Brazil: December IPCA inflation blasted past expectations

Chile: The race to build the Constitutional Assembly begins; renewed measures to contain the spread of COVID-19

Mexico: October sent mixed signals on the domestic recovery

Peru: December tax revenue is a hopeful sign of the strength of the rebound

BRAZIL: DECEMBER IPCA INFLATION BLASTED PAST EXPECTATIONS

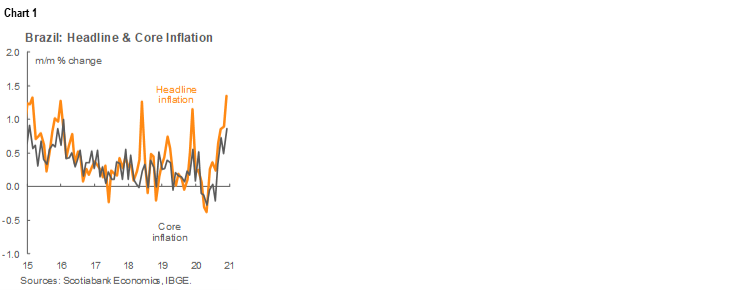

Brazil’s IPCA inflation reading for December blasted past consensus expectations with a print of 1.35% m/m (chart 1), up from 0.89% m/m in November and above Bloomberg’s survey of 1.21% m/m. Both goods and services prices drove the overshoot.

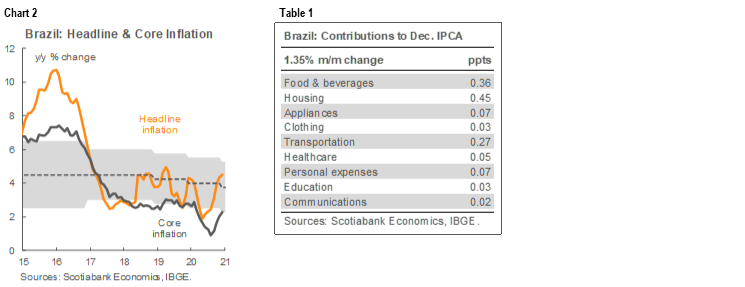

The sequential monthly numbers translated into annual inflation of 4.52% y/y (chart 2), an acceleration from November’s 4.31% y/y and above the consensus’ 4.37% y/y projection. As has been the case in recent months, the main culprit was food and beverage inflation (14.1% y/y), but consumer non-durables remain the biggest driver of price increases in the goods basket (table 1).

As we argued in our January 12 Latam Daily, the end of COVID-19 related consumer stimulus this month could help put a partial brake on inflation by dampening demand a bit. However, we also think that the BCB should get ahead of inflation by taking a more hawkish stance that would reduce the risk that indexation effects could trigger an inflationary spiral. In past inflationary cycles, when the BCB has chased inflation rather than being proactive, the deterioration in price stability has been material.

—Eduardo Suárez

CHILE: THE RACE TO BUILD THE CONSTITUTIONAL ASSEMBLY BEGINS; RENEWED MEASURES TO CONTAIN THE SPREAD OF COVID-19

I. More than 3,500 people will run for the 155 seats of the Constitutional Assembly

On Monday, January 11, the deadline to register the candidates for the four elections to be held on April 11 expired: mayors, municipal councillors, regional governors and convention constituents. According to Servel (i.e., the Chilean electoral agency) more than 3,500 people qualified to register their candidacy for the 155 seats of the body that will draft the new constitution, of which 2,213 are independent and almost 200 are representatives of native peoples who have been guaranteed 17 of the convention’s seats.

All candidates will now have to go through a process of acceptance or rejection of their applications, which will take ten days in the case of the Constitutional Assembly and 12 for the other elections. In total, there are 155 seats up for election in the Constitutional Assembly, 16 for governors, 345 for mayors, and 2,252 for municipal councillors. Likewise, Servel also ratified the audited electoral roll, which numbers 14,900,089 people who will be able to participate in the elections, comprised of 7,642,418 women and 7,257,671 men. Of that total, there will be 414,915 foreigners authorized to vote.

