ON DECK FOR WEDNESDAY, JULY 7

KEY POINTS:

- Bonds are telling the US to fix its debt ceiling issues…

- ...but it probably won’t until late Summer…

- ...as the debt ceiling could mess up taper talk like it’s 2013 again

- Other plausible theories for the bond rally

- China floats cutting required reserve ratio

- What to watch for in the FOMC minutes

- Other light releases

The overnight session was a total yawner but the North American session is heating things up for bonds again. Calendar-driven volatility may be focused upon FOMC minutes later today.

US Treasuries were starting off relatively little changed earlier this morning but shortly after 8amET began to fall again. The 10 year T note is down 4–5bps on the day and sits at 1.30% at the time of publishing. Canada 10s are slightly underperforming the rally in US 10s. 10 year EGB yields are rallying by 2–4bps with gilts down 5bps. The USD was flat on the morning until appreciating just before publication. There are mild gains on average across N.A. equity futures and European cash markets with some negative effects on social media accounts given a headline about a Trump lawsuit.

What’s driving bonds? There are various plausible theories but the one I continue to like the most is the argument that there continues to be far too much liquidity pumping into markets and expected to continue doing so in relation to looming debt scarcity around when the US debt ceiling gets reinstated at month-end. That issue may also have the potential to complicate the Fed taper dialogue like in September 2013 when the Fed held off tapering because of similar issues that led to a government shutdown. Bills auctions are being slashed in preparation.

Congress is nowhere near moving toward either suspending the debt ceiling or raising it. As August recess approaches, it may not feel pressure to do so until Congress returns to address the need for a new agreement to fund the US government beyond September 30th. The political divisions may still be far too deep in order to drive bipartisan agreement toward doing anything before they absolutely have to and maybe not until after a nasty bun fight. Into a September timeframe is ballparked for a perfect storm marked by the exhausting ability of the Treasury to fund the government, heightened uncertainty over funding the government beyond the end of the month and an inflexible debt ceiling. The scenario that unfolds involves the material risk of a partial government shutdown and payments prioritization by Treasury as flagged for a while now. Such a scenario would again demonstrate before the whole world the massive dysfunction that dominates American politics and its destabilizing effects on world markets. The country’s role as a reserve currency, however, would perversely have the probable effect of driving Treasury yields lower again like in the 2013 episode among others which is what I think we are observing now. I’m not optimistic around settling any of these issues any time soon given ongoing deep divisions in US politics, but when it eventually settles, we could be setting up a massive cheapening trade for Treasuries with an expedited push toward Fed tapering. In the meantime, partial government shutdowns tend to involve small effects on growth that get recaptured in the next period while everyone else benefits from lower term funding costs. When the US government shut down in 2013 the economy still grew by 3.2% in each of Q3 and Q4. Meh. For now, this is probably market theatre with side benefits to a pathetic and recurring American political soap opera.

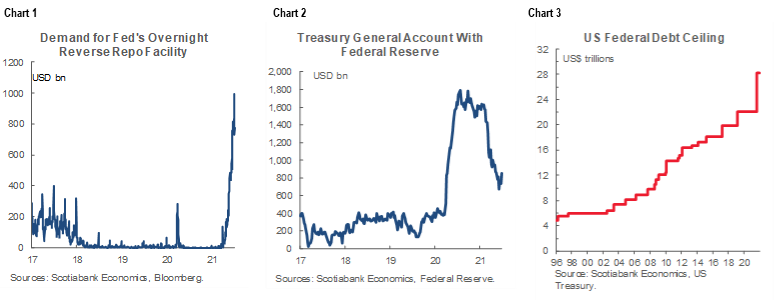

By way of refreshed background on the data, chart 1 shows the Fed’s RRP facility that is soaking up a fair amount of this liquidity. Chart 2 shows that there remain hundreds of billions of dollars of excess deposits over and above ~$450B that the Treasury has at the Fed that must be run down in order to comply with Treasury’s interpretation of the debt ceiling legislation. As this runs down, debt issuance is curtailed and then failure to raise the ceiling will put debt issuance on hold indefinitely while the Fed continues to buy US$120 billion of Treasuries ($80B) and MBS ($30B). Chart 3 shows where the debt ceiling may become binding at month-end.

