CANADA

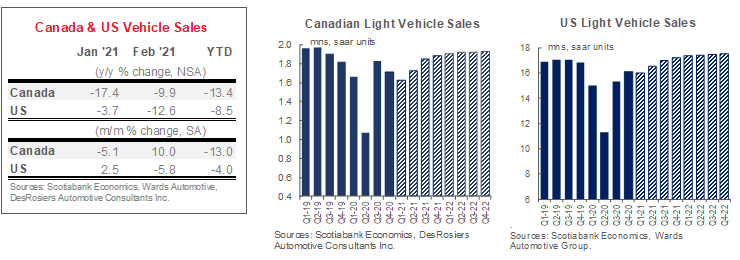

Canadian auto sales picked up in February relative to last month’s weak performance, but were still down relative to last February. DesRosiers Automotive Consultants Inc. estimates that new vehicle sales declined by 9.9% y/y. On a seasonally adjusted basis, sales posted a hefty improvement of 10% m/m over January’s slow start to the year. While broad-based lockdowns across the country were being lifted by late January, some major markets including the Greater Toronto Area—representing a fifth of Canadian output—remained under tight restrictions for the full month of February. Meanwhile, the global chip shortage likely depressed already-tight inventories, with Wards Automotive forecasting a consequential 10% contraction in North American vehicle production in the first quarter. This will likely weigh on auto sales over the next couple of months as the imbalance is unwound, while also placing continued upward pressure on prices. Despite depressed new vehicle sales in January on a unit basis (-3% y/y), new vehicle price inflation continued its upward trend to 2.8% y/y against headline inflation of 1.0% in January. Meanwhile, a resilient economic recovery supported by elevated household savings and extended employment benefits (not to mention vaccines on the horizon) should further underpin new vehicle demand—albeit pent-up demand—until supply constraints are resolved. This could erode new vehicle sales by 5–10% over the next few months and represents a material risk to our 2021 sales outlook—forecast at 1.8 mn units—should serious shortages persist well-into the second quarter. We had already built into our forecast some dampening in Q1 sales activity owing to pandemic restrictions which should offset a transitory impact of the parts-shortage, while a stronger-than-anticipated economic outlook for 2021 should support a more robust rebound in the latter part of the year.

UNITED STATES

US auto sales slowed in February with a 5.8 % m/m (sa) decline as inventory shortages and weather events temporarily disrupted the sector’s recovery. The year-over-year unadjusted decline (at -12.6%) was padded by an extra sales weekend this year, while the seasonally adjusted sales rate sat at just 15.7 mn units. American consumers were primed to continue unwinding the USD164 bn in stimulus cheques that had arrived in January, propelling retail spending up by 5.4% m/m (sa) in January, well-above consensus forecasts. But severe weather events across large swathes of the country kept many consumers home (and some dealerships closed) mid-month including in Texas, the second largest auto sales market. The chip shortage also further exacerbated tight inventory, with Wards Automotive estimating days’ supply at 57 days versus a five-year February average of 73 days. This supply constraint is expected to continue dampening auto sales over the next few months at least, as data from World Semiconductor Trade Statistics suggests automakers only ‘right-sized’ orders by late summer against a six-month production lag. Meanwhile, a stronger economic recovery—and robust household consumption in particular—will fuel further new vehicle sales demand as the year advances including through another round of stimulus cheques in April. We maintain our 2021 outlook at 16.7 mn units while acknowledging the chip shortage introduces a risk that demand is pushed out to 2022 the longer the shortage persists.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.