ON DECK FOR THURSDAY, NOVEMBER 5

KEY POINTS:

- Markets continue to price ‘blue light’ scenario

- US election results still pending, updates expected by mid-day

- BoE expands gilt buying by more than expected

- US jobless claims hold unchanged

- Fed likely to stay out of the fray

- Ontario’s budget today

INTERNATIONAL

Groundhog day continues in the US where we didn’t really receive material new information to help determine the outcome of the US election. Markets continue to price the ‘blue light’ scenario. It’s still technically up for grabs both for the Presidency and the Senate. The odds continue to tilt in Biden’s favour but the Senate remains stuck at 48 a piece. Fulton County, Georgia is expected to make a further announcement by about 11amET this morning after Trump’s lead in Georgia narrowed to about 18,500 votes overnight. Nevada’s results are expected at about 12pmET. Philadelphia may update later this morning. Arizona is not expected to update until around 9pmET tonight. Market participants will continue to monitor rolling newsfeeds and announcements tracking vote counting in Pennsylvania, Georgia, Nevada and Arizona. President Trump is expected to make a ‘major announcement’ in Las Vegas but no time was provided.

Otherwise, there are low expectations for this afternoon’s Fed meeting. Ontario’s budget will be covered by Scotia’s Marc Desormeaux.

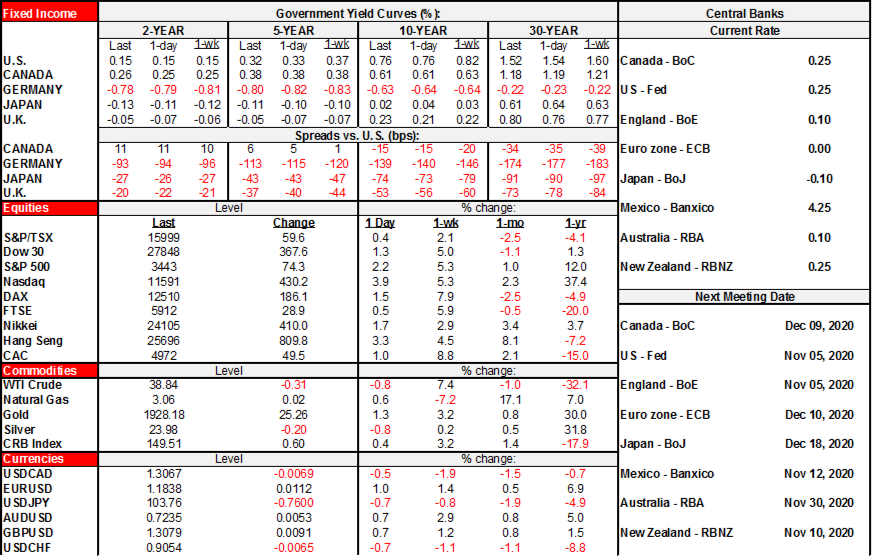

- US Ts are slightly richer and mostly toward the long end that’s down 2bps ahead of the Fed and in anticipation of election results. Canada’s curve is performing similarly. Gilts are a touch cheaper across the curve post-BoE including toward the front-end that is still negative yielding.

- Stocks continue to rally with US S&P futures up just under 2%, the TSX up similarly and European cash markets up by over 1% across all bourses ex-London’s ½% rise. Asian markets followed western markets higher overnight absent fresh regional catalysts.

- The USD is broadly depreciating, as it generally has been doing this week.

- Oil is off a dime or two as gold gains over 1%.

The Bank of England expanded its gilts purchases program by £150 billion to £895 billion. That’s larger than expected but not particularly surprising given a general bias that £100 was a minimum bid to make it worth bothering. It was also in keeping with media reports late yesterday that £150–200 billion was being contemplated. Sterling depreciated right off the mark but is now a middle of the pack performer on a general down day for the greenback. Growth forecasts were also revised lower including a forecast 2% contraction in Q4. The BoE surprised no one by leaning against back-to-back contractions which should surprise no one at this point. Gilts came into the morning dearer by about 3–4bps in 10s and have since cheapened back toward yesterday’s level.

German factory orders expanded at a slower than expected pace of 0.5% m/m in September (2% consensus) with only a part of this miss attributable to a modest upward revision to the prior month.

UNITED STATES

US weekly claims held at 751k last week which is essentially unchanged compared to the prior week’s 758k. Another 538k decline in continuing claims is constructive. Nevertheless, we’re between nonfarm reference periods with these numbers, soooo onto nonfarm tomorrow!

The Fed’s latest statement arrives at 2pmET and will be followed by Chair Powell’s press conference at 2:30pmET for up to about an hour. Given the election, it wouldn’t surprise me if the presser was shorter. The Fed is likely to stay out of the fray with election results still unknown. Risks include adjusting QE terms (shift buying further out) and guidance (willing to do more). No forecasts or dots are due until next month.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.