ON DECK FOR THURSDAY, APRIL 8

KEY POINTS:

- Treasuries rally slightly further post-claims

- Weekly US jobless claims edge up again

- Fed’s Powell on tap…

- …but takeaways from FOMC minutes set low expectations

- Canadian jobs preview

- German factory orders miss, UK PMI beats

- LatAm inflation prints land on expectations

INTERNATIONAL

Material new information is in short supply to explain mixed but generally mild evidence of a risk-on market bias. Overnight developments were very thin ahead and today’s calendar only includes weekly US claims, a likely uneventful appearance by Fed Chair Powell and a sprinkling of LatAm releases. See below for a look ahead to tomorrow’s Canadian jobs report.

- Stocks are catching a mild bid in US and Canadian futures and London and Paris but are somewhat mixed across the rest of Europe.

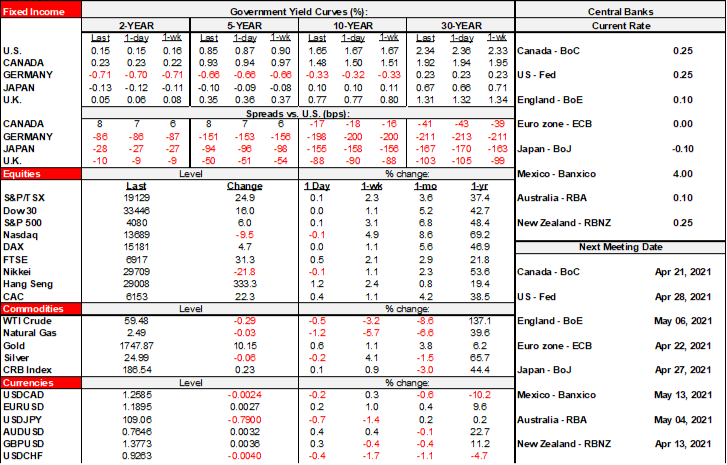

- US Treasuries and Canadian government bonds are outperforming most other curves over longer maturities and rallied a bit further after US claims. Longer-term yields are down by 2–3bps in both countries.

- The USD is slightly depreciating against most major crosses.

German factory orders fell a little shy of expectations because of downward revisions. They were up by 1.2% m/m in February which was on consensus, but January was revised to +0.8% from 1.4%.

The UK construction PMI strongly beat expectations at 61.7 (55 consensus, 53.3 prior).

Mexican CPI landed on the screws at 4.7% y/y and up by about 0.9% from the prior month’s year-ago pace. Prices were up 0.8% m/m which was also on consensus. Minutes to Banxico’s March 25th meeting arrive at 10amET.

Chilean inflation also landed in line with expectations at 2.9% y/y (3.0% consensus) with core at 2.6% y/y.

CANADA

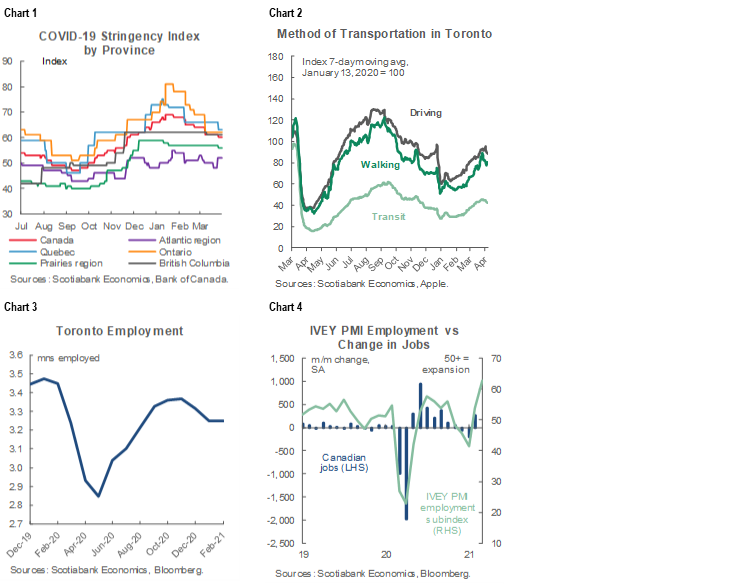

Canada’s calendar is empty today, but we’ll get a jobs report tomorrow that will probably offer a fleeting gain before renewed job losses in the subsequent report next month. My guesstimate submitted last Tuesday was for a 100k gain which turns out to be the median consensus call notwithstanding a range from about 50k to 175k across individual estimates. Much of that dispersion is captured within the random noise aspect of the call given the 95% confidence interval for monthly changes in employment is +/-58k.

