ON DECK FOR THURSDAY, SEPTEMBER 9

KEY POINTS:

- Stocks shake off pre-ECB jitters

- ECB: “The lady isn’t tapering” because she already had!

- China’s futile release of strategic oil reserves

- Chinese CPI downside reinforces RRR cut speculation

- Gilts curve continues to bear flatten on Bailey’s remarks

- The BoC is unwilling to be easily knocked off course…

- …while preserving optionality to hike when spare capacity shuts in 2022H2…

- …which means not skipping chances to taper to net zero...

- …and then reinvest for a meaningful period before hiking

- Enter Macklem’s speech on QE and the reinvestment phase

- Canadian jobs preview

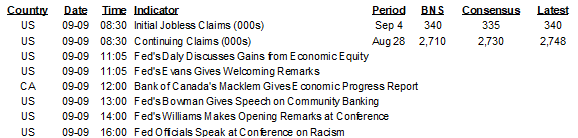

- US jobless claims dip, with cautions

Stocks had been moving lower before the ECB earlier this morning but have since shaken off much of that dip. The S&P500 is pushing gently higher, mainland European exchanges are higher in Germany and France but the FTSE100 is selling off on BoE remarks. The dollar is broadly softer. US Treasuries and Canadas are little changed while the front end of the gilts curve is underperforming and EGB 10s are rallying by 3–8bps partly on the lack of a hawkish surprise from the ECB compared to what they were already doing with purchases.

The gilts curve is flattening and underperforming all major markets with 2s up another 2–3bps this morning as yesterday’s remarks by BoE Governor Bailey continue to be digested. Bailey said during parliamentary testimony that he thought the minimum criteria for tightening monetary policy had been met. The criteria include eliminating the output gap and sustainably getting 2% inflation. He also said ending QE on target by the end of this year would be a tightening of policy. Therefore, you could take his comment to support front-end cheapening, but for now it could also simply reinforce that QE is ending.

German trade figures were soft. Exports advanced for a fifteenth consecutive month (0.5% m/m, 0.1% consensus) but only due to higher prices as export volumes fell 0.8% m/m. Imports fell 3.8% m/m (+0.1% consensus), entirely due to lower volumes (-6% m/m).

China’s CPI inflation pulled back to 0.8% y/y (1% consensus and prior) with core also ebbing a tick to 1.3% y/y. Producer prices edged higher at 9.5% y/y (9% consensus and prior) but largely due to already known commodity price moves. Mining and raw materials producer price categories accelerated by the most while manufacturing prices were up 8% y/y (7.5% prior), Key is that consumer goods producer prices were flat (0.3% y/y) which indicates little pass-through into global consumer prices as opposed to tighter margins in China.

China released strategic oil reserves into the market on the back of the producer price figures which always strikes me as a futile gesture when others do it; whenever the US has done so in the past the effects on oil prices tend to be modest and transitory. Sure enough, WTI fell by just over a buck or under 2% after the announcement and Brent performed similarly but oil prices are already recovering much of that modest dip. Still, the signal—as opposed to the substantive immediate market effect—may be that China doesn’t want to tolerate a relative price squeeze on margins and consumer incomes through narrowly based oil imports that could spark further downside to consumer price inflation by squeezing real incomes. As an extension of this point, I’d place greater emphasis upon the softer CPI figures that matter more as they reinforce a bias for the PBOC to ease likely through another possible cut in the required reserve ratio at some point.

The ECB statement (here) unanimously shifted PEPP purchase language by guiding that net asset purchases under the PEPP program would be lower than over Q2 and Q3. They did not put a time stamp on this period of lower purchases by saying, for instance, that it applied to Q4 in general or a shorter or longer period and so they preserved flexibility around the length of time they would target lower purchases. In one sense that went against expectations they might have just shifted the language in guiding they will continue to purchase at a higher pace than earlier in the year while leaving markets to continue watching what they are actually doing with weekly purchases. In another sense, however, it simply reaffirms what the ECB has shifted toward doing over recent weeks as the pace of bond purchases has already diminished (chart 1). The wording of relevance here is as follows:

“Based on a joint assessment of financing conditions and the inflation outlook, the Governing Council judges that favourable financing conditions can be maintained with a moderately lower pace of net asset purchases under the PEPP than in the previous two quarters.”

Lagarde offered a cheeky twist on “Iron Lady” Margaret Thatcher’s famous line that “the lady is not for turning” when she said “The lady isn’t tapering.” We could ignore that as mere entertainment if not for the fact it’s not true relative to what markets have been observing in ECB behaviour and not to mention that the twist is a bit demeaning to UK history—not to mention the original inspiration for Thatcher’s quote. Thatcher’s nickname made the quote a touch more appropriate and it was delivered in the grander context of how Thatcher meant she would not reverse her efforts to liberalize the UK economy despite having come under pressure within the Conservative Party ranks for doing so. Thatcher did not bend. Lagarde, however, already did as the ECB had already been reducing actual purchase data.