While the Opposition ended up divided into four lists for the Constitutional Assembly vote—which could split their support and favour the performance of the center-right, as they have admitted—Chile Vamos (the government’s coalition) and the Republican Party (the far-right party) signed on to a single pact. This situation could prevent the Opposition from controlling two-thirds of the seats in the Assembly, which could stymie agreement on new constitutional articles as those parts of society that voted “no” in the constitutional referendum last October may be over-represented.

Consequently, we continue to expect that the composition of the Assembly shouldn’t be very different from the current make-up of Congress which, combined with the requirement of a two-thirds majority to approve any article, should leave little room for extreme positions to prevail. However, as we have previously noted, strong debates will occur around sensitive topics such as the guarantee of social rights, particularly health and education; the role of the state in the provision of pensions; the independence and autonomy of the central bank, which we do not see being modified; property rights, especially water rights; minority issues; and the system of government.

II. COVID-19 cases continue rising, prompting new measures to contain it

From Thursday January 7, almost a quarter of the total population has been subject to strict movement restrictions. Faced with a sharp increase in COVID-19 cases registered in recent weeks—between 3,000 and 4,000 new cases a day, the government is implementing changes in its plan that regulates the mobility of citizens with the aim of reducing cases and avoiding a crash of the healthcare system.

Despite these new restrictions, for now we are not changing our forecast of a GDP expansion of 6% y/y in 2021. Our baseline scenario for this year already had a slowdown in activity in the first quarter caused by a second wave of infections that would bring stricter restrictions on mobility—which is indeed what is materializing. Eventual adjustments to our forecasts will be forthcoming only after we have the first monthly GDP print for 2021 in early March.

This is in a context where the latest economic data we do have—November’s GDP proxy, which was released on January 4—showed a 0.3% y/y expansion (chart 3) that was consistent with our baseline scenario, but which still implied a material output gap that will not be closed easily or quickly.

In the details, services expanded 1.9% m/m in November after a fall of -3.3% m/m in October. Given that many services are linked to investment, the partial re-opening of the economy during November could have brought some recovery in capital spending. But the re-imposition of isolation measures during December and January will negatively affect this sector again.

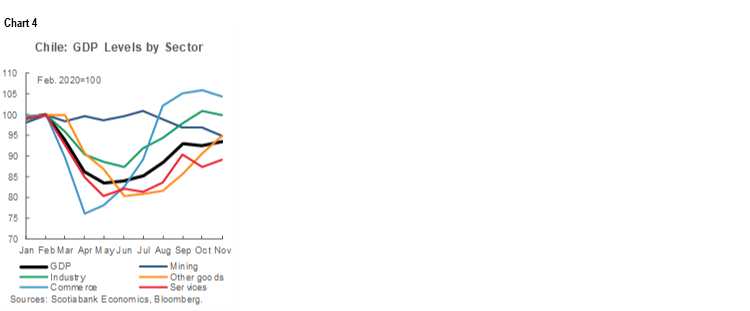

COVID-19 containment efforts together with slow execution of investment spending could be becoming the main obstacle to progress in closing Chile’s output gaps. As long as investment does not recover in a solid and sustained manner, services is likely to continue to be the sector that will show the largest gap compared to pre-COVID-19 levels (chart 4).

—Carlos Muñoz

MEXICO: OCTOBER SENT MIXED SIGNALS ON THE DOMESTIC RECOVERY

I. Private consumption growth moderated its pace in October, suggesting persistent weakness in domestic demand

According to data released by INEGI on December 12, private domestic consumption growth moderated its pace from 2.2% m/m sa in September to 1.1% m/m sa in October. This confirmed a weak trend in the domestic demand recovery, as we anticipated.

October’s deceleration in consumption growth knocked back its annual comparison for the first time since June.

- Real private consumption growth in the domestic market retreated from -9.8% y/y in September to -10.3% y/y in October (versus 1.4% y/y in October 2019, chart 5), the largest contraction for any October since at least 1994.

