ON DECK FOR FRIDAY, SEPTEMBER 23

KEY POINTS:

- Fed policy implications ripple through world markets…

- …as the market perils of reckless fiscal plans are on display in the UK

- What the Truss government did and why it mattered to markets

- Italy’s weekend election is the next potential risk to global fiscal policy

- Yen intervention worked for a single day…

- …as the yuan continues to tumble

- UK and Eurozone PMIs weaken…

- …as Australia’s indicate ongoing mild growth

- Weak Canadian retail sales probably reflect rotation to services spending

- US PMIs on tap

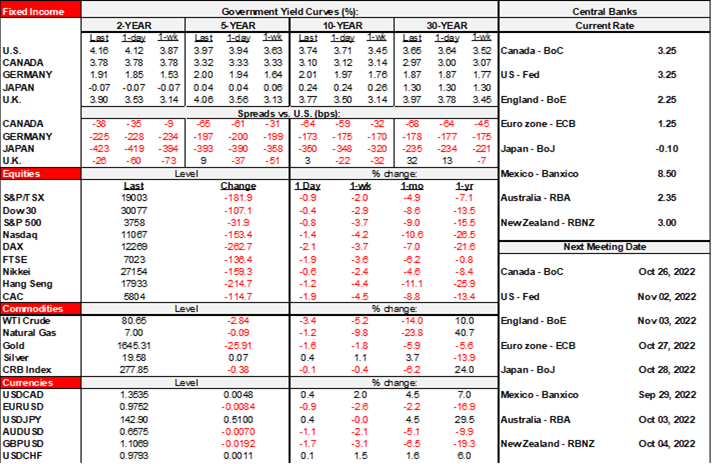

Fed policy implications continue to ripple through world markets while governments the world over are witnessing in real time the perils of irresponsibly attempting tone deaf pump-priming into a world concerned about inflation and higher borrowing costs. Gilts are by far the worst performers in a sovereign debt world that is seeing higher yields everywhere. The USD is attracting safe haven flows and gaining against all majors but with CAD outperforming most others. The yuan moved sharply lower overnight and with each move lower the fears of domestic market instability are rising given the impact upon Chinese savers. Yen intervention worked for a whopping single day as the currency is weakening again; it’s futile without coordination in a world that has no appetite for coordination. US equity futures are down by over 1% with TSX futures performing likewise. European cash equities are over 2% lower after Asian exchanges were a sea of red overnight. Oil is off by almost $3/barrel.

Gilts are blowing up this morning with the two-year yield up 40bps, 5s up 49bps and the long end up 20. The free-spending and debt-issuing Truss government is to blame and markets are interpreting her administration’s moves will add to a glut of gilts slamming the market while raising inflationary pressures and bringing forth additional monetary policy tightening. Hence, markets are sterilizing the moves and expecting the BoE to do likewise. Higher issuance needs just as the BoE will begin actively selling gilts early next month are front and center as the Truss government’s combined energy plans and deficit-financed tax cuts get digested by markets. More debt issuance will need to be bought by private market participants in a QT world and they are signalling willingness to do so only at a higher rate of return.

So what did they do and why are markets concerned?

1. Chancellor of the Exchequer Kwarteng’s package of tax cuts is estimated to cost £161 billion of foregone revenues over the next five years which sees the tax expenditures rise to £45 billion five years out. See chart 1. The full plan is available here and in particular note table 4.2 that breaks down the costing of the individual initiatives.

2. In order to fund this, the Treasury will have to issue a lot more debt. Treasury advised that an extra £72 billion will have to be issued just for this current fiscal year which takes the year’s tally to a whopping £234B.

3. The government’s costing estimates for the energy plan only extend six months out given uncertainties and are pegged at £60 billion. The government’s guidance on the “highly uncertain” costs of the energy plan amid no effort to even attempt an estimate at a longer run cost are hardly music to the ears of gilts traders.