They will face further dialogue and decisions at subsequent meetings over what to do as the PEPP program approaches its maximum size but that’s unlikely to figure prominently today.

CANADA

Canada continues to heat up the back half of the week on the heels of yesterday’s BoC statement and last evening’s leaders debate. Sticking to my job in judging these events through the lens of an economist while looking for shreds of substantive differences I have to say that I saw very little to nothing of interest that was worthy of bringing to your attention and instead saw the evening dominated by a bunch of opportunistic—and at times desperate—posing around ‘wedge’ issues. Really can’t wait for tonight’s second round in English….

Into Macklem’s pending appearance. As a reminder here is my take on the BoC statement that surprised me a little in terms of the length compared to other pre-election statements but more importantly in terms of some subtle indications of how the BoC is reading the tea leaves. They could have easily gotten away with a short and sweet see-you-in-October statement but they couldn’t resist tweaking some of the language that indicated a bias to look through a soft patch as narrowly based and transitory while softening some of the subtle language around inflation and supply chains. Was that to be expected ahead of an election? Not really, as they need not have done either of those things quite as explicitly in as long a statement at this point. They had something to say and I think that’s a good segue into today.

Governor Macklem speaks at noon ET today on QE and the reinvestment phase. See the Global Week Ahead for a section on topics he may broach that could still inform market participants’ views regardless of the election. The takeaway from yesterday’s statement may be that the BoC continues to set a high bar against being knocked off course in its overall order of operations before getting to a first hike. Pending new forecasts, for now it is still guiding that spare capacity will shut over 2022 and they have previously guided that would be the condition for commencing rate hikes. Prior to negative GDP revisions it was looking as those spare capacity might shut before then. They have also previously guided they would reinvest a flat lined QE portfolio for a time before getting to that hike stage. To be meaningful, this implies that reinvestment would have to occur for at least several months/quarters which in turn implies that the order of operations merits ending net purchases likely by year-end, maybe early next year. In my view, don’t be fooled by any temptation to think they will be blown well off course toward ending QE by a soft patch as doing so risks violating the order of operations on the path to a first hike that they’ve fairly explicitly guided. Look for nuanced discussion around this as a possibility today but with guidance that a hike is still a considerable way off. Beyond that, there are a lot of issues of mechanics around reinvestment that I went over in the week ahead.

Then we’ll be onto tomorrow’s jobs report for August that will further inform the narratives around the Canadian economy’s performance and the BoC’s stance into October’s forecast revisions.

I plugged in 50k for my guesstimate. The median consensus guesstimate is 67k and a higher average estimate of 81k indicates that there is a bit of an upside skewness to the distribution of estimates. The standard deviation is 33k. The 95% confidence interval for monthly job changes in this household survey is +/-58k. The highest estimate is 160k and there are several of us around the lowest estimate of 50k. There is no whisper number for Cdn jobs.

As for drivers around the guesswork:

- Delta shouldn’t be as big a deal as it was for US payrolls. Canada’s new cases per capita are running at about one-sixth the US rate and Canada’s cases started to rise later than the US. There was little change in new cases between LFS reference periods in July versus August (the weeks including the 15th day of the month).

- reopening effects and the relaxation of prior controls continued. A new indicator from StatsCan combines various readings into one real-time gauge that correlates reasonably well with hiring activity. See my week ahead.

- mobility readings increased between reference periods and presumably they were not all just pleasure drives and transit rides.

- This morning’s Ivey PMI leans toward a decent gain with upside potential, but without the greatest tracking. The employment subindex increased by 4.8 points to a hefty 66.9 which recovers about half of the dip from June’s high into July’s reading.

- job postings continue to rise in Canada

Going into tomorrow, Canada is only 246k away from recapturing all lost jobs since February 2020. Where does overall job market slack stand especially in a BoC-Fed relative sense? The unemployment rate is 1.8ppts higher than Feb’20. The participation rate is only 0.3% lower than it was in Feb’20. After adjusting for measurement differences, Canada’s UR is 6.2% (July) versus 5.2% (August) in the US. Canada’s R8 equivalent to the U6 measure in the US (8.8%) is 11% but knock at least 1½% off Canada for measurement differences to compare to the US. Canada’s 6¼% NAIRU measure of the UR is 2¼ ppts above the US. Soooo….using U6/R8 relative to NAIRUs shows the spread at just over 3% in Canada versus just under 5% in the US. Ergo, all-in, Canada has less labour slack than the US.

UNITED STATES

US weekly jobless claims fell to 310k last week (335k consensus, 345k prior) and are running at just 100k above where they were before the pandemic struck. That said, there are two cautions. One is that the big state of California was estimated this time. Second is that there should always be caution around how to interpret weekly claims into and out of long weekends when other plans could get in the way of making trips to the filing office and when seasonal adjustments may or may not adequately control for the holiday effect.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.