- USD sinks as Trump tweets about delaying the election

- Initial jobless claims rise for a second week

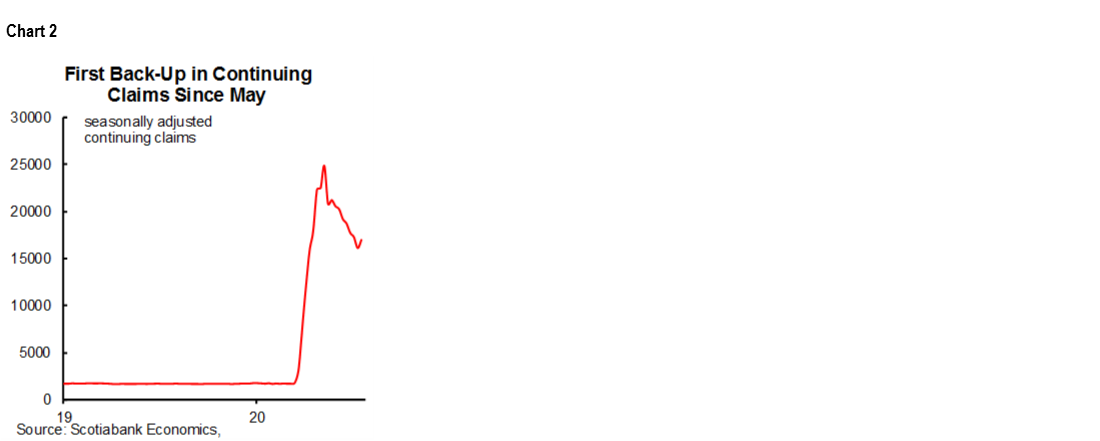

- Continuing jobless claims rise for the first time since May

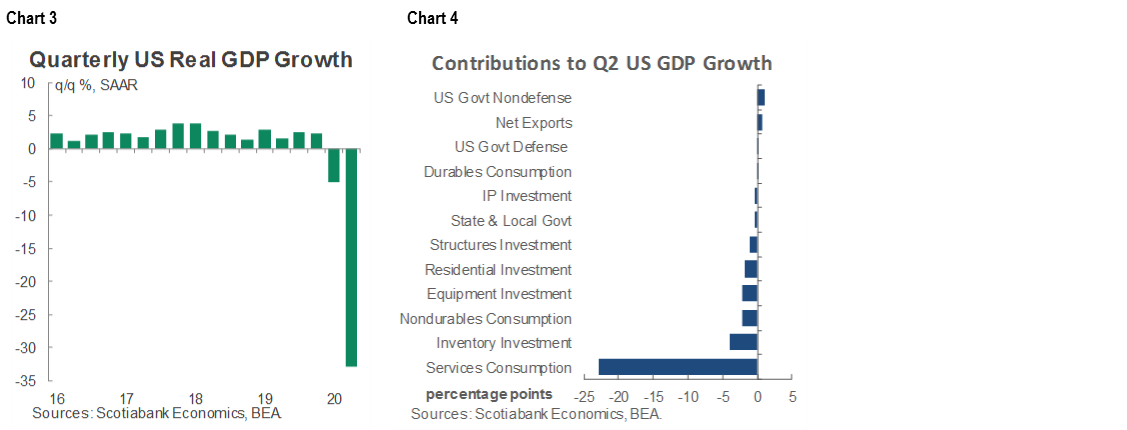

- US Q2 GDP sinks in line with expectations

- Sell US on political dysfunction, stalled stimulus & souring jobs…

- ...or buy on the hope that rising claims focus the minds?

US Q2 GDP, q/q SAAR %:

Actual: -32.9

Scotia: -36

Consensus: -34.5

Prior: -5

US weekly initial (July 24th)/continuing (July 18th) claims, 000s:

Actual: 1434 / 17018

Scotia: 1400 / na

Consensus: 1445 / 16200

Prior: 1422 / 16151 (revised from 1416 / 16197)

What a coincidence. Shortly after seeing the GDP and claims numbers and thinking about a souring economy into the election, President Trump tweeted that the election should be delayed because of the risks that people would be taking if they had to vote during the pandemic. Going back to school and reopening everything is ok, but voting would be wayyyy too dicey... I guess they were a tougher breed that still voted in the 1918 midterms!

What he saw was indeed disturbing, but not particularly impactful to markets—until his tweet hit and brought equity futures a bit lower as it obviously foments concern he won’t give up the title easily even if defeated. That risks political dysfunction of a shape and magnitude never before seen in the US. Hence the drop in the USD immediately after his tweet in that political dysfunction, stalled fiscal stimulus and a souring labour market lend serious consideration to a much greater degree of caution toward US assets. Each of these risks feed off of one another in that the tweet doesn’t help the tone of the fiscal dialogue with stimulus extensions of vital important to the job market.

Weekly initial jobless claims increased by 12k from an upwardly revised prior week estimate for a combined increased of 18k (chart 1).

Continuing claims registered the first jump in the extended duration of jobless benefits since the first week of May (chart 2). More initial claims and staying on earlier claims for longer is a double negative.

While two weeks of higher initial claims, an up-tick in the lagging duration of unemployment and expired $600/week benefits are less than ideal, the silver lining could be the possibility that a souring job market focuses the minds in Washington!

The GDP hit was in line with expectations and backward looking to forward looking markets. The dual rise in initial and continuing claims adds to concern that the US job market is slowing even if we don’t see that in next Friday’s nonfarm payrolls versus risk into August payrolls.

The GDP drop is shown in chart 3. Chart 4 shows the weighted contributions to growth by GDP component. The dominant role played by services consumption a) in an economy dominated by the service sector, and b) given the concentrated social distancing effect on services after the lockdown should surprise no one.

- Consumption dragged 25 percentage points off GDP;

- Investment knocked another 9.4 points off;

- Inventories subtracted 4 points;

- Exports dragged 9.4 points off GDP;

- Imports added 10 points (less import leakage effect with lower imports)

- Government spending added just 0.8 ppts as the Feds added 1.2 but challenges across states/locals knocked 0.4 ppts off GDP. This too could help focus the minds on the troubles facing state and local governments and how they are working against recovery.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.