KEY POINTS:

- Market sentiment sours as US stimulus talks drag on

- Global covid-19 trends in pictures

- The BoC’s twin business and consumer surveys in charts

- Fed’s Clarida repeats more needed, not out of ammo

- Light calendar-based risk overnight through tomorrow

TODAY’S NORTH AMERICAN MARKETS

A lack of obvious traction toward a US fiscal stimulus deal knocked risk appetite down a peg or two as the day wore on and particularly toward the end of the session. Stimulus headlines will remain dominant through tonight into tomorrow’s Pelosi-imposed deadline. Otherwise, global calendar-based risk will be light. The weekly round-up of global covid-19 cases is provided in chart form along with the main takeaways from the Bank of Canada’s twin business and consumer surveys.

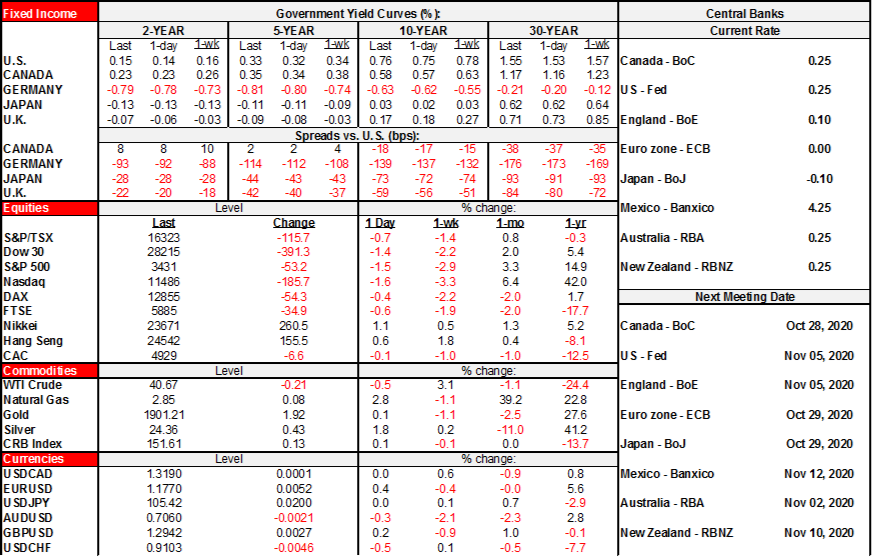

- US stocks fell by 1½% to just over that in the case of the Nasdaq. Canada fell by about ¾%. European markets sold off by a lesser amount on average because they shut before the fun really started in North American trading.

- Sovereign curves still wound up bear steepening a touch in the US and Canada. European markets saw Brexit headlines richen the gilts curve slightly while the main move in EGBs was to widen Italian and peripheral spreads.

- Oil prices fell by a few dimes with gold little changed.

- Currency markets generally still sold the greenback, but fiscal headlines this afternoon turned the dollar around somewhat. By the end of the session the Mexican peso sank to the weakest performer among major and semi-major crosses.

US fiscal stimulus talks dragged on today with no apparent deal in sight. As this note is being sent, we are awaiting guidance following a 3pmET call between US House Speaker Pelosi and US Treasury Secretary Mnuchin. Lower than even odds are likely attached to getting a sizeable package before tomorrow’s deadline that Pelosi imposed.

US Fed Vice Chair Clarida’s speech on the economic outlook and monetary policy contained no surprises (here). His main takeaway is that more monetary and fiscal policy stimulus is probably needed and that the Fed is not out of ammunition.

The Bank of Canada’s Business Outlook Survey (here) did not garner much attention by markets. It showcased improvement in measures like expectations for future sales growth, investment in new capacity and hiring plans as well as inflation expectations during Q3 compared to Q2. That was expected to reflect reopening efforts. The survey is nevertheless stale as it was conducted between August 24th and September 16th and hence before most of the second wave upturn in covid-19 cases. Charts 1–4 depict various aspects of what the limited size of 100 respondents across industries and regions said and the correlations with ‘hard’ data.

