ON DECK FOR WEDNESDAY, OCTOBER 13

KEY POINTS:

- Markets focused upon US developments…

- …as earnings season kicks off with beats…

- …ahead of a possible reacceleration of US inflation…

- …while FOMC minutes are likely to be stale on arrival

- A disastrous month for UK forecasters…

- ...was at first totally ignored by gilts, sterling

US CPI, US earnings and FOMC minutes will dominate market attention after a relatively quiet overnight session.

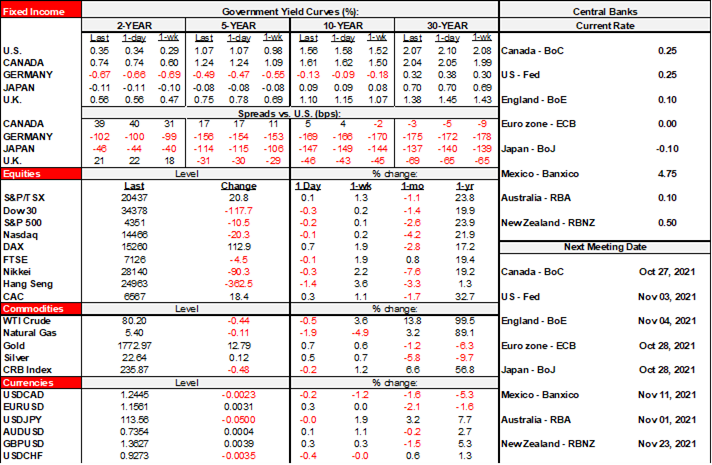

Sovereign curves are bull flattening with 10 year yields down ~4bps across Europe and with N.A. underperforming. The dollar is broadly weaker, but only slightly. Stocks are mostly higher with N.A. futures up by either side of ¼% across exchanges and European cash markets split between a slight dip in London and Spain and rallies across the rest of Europe.

The monthly UK data dump for August was an overall disappointment in what can best be described as a disaster for UK forecasters. If markets cared, then there was a long fuse on the trade as UK 10s didn’t start rallying until about a couple of hours after the releases and around the same time that a milder rally in US 10s began.

So what happened? The UK economy grew by 0.4% m/m in August (0.5% consensus) but the prior month was revised from a mild +0.1% expansion to a mild -0.1% dip. Industrial output grew by 0.8% m/m (0.2% consensus) which looked good at first except the beat only occurred because the prior month was revised down to 0.3% from 1.2%. Services missed all around with August up 0.3% m/m (consensus 0.6%) and the prior month was revised down a tick to -0.1%. Construction output came close to meeting expectations as a 0.2% m/m drop in August (+0.4% consensus) was mainly due to a higher than previously report jumping off point as July got revised up to -1% m/m from -1.6%. Finally, the trade deficit widened with negative revisions and against expectations for a narrower deficit as exports fell faster than the drop in imports.

Chile’s central bank is expected to hike by 75–100bps later today (5pmET). Scotia’s Chilean economist thinks they’ll hike 75bps. Soaring inflation is the catalyst alongside the central bank’s guidance that it feels it needs to get from an overnight rate of 1.5% to a more neutral level ~3.5% by 2022Q1.

UNITED STATES

US earnings season kicked off in earnest this morning with BlackRock already posting a beat (adjusted EPS US$10.95, consensus $9.39). JP Morgan followed that with a beat of its own as EPS landed at US$3.74 (consensus $2.97).

The main focal point will be US CPI for August. I expect a reacceleration after a temporary deceleration in during August. See the Global Week Ahead write-up for more thoughts (here) as well as the accompanying deck. A few highlights are as follows.

Headline CPI:

- consensus 0.3% m/m, 5.3% y/y (Scotia 0.4, 5.5)

- one-third of consensus is at 0.4 m/m, two-thirds 0.3

- most are at 5.3–5.4 y/y. I’m at the high end.

