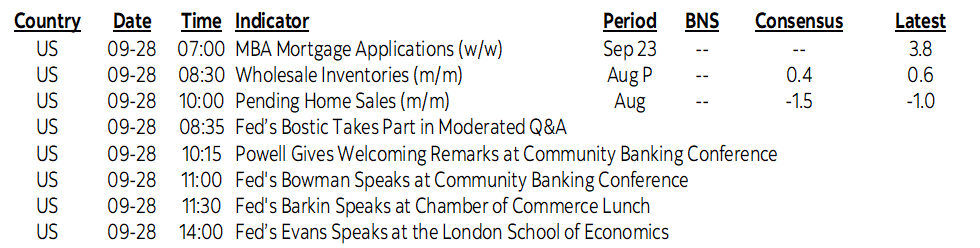

ON DECK FOR WEDNESDAY, SEPTEMBER 28

KEY POINTS:

- The BoE was in a tough spot…

- ...but may have further compromised the credibility of bond purchase programs

- BoE pivots on gilt purchases…

- …signalling a limit to allowing markets to respond to reckless fiscal policy…

- …by announcing temporary purchases of long-dated gilts…

- …and delaying the sale of gilts until Halloween…

- …while standing by gilt reduction targets…

- …and on course to accelerate rate hikes

- BoT hikes 25bps, baht slips as markets leaned toward more

- Fed-speak on tap, plus pending homes, trade and inventories

- BoC’s (lack of) transparency to be a focal point today

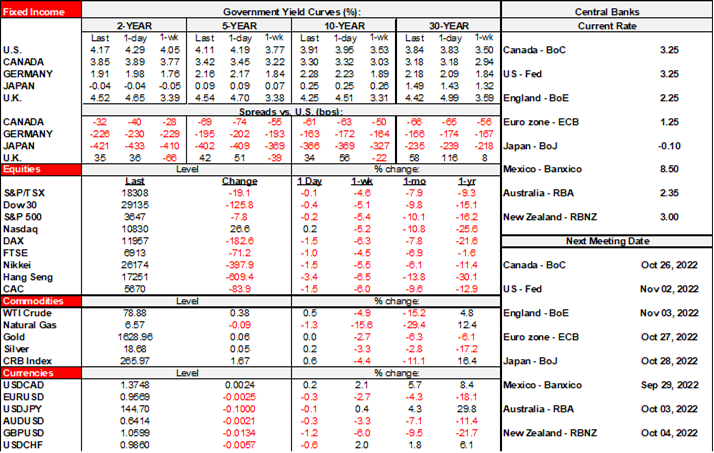

That central banks will tolerate perceived dysfunction in bond markets only to a point even when it is derived from fiscally irresponsible actions is the message that is resonating across fixed income markets this morning. The Bank of England is leading the move after its altered stance toward the sell-off in gilts but the effects are trickling across into other curves with US Treasuries also benefiting on the carry. What is notable, however, is that Canada is underperforming Treasuries again this morning. In fact, the Canada 10s spread to the US has narrowed by about 10bps from Monday’s wides.

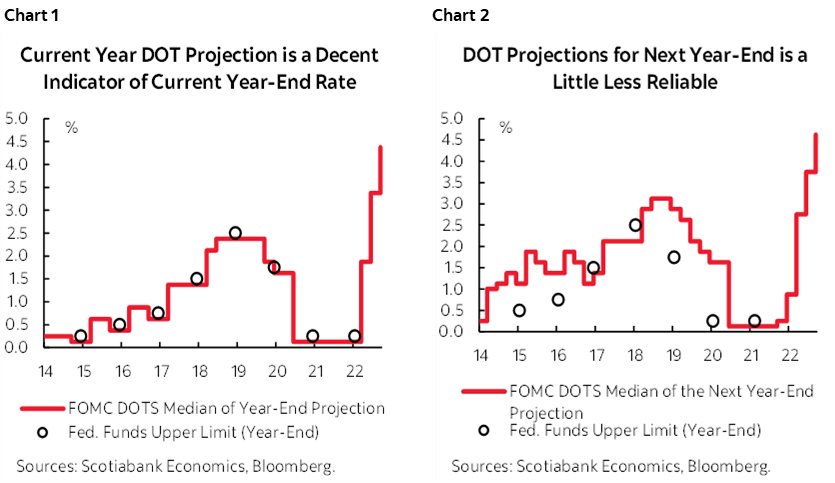

As a result, the response in UK markets (see below) also drove US Treasury yields about 5–6bps lower in 2s into what was already a richening market and 8–9bps lower in 10s. There was a minor move lower in Fed funds pricing for the November rate move, though as chart 1 shows, what the FOMC’s in-year dots guide for the year-end policy rate is typically very close to reality especially this late into the year even if chart 2 shows the next year’s guidance to be rather shaky. Stocks reacted in mildly positive fashion including in snp futures but are still broadly in the red. Safe haven crosses nevertheless continue to gain with the USD, Swiss franc and yen firmer against other major crosses.

