain disruptions. Residential real estate partially mitigated these losses, increasing 1.4% for the quarter.

RECORD UPS & DOWNS

The Federal Government introduced new policy measures, while continuing or expanding on measures introduced at the end of the first quarter, designed to mitigate the economic impact of mandatory lockdowns instituted throughout most of Q2. As a result, household disposable income increased 10.8% despite the fact that employee compensation dropped significantly. This increase, coupled with a 13.7% decrease in household spending during the quarter, pushed the household savings rate to a record high of 28.2% in Q2 (chart 2).

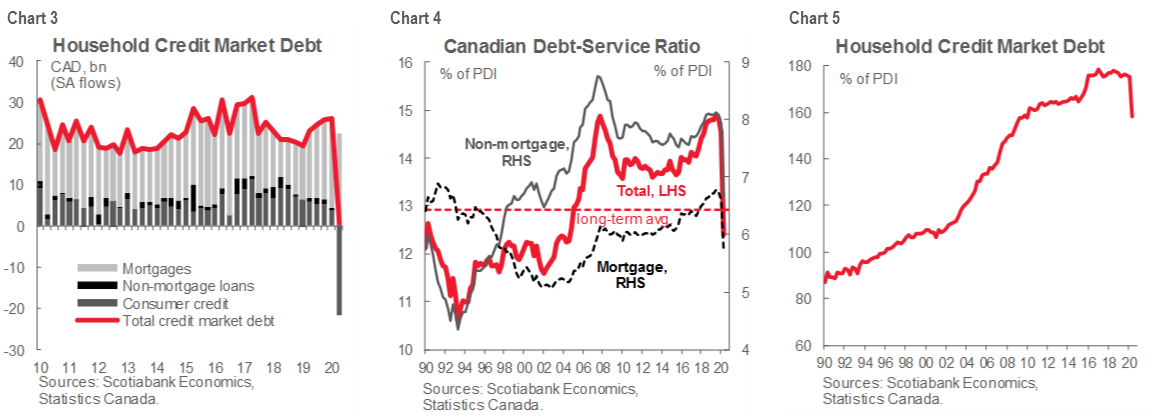

Credit market borrowing decreased to CAD 0.9 bn, with a drop in consumer credit and non-mortgage loan borrowing of CAD 21.5 bn only barely offset by CAD 22.3 bn in mortgage loans (chart 3). With the demand for new debt slowing, household income rising while spending decreased, and interest rates falling, the household debt-service ratio fell a record amount from 14.54% in Q1 to 12.40% in Q2 (chart 4). Also, since credit market debt hardly moved and personal income spiked, the ratio of household credit market debt to disposable income saw its greatest decrease on record, falling 175.4% to 158.2% for the quarter (chart 5).

The government stimulus implemented to help mitigate the economic shock of the pandemic resulted in record levels of net government borrowing, with funding raised mainly through the sale of government debt. This increase in government debt, coupled with the sharp contraction in economic output over the quarter, led to the largest quarterly increase in federal government net debt on record to 32.0% (chart 6).

Private non-financial corporations saw a modest improvement in their balance sheets as a result of the equity market recovery over the quarter. The increase in stock prices outpaced the increase in debt, resulting in the debt-to-equity ratio falling from a decade high level of 213.2% to 199.7% (chart 7).

As we move into Q3, we should see a further improvement in financial assets as global equity markets continued to improve over the summer (provided the recent pullback begins to reverse), and some normalization to take place in these numbers. However, as the specter of a second wave continues to loom in the Fall and no vaccine available yet for mass distribution, these records could potentially prove to be short-lived.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.