4. Today also delivered a warning to markets that governments are open to softening their fiscal anchors. The Truss government has intimated that fiscal rules requiring debt-to-GDP to decline over three years are at risk as “In due course, we will publish a medium-term fiscal plan.”

So, heavy debt issuance, uncertainty over exactly how much and willingness to toy with fiscal anchors is a recipe for blowing up the bond market. That’s focusing upon the issuance and supply considerations.

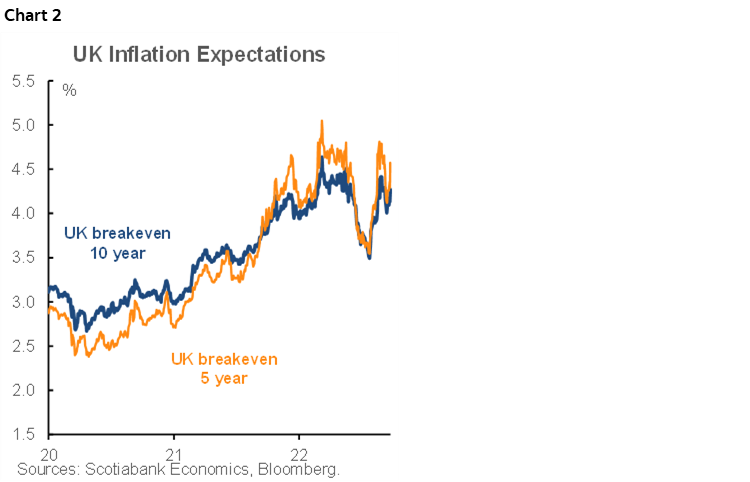

Markets are also worried about the consequences for inflation. The UK 5-year inflation break-even is up by about another 30bps this morning. Markets are saying fat chance to restoring price stability (chart 2).

Implications for the outlook for core inflation have resulted in pricing for the BoE’s next move on November 3rd immediately jumping by 25bps (and counting) this morning to anticipate a full 100bps hike. Sterling is in a nosedive as the weakest major cross albeit on a morning of general USD strength.

On the broader implications, it’s unclear to what extent foregone revenues will trigger more rapid growth but don’t start with Laffer curve nonsense about how tax cuts pay for themselves. In fact, in this environment of heightened uncertainty toward the job market and overall economic climate, it’s doubtful that folks will spend their tax cuts versus hording them. The government’s aim is to boost UK real GDP growth to a trend target of 2.5% which a) seems lofty, and b) if even remotely achieved adds to pressure on the BoE to tighten policy at a quicker pace.

It’s also likely fair to say that the composition of the tax cuts is politically tone deaf and immediately driving divisions. This FT article shows the likely tax savings by income level; anyone earning about £80k per year and up stands to save about £1,000 in taxes or more with earners over £200k estimated to save over £4k in taxes per year and that number only goes up from there for higher earners. Those earning under £80k down to £20k stand to save between about £200 to under £900 per year. Merry Christmas. The government argues that its energy plan helps lower and middle income households and so basically its tax cut plan focuses upon higher earners. Good luck with selling that.

With all of that, markets are also bracing for Italy’s weekend election and risks that may pose to Italian fiscal policy.

