ON DECK FOR TUESDAY, AUGUST 2

KEY POINTS:

- Markets in risk-off mode on the Pelosi factor

- Why is Pelosi in Taiwan?

- You’ve seen nothing yet by way of supply chain disruptions and inflation…

- …if conflict escalates around Taiwan

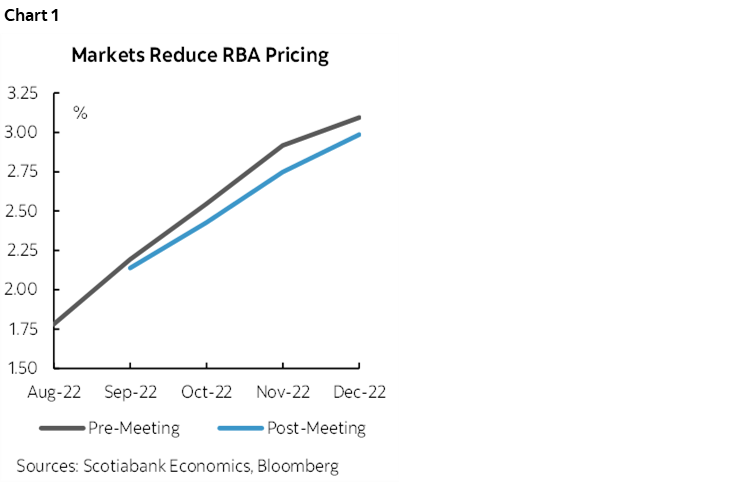

- RBA hikes 50bps, markets may be misinterpreting forward guidance

- Fed-speak, US vehicle sales and JOLTS on tap

- Global Week Ahead reminder

As a reminder, please see the Global Week Ahead—Into the Dog Days that was first sent on Friday. The publication is here and the companion deck is here.

Key topics in the Global Week Ahead:

- Are US nonfarm payrolls still resilient?

- Could Canadian jobs rebound?

- BoE will likely hike 50bps

- RBA to step further toward neutral

- Brazil’s CB still on a hiking path

- Other global macro

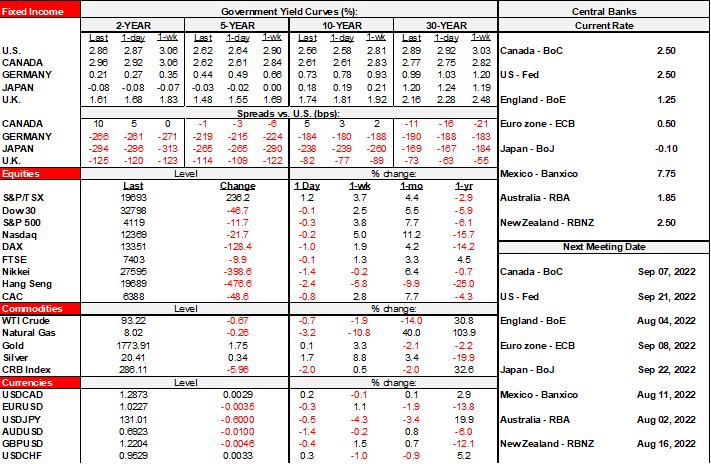

Markets are in mild risk-off mode on the Pelosi factor (see below). Sovereign bonds are gently rallying across all major markets. US equity futures are off by between ¾% and 1% across the benchmarks with Toronto down by nearly 1% and European cash markets down by as much as 1%. Asian equities sold off by 1–3% across benchmarks with declines led by mainland China’s exchanges. The USD is slightly firmer against most crosses except for the yen that is also picking up safe haven flows. Oil prices are about 1% lower.

US House Speaker Pelosi (Dem) is thought to possibly arrive in Taipei by mid-morning or a little later eastern time (various sources are all over the map on the exact time). China and Taiwan have both been engaged in some military posturing. China’s media and President Xi Jinping’s remarks on a call with Biden last week have put forth thinly veiled threats of unspecified actions if she does indeed land. What she says when she’s there matters less than the optics.

So why is she there?

- On the one hand, perhaps the US wants to make it clearer to China that it has Taiwan’s back than was the case with Trump’s shameful failure to do so with Russia and his supportive comments for Putin during his term.

- On the other, perhaps the US is poking the bear and being unhelpful by going out of its way to embarrass China at home and abroad. This is of course the line that Russia is taking this morning as one dictatorship that has invaded a sovereign nation sides with another.

- It’s also entirely possible that Biden is looking to shore up his foreign policy creds into the mid-terms as one of the oldest playbooks in US politics. Enter yesterday’s drone attack on an Al-Qaeda leader that has obvious merit but at least coincidental timing in the lead-up to mid-terms. A danger here is that this timeline roughly overlaps with Xi Jinping’s quest for a third term that is likely in the bag unless but could face risk if his response is perceived as being weak.

The potential ramifications of conflict around Taiwan would obviously invoke further damage to global supply chains given Taiwan’s important role in supplying semiconductors and electronic components. That would mean more inflation.

The RBA hiked 50bps to a cash rate target of 1.85%. The market’s interpretation of the forward guidance led to a sell off in the A$ and a rally in Australian government bonds. The 2-year yield fell by about 4bps post-statement but is still cheaper than last Friday’s close (Australia was on a bank holiday yesterday). We’re seeing central banks alter their language as they enter neutral rate ranges and guide that how much further they go and at what pace will be more data dependent. In Australia’s case, it involves noting they are not on a pre-set path. Markets are incorrectly interpreting that as dovish pivots in my opinion and therefore at risk of getting caught flat-footed yet again should central banks hike by more than priced as in the case of the Fed. As for the RBA, they totally blew it on inflation much like the Fed so I don’t know why any analyst or trader would pay much attention to their forward guidance anyway.

The US calendar only includes vehicle sales for the month of July that are expectedly to post a modest rise late in the day. Lagging JOLTS job openings and quit rates for June won’t help with Friday’s nonfarm payrolls but watch for further signs they are pulling off while I’ll bet many of them are now zombie postings anyway. A trio of Fed-speakers round it all out including Evans (10amET), Mester (1pmET) and Bullard (6:45pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.