How to fix this? Congress holds the keys. Its inaction on the debt ceiling is already having a very distorting and destabilizing effect on markets while the Fed is simply buying too much. The Fed has other tools at its disposal if it’s uncomfortable with the speed and magnitude of adjustment and distortions in fixed income markets, but they are band-aids when the durable solution lies with Congress. The Fed could raise or eliminate the counter-party RRP limits, raise IOER again

Other considerations are significant but more tangential in my view. Some of the market volatility may be due to positioning ahead of the upcoming US earnings season. Some may be due to OPEC+ dysfunction and note that energy was the dominant drag on the snp yesterday (-3.2%) indicating stocks could swing violently if OPEC+ gets its act together at some point. Some of it may be due to nearer term concerns about growth if supply chain issues continue to dampen some activity indicators, but I suspect the rotation of the sources of growth toward the distanced activities that are concentrated in services will still drive buoyant conditions ahead. The market may just need to wrap its mind around relatively transitioning away from a goods-driven expansion toward more of a role played by services that data and time will inform. The delta variant is lurking in the background with all eyes on the UK reopening risks as cases continue to climb. Some of the market effects may be month-end transitioning in terms of rebalancing effects with equity valuations being more carefully treated. Further, one always has to leave the door open to the possibility that bond markets undershoot ultimate resting points through pile-on trades.

German industrial output roughly met expectations net of revisions. Output fell 0.3% m/m in May (consensus +0.5%) but the prior month was revised up to a dip of -0.3% (from -1.0%). Still, momentum has been lost as output has fallen in four out of the five months this year. Onto H2….

China floated the possibility of cutting the required reserve ratios on banks early this morning. It has not cut those measures since January of last year in the thick of China’s pandemic (chart 4).

Canada’s Ivey PMI climbed to 71.9 (64.7 prior). It’s an all-economy PMI including the public and private sectors so it’s somewhat tough to read, but employment increased (69.6 from 67), inventories were stable relative to the prior month and price increases accelerated again as yet another inflationary signal.

Russia updates CPI inflation at 12pmET and both the headline and core measures are expected to rise again which may further fan tightening expectations.

UNITED STATES

Minutes to the incrementally hawkish June 15th–16th FOMC meeting will be the main focus (2pmET). JOLTS job openings for May hit a new all-time record high but really only because the prior month was revised down a touch.

Here is a repeat of the things to watch:

- it’s likely too soon to start talking about tapering mechanics and timing. A small minority thinks they should have already been tapering or talking more about it. Others want to watch data evolve over “coming meetings” before turning the dial up on the conversation around timing, amounts etc. The real doves don’t even want to reference tapering.

- Will “a number” of participants who are seeking to discuss tapering over coming meetings get upgraded using the Fed’s frequency of citations language? ie: several, many, most etc.

- Is it still “a number” who believe bottleneck price pressures will persist into next year, or more? It’s unlikely to be less.

- More fundamentally, watch for any frequency of citations language that evolves toward more uncertainty over the inflation outlook.

- Will “some” FOMC officials who are citing wage pressures and tighter job markets get upgraded to more members?

- Watch for signs around those who may be on the fence on hiking in 2022–23 and tapering faster/slower that may not be well captured in the dots themselves. It’s pretty clear that Powell got arm wrestled into different guidance on tapering in the context of monitoring nearer term data at this meeting so the breadth of discussion around this topic could get fairly lively.

- Watch the discussion around market liquidity in terms of how the Fed’s RRP hike, Treasury’s redeployment of its General Account at the Fed, ongoing Fed buying and debt ceiling dynamics interact. Watch for discussion around potential further steps. So far, the IOER hike and RRP facility have been working to raise bill yields and EFF.

Still, the minutes are going to be slightly stale post-nonfarm’s 850k even with soft details and with 56% of Americans >12 double dosed as of now (64% one dose). Further, returning to the start of this note, the discussion on tapering could well be vulnerable to being disrupted by debt ceiling issues just like in 2013.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.