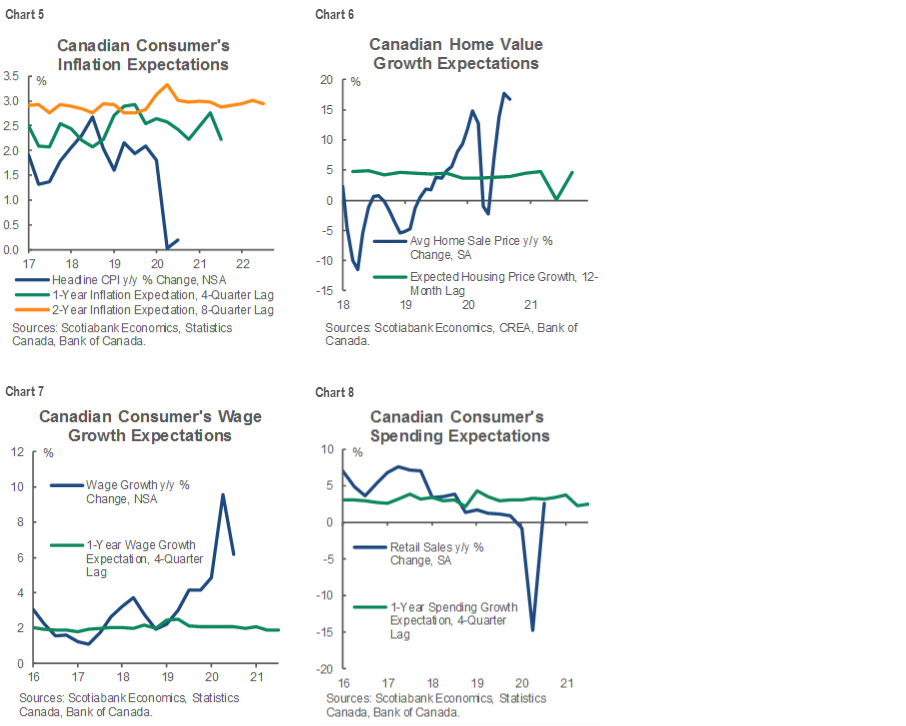

The Bank of Canada also updated its quarterly consumer survey (here). I’ll leave it to you to determine based on charts 5–8 whether their expectations are realistic or not. In my view, they’re too high on inflation but probably in the ballpark on house prices and wages with downside risk.