We can, however, point to a few general references to labour market conditions in support of expectations for a decent gain tomorrow. Restrictions eased into the March reference week that includes the 15th of each month (chart 1). That was particularly so in Toronto that did not participate in the February nationwide job gain of 259k and is likely to play a leading role tomorrow by recapturing some of the lost jobs over prior months (chart 2). The impact of easing restrictions was seen in mobility readings (chart 3). We also learned yesterday that hiring intentions shot sharply higher as the employment subcomponent to the Ivey PMI hit the highest reading since November 2007 (chart 4).

But wherever tomorrow’s print lands, it’s all going to be very fleeting as the country goes back into varying degrees of lockdowns to counter rising COVID-19 cases. Still, Canada has had a total of 1.04 million COVID-19 cases to date versus about 31 million in the US. The US has had about 31 times as many COVID-19 cases as Canada with only 9 times the population so the gold medal for pandemic mismanagement still goes to the US by a landslide margin. A big pharma home bias is serendipitously bailing out the US through vaccines and sowing future moral hazard should another pandemic arise. Canada’s vaccine progress is frustrating and has multiple drivers dating back decades in time but it’s still likely that the country is 1–2 quarters behind the progress in the US.

UNITED STATES

Fed Chair Powell will be on an IMF panel with the heads of the IMF and WTO at about 12pmET. I wouldn’t expect a whole lot out of this. Yesterday’s meeting minutes generally indicated as much. The minutes made it clear that FOMC officials don’t wish to be hassled by pleas to update their views at every twist and turn when they said:

“They noted that a benefit of the outcome-based guidance was that it did not need to be recalibrated often in response to incoming data or the evolving outlook."

Translation? Buzz off. Leave us alone. We gave you our fresh guesses at the last meeting and now we’re back to watching developments on fiscal plans, data, vaccines and consumer behaviour just like the rest of you are and all of this will take time to assess. Ergo, don’t look to Powell to indicate any material narrative swings today.

Otherwise, the minutes to the March meeting were a) stale, and b) pretty uneventful. Stale because they speak to the discussion in mid-March after which the vaccine curve super accelerated and before President Biden announced his American Jobs Plan with infrastructure spending financed by corporate tax hikes as we await his next American Families Plan. The minutes repeated reference to being “some time” before the conditions for adjusting Treasury and MBS purchases are expected to be achieved; we heard the same reference in the prior minutes among other communications. Third, the minutes reinforced willingness to adjust short-term administered rates if required in the face of a pending onslaught of liquidity as the Treasury General Account gets redeployed. Here is the exact quote:

"Following the discussion, the Chair noted the potential for downward pressure on money market rates and suggested that, should undue downward pressure on overnight rates emerge, it might be appropriate to implement adjustments to administered rates at upcoming meetings or even between meetings to support effective policy implementation and ensure that the federal funds rate remains well within the target range."

We also heard that a few participants were in favour of removing the counterparty ON RRP limit entirely, whereas the March meeting raised it by US$50B to $80 billion. The sum takeaway is that while big shifts are well down the road, money market participants got additional clues to be monitoring opportunities in short-term relative rates.

US weekly initial jobless claims backed up a bit last week to 744k and the prior week was revised up a bit to 728k from 719k. That’s higher than consensus expected and marks two weeks of increases. Still, initial claims have been bouncing around a range of roughly 660k to 760k since about mid-February. I would treat that as mostly noise following the prior improvement. Continuing claims also exceeded expectations at 3.73 million (3.64 million consensus) with a mild downward revision to the prior week at 3.75 million from 3.79.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.