ON DECK FOR MONDAY, NOVEMBER 21

KEY POINTS:

- Risk off, as China’s back—and not in a good way

- Lockdowns return to Chinese city

- PBoC keeps LPRs unchanged as expected

- German producer prices unexpectedly plunge…

- …but solely due to energy prices

- Thai GDP beats, currency shakes it off

- Very light developments expected today

- Global Week Ahead reminder

Please see the Global Week Ahead—World Cuponomics (here) and the accompanying slide deck (here).

Key topics in this issue of the Global Week Ahead:

- This could be an earlier, stronger holiday shopping season…

- …as buy early sentiment and World Cuponomics…

- ... combine with Black Friday, Cyber Monday

- The week’s second half may be ripe for volatility trades

- FOMC minutes: in case you didn’t hear them the first time

- BoC guidance may focus on stability, wages

- Canada’s dubious international standing on wage pressures

- Will the RBNZ take a more hawkish turn?

- Bank of Korea likely to downshift

- Riksbank: hard to be more hawkish than markets

- PBoC likely to leave LPRs unchanged

- Turkey’s rate cuts to keep fanning inflation

- PMIs are signalling a worldwide contraction

- US cap-ex investment still a bright spot?

- Canadian retail sales transition to the holiday season

- Light global inflation, GDP updates

Moving onto the day’s developments, China is back, and not in a good way. Risk-off sentiment is driving the USD to be stronger against all major crosses. US and Canadian equity futures are down by ¼% to ¾%, European cash markets are slightly softer on average and Asian equities slipped with the Hang Seng’s nearly 2% decline leading the way. Oil prices are a few dimes lower. Sovereign bond yields are little changed on balance.

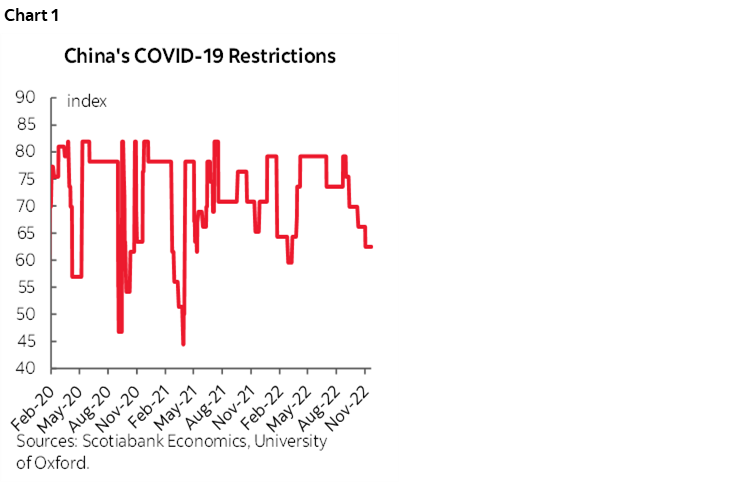

The culprit is that China’s on and off COVID Zero sentiment is, well, off again. Following a recently declining trend in China’s stringency index (chart 1), lockdowns returned to a city of 11 million that was thought to be easing. A spike in cases drove the reversal, with schools shutting as people were ordered to remain at home for five days as a mass testing program was unveiled. Three covid-19 deaths (yes three…) were registered in Beijing. One issue is uneven application of the National Health Commission’s 20 measures that were announced last week and meant to guide more targeted restrictions. Clearly another is China’s hypersensitivity to relatively small numbers of cases and its stubbornness toward embracing superior foreign vaccines.

Other overnight/weekend developments were very light. The People’s Bank of China left its 1-year and 5-year Loan Prime Rates unchanged as expected. German producer prices unexpectedly fell by 4.2% m/m (+0.6% consensus) and that mattered for, oh, let’s say maybe half an hour before 2-year bunds moved on. One reason for that may have been realization that there wasn’t any breadth to the weakness outside of energy prices (-10.4% m/m); PPI ex-energy was up 0.4% m/m. Thailand’s Q3 GDP beat expectations at 1.2% q/q (0.8% consensus) and absolutely nobody cared given China’s issues.

Very little is on tap by way of calendar-based risk today. A minor US release—the Chicago Fed’s National Activity Index for October (8:30amET)—and San Fran Fed President Daly (1pmET) are all that’s on offer.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.