ON DECK FOR MONDAY, JUNE 20

KEY POINTS:

- Light start to what should be a less active week for calendar-based risk

- Major center-left governments are being knocked down a peg or two…

- ….first Canada, now France, soon Biden

- Markets will react to Colombia’s election tomorrow

- ECB’s Lagarde, Fed’s Bullard on tap

- US markets shut for Juneteenth holiday

- Global Week Ahead

Please see the Global Week Ahead here. Since published on Friday evening we’ve had the French and Colombian election results (see below), but most of the week’s major developments are still ahead. Key topics include:

- A rotation toward services could insulate the economy

- Fed’s Powell to deliver hawkish warnings to Congress

- Canadian inflation to reach for greater heights

- BoC may firm up super-size risk

- UK CPI holding high, further upside ahead

- Macron’s agenda at risk in French election

- Banxico expected to hike 75bps

- Colombia’s Presidential election

- PBoC likely to hold LPRs

- Norges to hike, size and guidance in question

- Bank Indonesia to hike on currency and stability concerns…

- …and ditto for Philippines’ central bank

- Turkey’s messed up monetary policy

- Global PMIs to headline other indicators

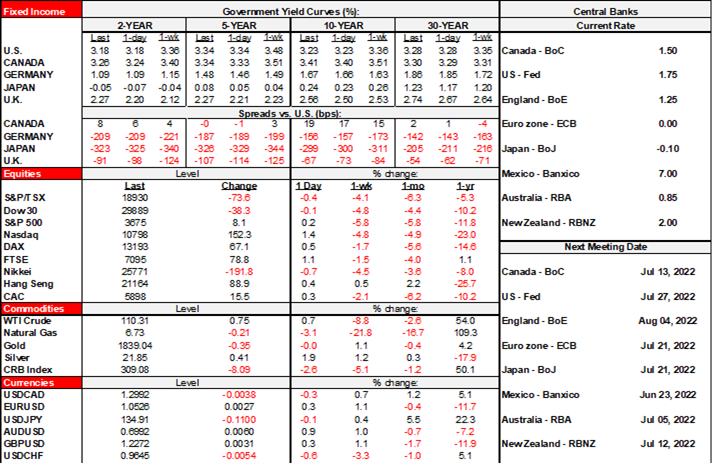

A light calendar and the fact that US markets are shut for the second annual Juneteenth holiday is offering a fairly subdued start to a fresh trading week. N.A. equity futures are higher by about ½% to ¾%. European cash equities are up by as much as 1% in London and Spain. That followed a generally soft tone across Asian equities. With Treasury trading shut, mild moves across sovereign bonds position about a 6–7bps cheapening in gilts as the main stand-out. The USD is a touch softer.

Colombia’s election was won by the narrowest of margins as left-wing candidate Gustavo Petro took 50.4% of the vote. Markets will weigh his ambitious plans against the fact he lacks a majority in Congress, but we’ll have to wait until tomorrow for market reaction given that today is a holiday in Colombia. I’ll leave further views to Scotia’s large LatAm research team to stickhandle.

Macron’s loss of his Parliamentary majority may be behind mildly wider French spreads over bunds toward the longer end. Macron’s allies won only 245 seats and hence well shy of the 289 required for a majority. The left-wing coalition Nupes was next at 131 seats followed by 89 seats for the National Rally and 61 for center-right allies. While aspects of his reforms may be jeopardized, the clear message from voters in France, Canada last Fall and soon the US come November is more tilted toward applying checks against the center-left political ambitions within major economies.

The PBoC left its 1- and 5-year Loan Prime Rates unchanged overnight as most had expected.

ECB President Lagarde speaks twice (9amET, 11amET) at the same event to deliver introductory remarks before a European Parliamentary committee. We’ll also hear from ECB Chief Economist Lane at an economists event (3:30pmET).

Notwithstanding the US holiday, St. Louis Fed President Bullard speaks this afternoon on inflation and rates (12:45pmET). Canada's calendar is dead quiet with nothing useful to consider while markets will be more subdued given the US holiday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.