ON DECK FOR TUESDAY, DECEMBER 7

KEY POINTS:

- Omicron speculation drives risk-on, pending evidence!

- The RBA didn’t put up its dukes against bond markets

- Light overnight releases from China, Germany

- Canadian trade may inform Q4 growth tracking

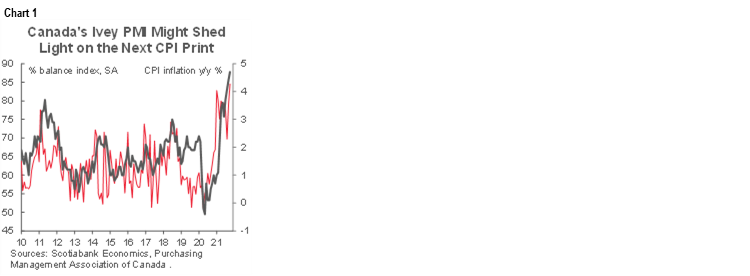

- Canada’s Ivey PMI might inform CPI inflation expectations

As far as I can tell, the main driver of this morning’s risk-on sentiment is speculation that Omicron will be a manageable risk. There isn’t much to go by other than Glaxo’s study on its antibody treatment and a very lagging new entrant in the vaccine field, as markets will be more sensitive to when the first of hundreds of Omicron studies begin to be released at any moment from now through next week. Stocks continue to rally. US and Canadian futures as well as European cash markets are up by about 1–2% across the exchanges. Sovereign bonds are a touch cheaper across major markets with cheapening led by ‘down under’. Several commodity crosses are leading FX gainers against the USD and led by those most exposed to another $2 gain in oil prices, plus the A$/NZ$.

The main overnight moves saw cheapening in the Aussie/kiwi curves and strength in their currencies on the back of the RBA communications. It’s the first central bank to weigh in after the discovery of the Omicron variant and with the BoC up next tomorrow. The RBA didn’t put up its dukes against market expectations for rate hikes as much as markets may have anticipated. They repeated the criteria for reassessing bond purchases at the planned review in February that remain a) First, progress toward full employment and the inflation target, b) “the actions of other central banks,” which offers little intrigue over who they are referring to, and c) the functioning of the Australian bond market. So if the Fed shuts down purchases sooner than mid-2022 as they are expected to do next week and if evidence on liquidity effects from owning so much of the Aussie bond market continues to mount, then we’re left with tracking inflation, jobs and the broader growth drivers of each. On that, the RBA indicated Omicron is a new uncertainty “but it is not expected to derail the recovery,” though that sets a pretty low bar to get excited about. Still, they went on to look through the variant in saying “The economy is expected to return to its pre-Delta path in the first half of 2022” while emphasizing “a strong recovery in the labour market” and an expected “further pick-up in wages growth…”

German industrial output was stronger than expected in October (2.8% m/m, consensus 1%) and with a slight upward revision. Germany ZEW investor expectations were relatively little changed in the December survey and have been range-bound over the past four months. Chinese export growth eased broadly in line with expectations (22% y/y in USD terms, 27.1% prior) but imports soared (31.7% y/y, 20.6% prior). That drove the balance lower following a string a improvements that had been in place since April. Chilean inflation landed at 6.7% y/y in November, up from 6% but in the realm of expectations.

N.A. will only take down trade reports out of the US and Canada at 8:30amET. The US report is inconsequential as it just plugs in the services balance on top of the earlier preliminary estimate for the goods balance plus any revisions if necessary; a sharp improvement in the deficit is expected.

Canada’s trade figures will inform Q4 GDP tracking, but supply distortions are likely to weigh heavily on the figures. BC’s flooding that disrupted activity at Vancouver’s port in the second half of November will show up in the next month’s report. Last Friday’s tracking of the gain in hours worked at over 9% q/q SAAR in Q4 remains the best indication of Q4 growth prospects so far.

Canada's Ivey PMI (10amET) and its prices subindex might marginally inform CPI risks ahead of next week's print for November (see chart).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.