ON DECK FOR THURSDAY, JULY 29

KEY POINTS:

- Risk-on sentiment driven by China, US stimulus

- Chinese regulators walk back fears of a regulatory clampdown

- US infrastructure and budget negotiations advance

- Germany’s economy is getting hotter…

- …and so is inflation

- US Q2 GDP a footnote amid forward risks

INTERNATIONAL

Global markets are in classic risk-on mode across asset classes this morning. The main catalysts include efforts to calm Chinese financial markets and progress toward advancing infrastructure and a bigger budget resolution in the US Congress. The German economy provided an assist to the risk-on tone. There is little to no follow-through on the Fed’s communications (recap here) as record earnings beats this season matter more (chart 1).

Stocks are higher across the board including strong gains in HK and mainland China after attempts by Chinese regulators to assuage concerns about a broader clampdown even though that’s basically what China is doing. Sovereign curves are steepening with 10 year yields up by 1–3 bps with Canadas and Treasuries leading the rise. The dollar is broadly softer with all major crosses and pretenders pushing higher.

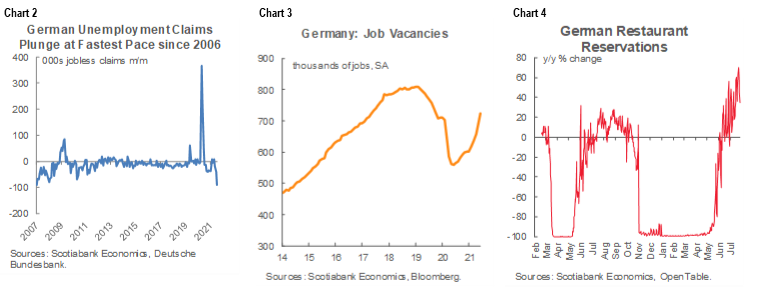

Some hot German numbers aren’t hurting. German unemployment claims fell by more than guessed (-91k) in July. That’s the fastest monthly improvement since May 2006 (chart 2). The unemployment rate fell two-tenths to 5.7% and is inching toward the 5% pre-pandemic level. Job vacancies are rising to 725k which is the highest since November 2019 (chart 3). It all coincided with Germany just crossing the 50% mark on the share of the population that is fully vaccinated (61% with at least one dose), although the rate of vaccination has slowed which has prompted increased vaccination efforts and more debate on targeted restrictions against the unvaccinated as elsewhere. Other signs of healing include restaurant reservations (chart 4).

German states have reported some hot inflation readings that point to upside risk to the national estimate due at 8amET. Consensus had expected 0.4% m/m and 2.9% y/y in the EU-harmonized reading but all of the states reporting so far have landed higher.

Preliminary Spanish CPI landed on expectations with the EU-harmonized measures at 2.9% y/y (2.5% prior) and down 1.2% m/m. Higher accommodation services (hotels) and gas drove the year-over-year rate higher along with food and electricity price effects.

UNITED STATES

US Q2 GDP (8:30amET) will be the main release this morning but it’s likely to be treated as a footnote in the face of forward uncertainties. Consensus estimates 8.5% q/q SAAR growth with most estimates between about 7–10% (Scotia 7.7%). Earnings risk is skewed to Amazon in the N.A. after-market.

Weekly claims (8:30amET) and pending home sales (10amET) will likely play second fiddle to GDP. Amazon is the main earnings risk in the after-market (EPS consensus US$12.28).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.