Core CPI:

- consensus 0.2% m/m, 4.0% y/y (Scotia 0.3 / 4.2)

- it’s almost a 50–50 split between 0.2–0.3 m/m with a handful at 0, 0.1 and 0.4

- most estimates are at 4.0–4.1 y/y with a few at 3.8–3.9 and a few at 4.2

Reasons:

- September is normally a mild seasonal up-month as a baseline.

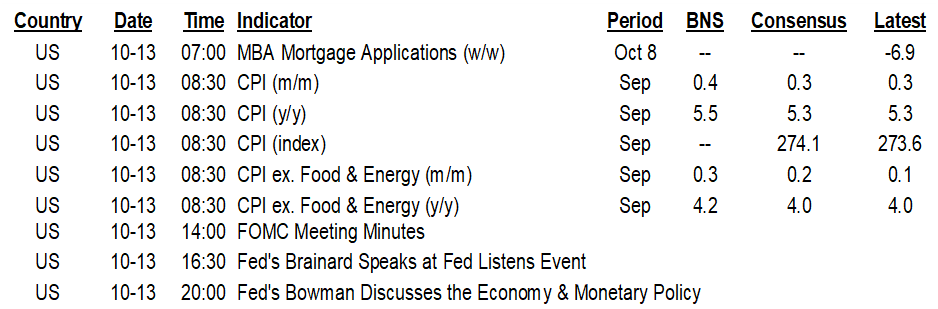

- used and new vehicle prices were both tracking about +4% m/m SA in September and so used vehicles should reverse the prior month’s outright decline as a one-off against the trend. The temporary small dip in used vehicle prices during August gave way to a renewed gain in September (chart 1).

- ISM price gauges bounced higher in September after a mild softening trend (chart 2).

- natgas prices soared in September and so I expect some pass through into CPI.

- ‘Food at home’ could accelerate at a quicker pace given broad composites of food prices have accelerated again over the past two months following a softening trend from May–July.

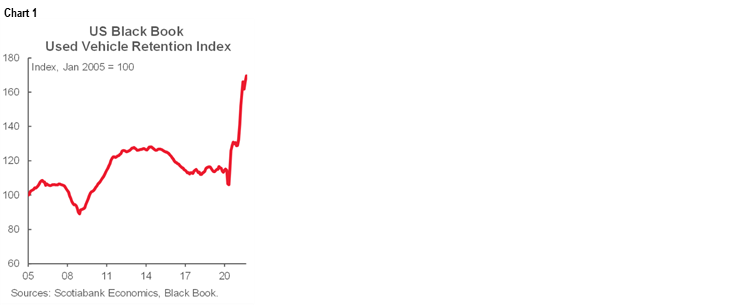

- I’m expecting less drag from the high contact components like airfare etc this time around. During August, it was the high contact sectors that made the biggest negative contributions to m/m price changes in weighted terms (chart 3).

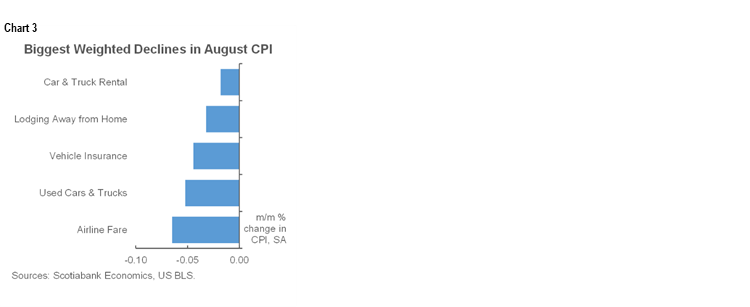

- OER, rent and medical care are expected to be solid contributors as OER plays catch up to house prices in typical lagging fashion (chart 4).

FOMC minutes (2pmET) will largely just reaffirm what was laid out in the statement, dots, forecasts and press conference 3 weeks ago. Fresher information includes Friday's payrolls and today's CPI plus the week’s Fed-speak. Today we’ll hear from Governors Brainard (4:30pmET) and Bowman (8pmET) for their possible take on the latest inflation readings.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.