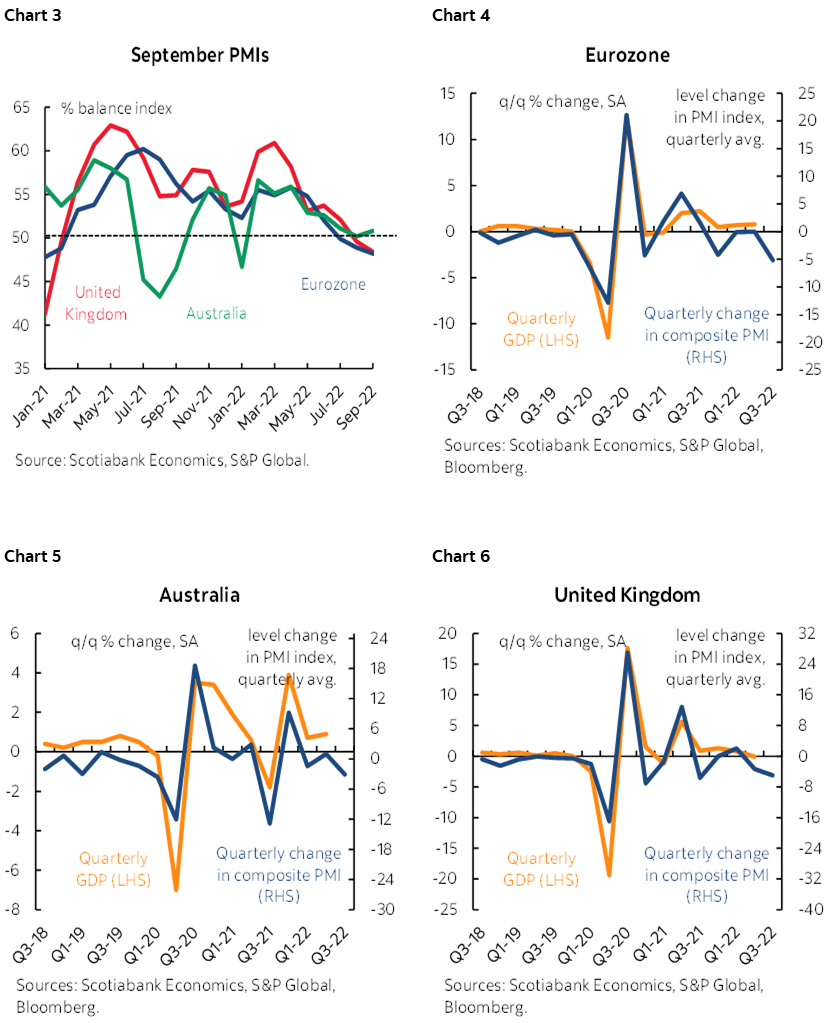

Data is playing a backseat role as a round of global PMI updates is about all there is to consider. See charts 3–6.

1. UK: The composite PMI fell to 48.4 from 49.6 (49 consensus). The services PMI fell by more than expected (49.2, 50.9 prior, 50 consensus) but the manufacturing PMI increased to a still contractionary 48.5 (47.3 prior, 47.5 consensus).

2. Eurozone: The composite PMI fell to 48.2 on-consensus (48.9 prior). The services PMI fell by 0.9 points (48.9, 49.1 consensus). The manufacturing PMI also fell (48.5, 49.6 prior, 48.8 consensus). All in contraction.

3. Australia: The composite PMI increased a touch to 50.8 (50.2 prior) as both the services PMI (50.4, 50.2 prior) and manufacturing PMI (53.9, 53.8 prior) ticked higher and are in mildly expansionary territory.

The US will update next (9:45amET) but these measures capture multinational firms whereas the Fed prefers the ISM gauges of domestic activity given its Congressionally mandated domestic dual mandate.

Canadian retail sales fell by 2.5% m/m in dollar terms during July which was worse than the initial –2% guidance. The prior month of June was also revised lower to 1% m/m (from 1.1%). August’s ’flash’ guidance pointed to a 0.4% m/m rise. Sales volumes were 2% m/m lower in July. I suspect that the 0.4% rise in the value of sales in August was driven by higher volumes since we already know that gas prices for instance were about 9% lower than the prior month. Rough tracking points to a Q3 decline in retail sales volumes of somewhere around 8% q/q SAAR assuming August’s gain was all volume-led and that September comes in flat in order to focus the math upon the effects of what we know so far. That’s not necessarily a collapsing consumer. Additional cautions include leakage of spending dollars out of retail sales probably into services spending that is generally not captured in retail sales. As folks re-engaged with their social circles, what they spent at restaurants, bars, airlines, hotels, movie theatres etc is all excluded from retail sales.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.