- By components, annual services growth pulled back from -14.0% y/y in September to -14.5% y/y in October (versus 0.6% y/y a year earlier); annual growth in the consumption of domestic goods improved from -2.8% y/y to -1.9% y/y (versus 0.5% y/y a year earlier), but annual growth in imported goods consumption declined from -18.9% y/y to -24.2% y/y (versus 7.4% y/y in October 2019).

- The cumulative rate for January–October was -11.9% y/y YTD (versus 1.0% y/y YTD for the same period in 2019), another record low since at least 1994.

We maintain our view that domestic private consumption is likely to remain cautious through 2021, driven by a highly uncertain economic environment, intensified pandemic-related restrictions, and weak labour-market expectations.

II. Gross fixed investment growth picked up in October, but remained soft

Sequential monthly growth in gross fixed investment rose from -2.6% m/m sa in September to 2.8% m/m sa in October, in data published by INEGI on December 12.

This brought annual growth in capital spending up from -16.0% y/y in September to -14.7% y/y in October (chart 6), a bit softer than the Bloomberg consensus expectation of -13.7% y/y. This made for 25 months of annual contractions over the last 27 months, with year-on-year YTD growth at -19.5% the poorest since 1995 for January–October.

Looking at the details:

- The investment in machinery and equipment deepened its annual decline from -12.7% y/y in September to -17.0% y/y in October. Both its components, spending on national and imported machinery and equipment, respectively saw bigger annual declines: from -17.9% y/y in September to -18.3% y/y in October for domestic M&E, and from -8.8% y/y in September to -16.1% y/y in October for imported M&E; and

- In contrast, construction spending growth moderated its fall, from -18.4% y/y to -12.7% y/y, with its residential sub-index going from -14.3% y/y to -5.5% y/y and the non-residential side moving from -22.2% y/y to -19.6% y/y.

Waning progress in bringing investment back to 2019 levels remains a major risk to the upturn in real GDP growth we expect in 2021.

—Miguel Saldaña

PERU: DECEMBER TAX REVENUE IS A HOPEFUL SIGN OF THE STRENGTH OF THE REBOUND

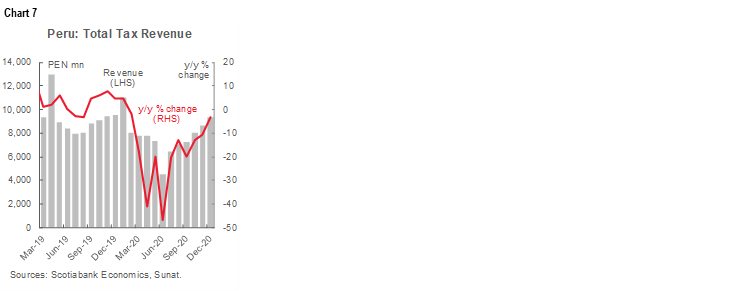

Total monthly tax revenue was down -3.1% y/y, in December (chart 7). This was the smallest gap compared with a year ago since February’s print. Tax revenue was up 9.0% in month-on-month terms from November. This was the sixth consecutive month-on-month increase since the series’ low point in June in the midst of the economic lockdown. As a result of the good December figures, tax revenue growth for full-year 2020 came in at -17.4% y/y, which was moderately better than the -20% y/y we had been forecasting. This is a ratification of the overall theme of an economy that has been recovering better than expected from 2020’s efforts to control the pandemic.

The theme of beating expectations is fortified further by the sales tax revenue results for December: the IGV sales tax rose 5.1% y/y in December, which put it firmly above pre-COVID-19 levels (chart 8). This, of course, reflected sales strength and, thus, underlying firmness in consumer spending. However, the headline number probably overstates the case a bit, as robust sales-tax revenue also reflected the increased formalization of sales due to digitalization. Social distancing has accelerated the move to online sales that are much more difficult to hide from taxes than in-person cash transactions. For full-year 2020, sales tax revenue contracted a relatively mild -5.8%.

Overall, December’s results suggest that annual tax revenue growth will be positive as early as January, and remain above last-year’s levels throughout 2021.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.