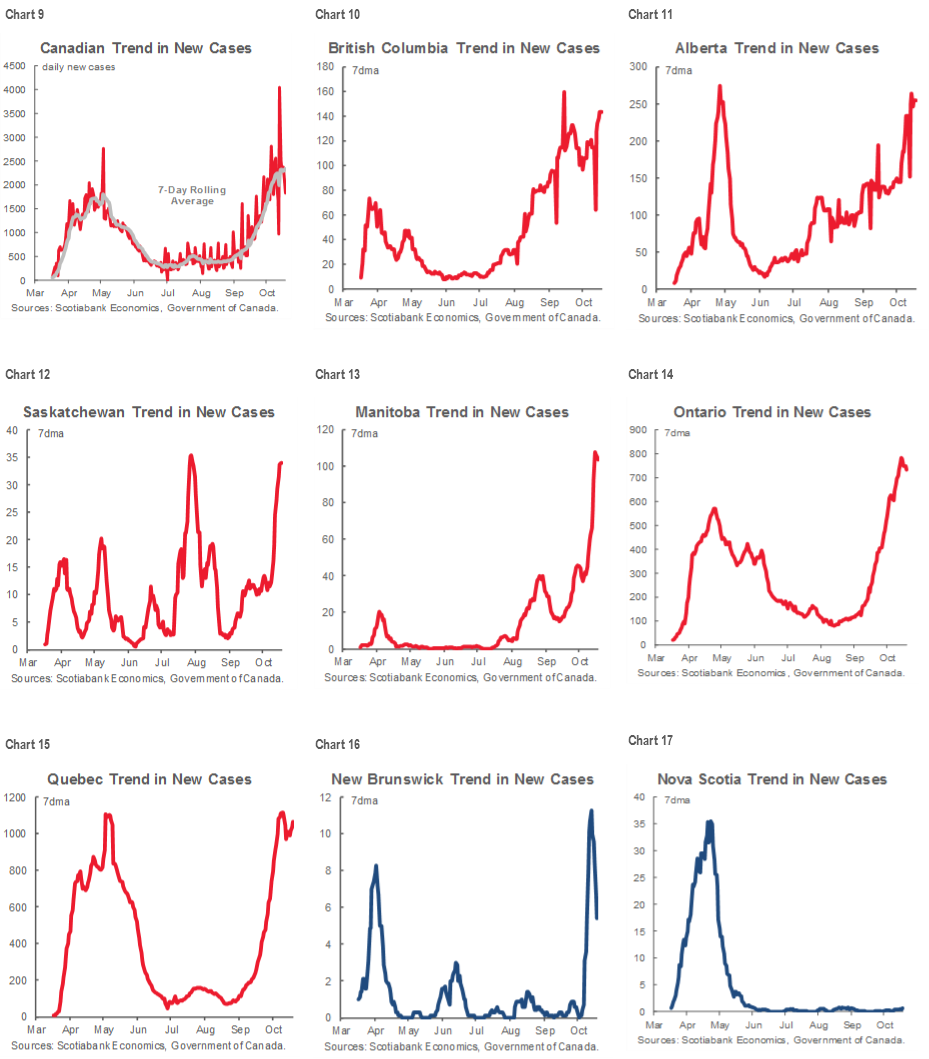

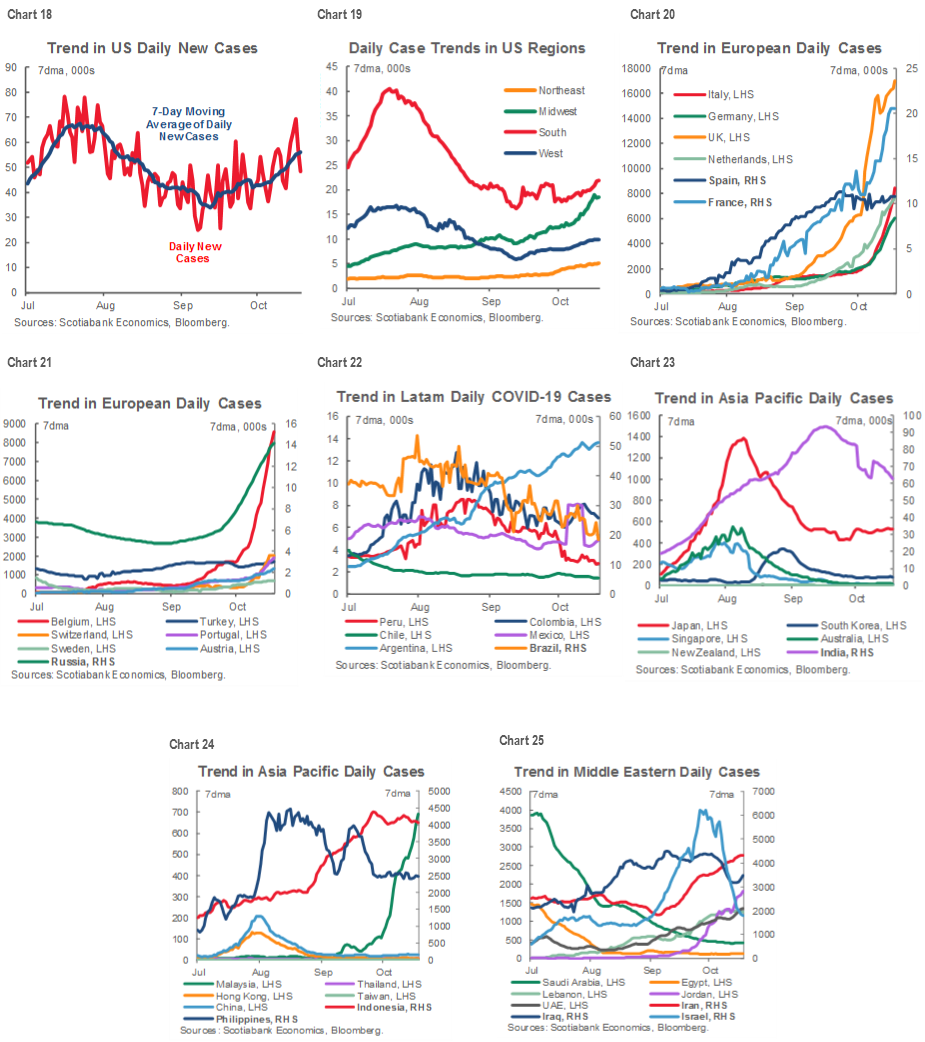

Since we’ve adopted the custom of providing global covid-19 charts at the start of each week, please see charts 9–17 for Canada and its provinces as well as charts 18–25 for global trends. All of Europe and North America is deep into second waves while case trends in LatAm and under somewhat greater control (ex-Argentina) and ditto across Asia except for Malaysia and Indonesia.

OVERNIGHT MARKETS

There is nothing material by way of calendar-based risk that is due out overnight that is likely to drive global market sentiment.

RBA October Monetary Policy Meeting Minutes (8:30pm ET): These minutes will be ignored by markets after RBA Governor Lowe’s speech last week. In his address, Governor Lowe suggested that its possible for the RBA cuts it’s cash rate 15bps to 0.1% as soon its November 2nd meeting. If this were to go ahead, the lower rate would likely be complimented by a reduction in the three-year yield target and new purchases in other parts of the Australian government bond curve.

PBoC One-Year Loan Prime Rate (9:30pm ET): Our Asia Pacific Economist Tuuli McCully expects the One-Year Loan Prime Rate to remain at 3.85%. Bank officials should signal their continued satisfaction with China’s recovery so far, despite Q3 GDP coming in softer than expected—4.6% y/y compared to the 5.5% y/y consensus. In addition, no change is expected for the Five-Year Loan Prime Rate which currently sits at 4.65%.

TOMORROW’S NORTH AMERICAN MARKETS

Stimulus watch will dominate US markets with just US housing starts on tap (8:30amET). Calendar’s calendar is empty.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.