After saying yesterday that a ‘significant monetary policy response’ to the UK government’s fiscal largesse would be delivered at the November meeting, the BoE jumped into gilts with a statement (here) expressing concern about market dysfunction as opposed to fundamentally altering its course on monetary policy. They announced temporary purchases of long-dated UK government bonds commencing immediately “to restore orderly market conditions” and at “whatever scale is necessary to effect this outcome” on “a strictly time limited” basis. The statement emphasized that the purchases are to “tackle a specific problem in the long-dated government bond market” with auctions from today until October 14th and with a plan to unwind them once risks to market-functioning have subsided. The sale of gilts has been postponed until October 31st instead of next week but the £80B annual targeted reduction remains unchanged.

The moves prompted a strong bull flattener as the 30-year gilt yield plunged 77bps and counting while the 2s yield fell 14bps. Sterling shook it off on the continued expectation for monetary tightening.

I can see the concern around the potential for collateral calls that were coming due and that could have created much greater havoc in the gilts market. The BoE was in a tough spot here in that it is principally responsible for maintaining smooth market functioning. But the trade off is that I can also see a strong case for concern based upon two main reasons.

- First, calendar-based guidance around purchase plans may prove to be dicey in that come the 14th and the 31st I’m just not sure how the BoE extricates itself from this mess. Will it succeed in calming markets even when it stops? Will markets perceive there to be a credible threat that if they push it too far once the dates come and go then the BoE will return once more? Or will the BoE be dragged into extensions and postponements in serial fashion? I guess we’ll just have to see what ghouls and goblins surface (sorry…no I couldn’t resist) around such calendar-based purchase guidance and how durable it proves to be.

- Secondly, I don’t like the signal that the BoE’s gilts purchase program is malleable in the face of a fiscal policy shock that amounts to nearly a quarter trillion pounds of tax expenditures and energy relief. £160B of tax expenditures plus £60B of energy relief that isn’t even fully costed plus a signal that fiscal anchors may be weakened or abandoned should be met by dysfunction. There should be a wicked response across the gilts curve. There should be tighter monetary policy including through purchase programs in response to such recklessness in what is thus far a Truss administration that is making Boris Johnson look good. The onus should have been on the government to temper its plans or reverse course and possibly respond to rumours that a new Chancellor of the Exchequer would be a symbolic move. Instead, the BoE is cleaning up the mess. It’s not the job of a central bank to come to the rescue of incompetent fiscal stewardship. I’m sure there will be spirited debate over the merits of this move that also considers the sharp sell-off in 30s from 3½% to crossing 5% before the intervention and the evidence of market dysfunction through sundry measures and whether that had merit or required today’s moves. Time will tell and maybe it is just a transitory set of measures, but the BoE had better prove it.

Otherwise, there is very light calendar-based risk that will principally focus upon Fed-speak. Powell just delivers welcoming remarks at 10:10amET but the Fed’s Bostic (8:35amET), Bullard (10:10amET), Bowman (11amET), Barkin (11:30amET) and Evans (2pmET) also speak. The A$ shook off Aussie retail sales that were up 0.6% m/m (consensus 0.4%). The Bank of Thailand hiked by 25bps as expected by most but there had been speculation toward a 50bps hike that when not delivered resulted in a weaker baht. The US updates pending home sales for August (10amET), advance merchandise trade figures for August (8:30amET) and inventory figures (8:30amET). On the latter, just-in-time is just going as industries will probably be tolerating higher inventory to sales ratios than in past cycles given the disruptive effects of sundry forms of border frictions to their supply chains.

This won’t impact markets, but the IMF releases its review of the BoC’s transparency practices and the BoC will issue its response at 10amET. I’m hoping the IMF applies pressure in favour of greater transparency with tangible steps. We’ll see what the exchange brings forward. My opinion remains that the BoC should be taking further steps toward greater transparency more in keeping with standards elsewhere. Bring in more outsiders and give them some powers, like the BoE and RBNZ. Publish minutes. Open up much freer dialogue across Governing Council members. Publish useful meeting minutes. In short, was it mainly the Governor who believed what he was saying about monetary policy focusing upon fully inclusive employment while entirely ignoring the warning signs on inflation throughout last year or did anyone else on GC actually challenge this thinking that resulted in policy error?

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.